You might also like

- Cost & Management Accounting Prepared by Vishal GoelDocument20 pagesCost & Management Accounting Prepared by Vishal Goelgoel76vishalNo ratings yet

- Contract CostingDocument27 pagesContract CostingNishit BaralNo ratings yet

- Budgetary ControlDocument7 pagesBudgetary Controlaksp04No ratings yet

- Transfer Pricing MethodsDocument41 pagesTransfer Pricing MethodsExcel100% (1)

- Cost AccountingDocument22 pagesCost AccountingSiddharth KakaniNo ratings yet

- Contract Management: Brief 22Document11 pagesContract Management: Brief 22Sadaf JavedNo ratings yet

- Objectives and Functions of Cost AccountingDocument14 pagesObjectives and Functions of Cost AccountingShantanu TyagiNo ratings yet

- 06 Guide To Tender EvaluationDocument9 pages06 Guide To Tender Evaluationromelramarack1858No ratings yet

- Application of Evaluation Methods in UgandaDocument6 pagesApplication of Evaluation Methods in UgandaEmmaNo ratings yet

- Job, Batch, ContractDocument25 pagesJob, Batch, ContractParminder Bajaj100% (1)

- Objectives of Cost Analysis ControlDocument19 pagesObjectives of Cost Analysis Controlprecious omokhaiyeNo ratings yet

- DMS Demo - Job Card FlowDocument25 pagesDMS Demo - Job Card Flowapi-3858425No ratings yet

- Makerere University College of Business and Management Studies Master of Business AdministrationDocument15 pagesMakerere University College of Business and Management Studies Master of Business AdministrationDamulira DavidNo ratings yet

- Cost of ProductionDocument24 pagesCost of ProductionPiyush MahajanNo ratings yet

- 1.PPT Cost AccountingDocument14 pages1.PPT Cost AccountingShruti GargNo ratings yet

- ACM 402 Unit - IV To V (Classnotes)Document78 pagesACM 402 Unit - IV To V (Classnotes)Vandana Sharma100% (1)

- ValuationDocument23 pagesValuationishaNo ratings yet

- Introduction To Cost Accounting: Prof. Chandrakala.M Department of Commerce Kristu Jayanti College BengaluruDocument11 pagesIntroduction To Cost Accounting: Prof. Chandrakala.M Department of Commerce Kristu Jayanti College BengaluruChandrakala 10No ratings yet

- Unit Iv: Cost Volume Profit (CVP) AnalysisDocument51 pagesUnit Iv: Cost Volume Profit (CVP) AnalysisBereket DesalegnNo ratings yet

- Marginal Costing: A Management Technique For Profit Planning, Cost Control and Decision MakingDocument17 pagesMarginal Costing: A Management Technique For Profit Planning, Cost Control and Decision Makingdivyesh_variaNo ratings yet

- Contract CostingDocument11 pagesContract CostingCOMEDSCENTRENo ratings yet

- Cost Sheet PDFDocument17 pagesCost Sheet PDFRajuSharmiNo ratings yet

- Demand ForecastingDocument16 pagesDemand Forecastingkarteek_arNo ratings yet

- Cost Accounting Unit 1Document16 pagesCost Accounting Unit 1archana_anuragiNo ratings yet

- Variable & Absorption CostingDocument23 pagesVariable & Absorption CostingRobin DasNo ratings yet

- 3 - Cost Volume Profit AnalysisDocument1 page3 - Cost Volume Profit AnalysisPattraniteNo ratings yet

- Cost NotesDocument16 pagesCost NotesKomal GowdaNo ratings yet

- Materials Management-Unit-3Document15 pagesMaterials Management-Unit-3Garima KwatraNo ratings yet

- Price AnalysisDocument13 pagesPrice Analysisyam0078No ratings yet

- Time Value of MoneyDocument19 pagesTime Value of Moneyjohnnyboy30003223No ratings yet

- Introduction To Accounting For Construction ContractsDocument4 pagesIntroduction To Accounting For Construction ContractsJohn TomNo ratings yet

- Costing ElementsDocument3 pagesCosting ElementsIsHq VishqNo ratings yet

- Cost Concepts & Classification ShailajaDocument30 pagesCost Concepts & Classification ShailajaPankaj VyasNo ratings yet

- Methods of Costing 1 PDFDocument21 pagesMethods of Costing 1 PDFRupesh Shinde100% (1)

- Implementing Quality ConceptsDocument14 pagesImplementing Quality ConceptsAnonymous KYjEOO2nGNo ratings yet

- Contract Costing Sample QuestionsDocument12 pagesContract Costing Sample QuestionsArjan AdhikariNo ratings yet

- Inflation AccountingDocument23 pagesInflation AccountingthejojoseNo ratings yet

- Process of Fundamental Analysis PDFDocument8 pagesProcess of Fundamental Analysis PDFajay.1k7625100% (1)

- Chapter Two Cost Concepts and Classification: Value Chain Functions and Examples of Costs R&D Example of Cost DriverDocument13 pagesChapter Two Cost Concepts and Classification: Value Chain Functions and Examples of Costs R&D Example of Cost DriverEnoch HE100% (1)

- Cost and ManagementDocument310 pagesCost and ManagementWaleed Noman100% (1)

- Replacement Study: Engineering EconomyDocument28 pagesReplacement Study: Engineering Economycyper zoonNo ratings yet

- Accounting Treatment of Zakah: Additional Evidence From AAOIFIDocument6 pagesAccounting Treatment of Zakah: Additional Evidence From AAOIFIMuhammad SheikhNo ratings yet

- Standard Costing Summary For CA Inter, CMA Inter, CS ExecutiveDocument5 pagesStandard Costing Summary For CA Inter, CMA Inter, CS Executivecd classes100% (1)

- Chapter 8 - ForecastingDocument42 pagesChapter 8 - ForecastingVernier MirandaNo ratings yet

- Transfer PricingDocument20 pagesTransfer PricingPhaniraj Lenkalapally0% (1)

- Methods and Types of CostingDocument2 pagesMethods and Types of CostingCristina Padrón PeraltaNo ratings yet

- Bbe 3102 (Cost Accounting) Lecture Notes - Topic 1 (Part Ii)Document9 pagesBbe 3102 (Cost Accounting) Lecture Notes - Topic 1 (Part Ii)SAMSON OYOO OTUKENENo ratings yet

- Chapter 1, 4,6 THEORYgfgciibcom ADocument16 pagesChapter 1, 4,6 THEORYgfgciibcom APradeepNo ratings yet

- Performance ManagementDocument16 pagesPerformance ManagementKanchanaNo ratings yet

- Meaning, Importance and Categories Cost Accounting Standards-Generally Accepted Cost Accounting Standards Purpose, Objectives and ApplicabilityDocument18 pagesMeaning, Importance and Categories Cost Accounting Standards-Generally Accepted Cost Accounting Standards Purpose, Objectives and ApplicabilityKarishma JainNo ratings yet

- MA AssignmentDocument11 pagesMA AssignmentSathyendra Singh ChauhanNo ratings yet

- Cost Accounting ConceptsDocument18 pagesCost Accounting Concepts18arshiNo ratings yet

- Anand Pandey COSTINGDocument8 pagesAnand Pandey COSTINGAnand PandeyNo ratings yet

- Job CostingDocument9 pagesJob CostingRameez RakheNo ratings yet

- Cost AccountingDocument77 pagesCost Accountinggokulamaromal2001No ratings yet

- Ch-3 Cost BehaviorDocument25 pagesCh-3 Cost BehaviorNeelesh MishraNo ratings yet

- Chap 4 CMADocument18 pagesChap 4 CMAsolomonaauNo ratings yet

- Introduction To Process CostingDocument29 pagesIntroduction To Process Costingshersudsher67% (3)

- Methods of CostingDocument4 pagesMethods of CostingRajamma YogeshNo ratings yet

- Finman Case 1Document9 pagesFinman Case 1Jastine Sosa100% (1)

- Measuring Service Quality in Regional Rural Bank: Research Project Synopsis ONDocument24 pagesMeasuring Service Quality in Regional Rural Bank: Research Project Synopsis ONAren ChhikaraNo ratings yet

- Factors Attracting Mncs in IndiaDocument17 pagesFactors Attracting Mncs in Indiarishi100% (1)

- Form of Application For Repurchase of UnitsDocument2 pagesForm of Application For Repurchase of UnitsHaritha SankarNo ratings yet

- Acct Statement - XX6440 - 28032023Document16 pagesAcct Statement - XX6440 - 28032023Maran PrabakaranNo ratings yet

- Reissued Statement Reissued Statement: OMB No. 1545-0008 OMB No. 1545-0008Document1 pageReissued Statement Reissued Statement: OMB No. 1545-0008 OMB No. 1545-0008Sadiki LuhandeNo ratings yet

- Arbitration CaselistDocument12 pagesArbitration CaselistDaniel FordanNo ratings yet

- Shell International MarketingDocument37 pagesShell International MarketingParin Shah0% (1)

- Induction Training 182Document1 pageInduction Training 182Satyam mishraNo ratings yet

- An Appraisal of Nigeria's Micro Small and Medium Enterprises MSMES Growth Challenges and Prospects.Document15 pagesAn Appraisal of Nigeria's Micro Small and Medium Enterprises MSMES Growth Challenges and Prospects.playcharles89No ratings yet

- SITXWHS001 - Participate in Safe Work Practices Student Assessment GuideDocument34 pagesSITXWHS001 - Participate in Safe Work Practices Student Assessment GuideKAROL ESTEFANIA GARCIANo ratings yet

- The Great DepressionDocument15 pagesThe Great DepressionRAahvi RAahnaNo ratings yet

- Sewale Bitew PDFDocument84 pagesSewale Bitew PDFTILAHUNNo ratings yet

- Solutions of Money, Banking and The Financial SystemDocument105 pagesSolutions of Money, Banking and The Financial Systemscribd50% (2)

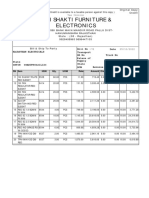

- Shri Shakti Furniture & Electronics: Credit OrginalDocument1 pageShri Shakti Furniture & Electronics: Credit OrginalRahul BansalNo ratings yet

- 6 Stocks Double Investors' Wealth Since Last Ganesh ChaturthiDocument8 pages6 Stocks Double Investors' Wealth Since Last Ganesh ChaturthiJayaprakash MuthuvatNo ratings yet

- Murdzhev P PDFDocument354 pagesMurdzhev P PDFAleksandar RistićNo ratings yet

- Draft Resolution (Saudi Arabia, Usa, Japan)Document2 pagesDraft Resolution (Saudi Arabia, Usa, Japan)Aishwarya PotdarNo ratings yet

- Srilanka GemstoneDocument148 pagesSrilanka GemstoneJaganathan ChokkalingamNo ratings yet

- Use The Figure Below To Answer The Following QuestionsDocument5 pagesUse The Figure Below To Answer The Following QuestionsSlock TruNo ratings yet

- Catalogo GROFE IngDocument50 pagesCatalogo GROFE IngAlvaro Antonio Cristobal AtencioNo ratings yet

- Acctg 303Document9 pagesAcctg 303Anonymous IsEZYR1No ratings yet

- COIMBATOREDocument3 pagesCOIMBATOREYashNo ratings yet

- Denver Equipment Company Handbook - IndexDocument6 pagesDenver Equipment Company Handbook - IndexCristiam MercadoNo ratings yet

- Department of Education: Project Proposal IDocument6 pagesDepartment of Education: Project Proposal IIt's AlfredNo ratings yet

- Guingona V City FiscalDocument1 pageGuingona V City FiscalFaye Jennifer Pascua PerezNo ratings yet

- The Australian EconomyDocument35 pagesThe Australian Economybiangbiang bangNo ratings yet

- For Billing Enquiry Visit Https://selfcare - Tikona.inDocument2 pagesFor Billing Enquiry Visit Https://selfcare - Tikona.inVivek Jain100% (1)

- GD Steam TurbinesDocument1 pageGD Steam Turbinesmadhusudanan.asbNo ratings yet

- SA Climate Action and Adaptation PlanDocument92 pagesSA Climate Action and Adaptation PlanDavid IbanezNo ratings yet

- Money Made Easy: How to Budget, Pay Off Debt, and Save MoneyFrom EverandMoney Made Easy: How to Budget, Pay Off Debt, and Save MoneyRating: 5 out of 5 stars5/5 (1)

- The Black Girl's Guide to Financial Freedom: Build Wealth, Retire Early, and Live the Life of Your DreamsFrom EverandThe Black Girl's Guide to Financial Freedom: Build Wealth, Retire Early, and Live the Life of Your DreamsNo ratings yet

- Basic Python in Finance: How to Implement Financial Trading Strategies and Analysis using PythonFrom EverandBasic Python in Finance: How to Implement Financial Trading Strategies and Analysis using PythonRating: 5 out of 5 stars5/5 (9)

- Financial Literacy for All: Disrupting Struggle, Advancing Financial Freedom, and Building a New American Middle ClassFrom EverandFinancial Literacy for All: Disrupting Struggle, Advancing Financial Freedom, and Building a New American Middle ClassNo ratings yet

- The Best Team Wins: The New Science of High PerformanceFrom EverandThe Best Team Wins: The New Science of High PerformanceRating: 4.5 out of 5 stars4.5/5 (31)

- CAPITAL: Vol. 1-3: Complete Edition - Including The Communist Manifesto, Wage-Labour and Capital, & Wages, Price and ProfitFrom EverandCAPITAL: Vol. 1-3: Complete Edition - Including The Communist Manifesto, Wage-Labour and Capital, & Wages, Price and ProfitRating: 4 out of 5 stars4/5 (6)

- Swot analysis in 4 steps: How to use the SWOT matrix to make a difference in career and businessFrom EverandSwot analysis in 4 steps: How to use the SWOT matrix to make a difference in career and businessRating: 4.5 out of 5 stars4.5/5 (4)

- You Need a Budget: The Proven System for Breaking the Paycheck-to-Paycheck Cycle, Getting Out of Debt, and Living the Life You WantFrom EverandYou Need a Budget: The Proven System for Breaking the Paycheck-to-Paycheck Cycle, Getting Out of Debt, and Living the Life You WantRating: 4 out of 5 stars4/5 (104)

- Radically Simple Accounting: A Way Out of the Dark and Into the ProfitFrom EverandRadically Simple Accounting: A Way Out of the Dark and Into the ProfitRating: 4.5 out of 5 stars4.5/5 (9)

- Budget Management for Beginners: Proven Strategies to Revamp Business & Personal Finance Habits. Stop Living Paycheck to Paycheck, Get Out of Debt, and Save Money for Financial Freedom.From EverandBudget Management for Beginners: Proven Strategies to Revamp Business & Personal Finance Habits. Stop Living Paycheck to Paycheck, Get Out of Debt, and Save Money for Financial Freedom.Rating: 5 out of 5 stars5/5 (91)

- The 30-Day Money Cleanse: Take Control of Your Finances, Manage Your Spending, and De-Stress Your Money for Good (Personal Finance and Budgeting Self-Help Book)From EverandThe 30-Day Money Cleanse: Take Control of Your Finances, Manage Your Spending, and De-Stress Your Money for Good (Personal Finance and Budgeting Self-Help Book)Rating: 3.5 out of 5 stars3.5/5 (9)

- How To Budget And Manage Your Money In 7 Simple StepsFrom EverandHow To Budget And Manage Your Money In 7 Simple StepsRating: 5 out of 5 stars5/5 (4)

- CDL Study Guide 2022-2023: Everything You Need to Pass Your Exam with Flying Colors on the First Try. Theory, Q&A, Explanations + 13 Interactive TestsFrom EverandCDL Study Guide 2022-2023: Everything You Need to Pass Your Exam with Flying Colors on the First Try. Theory, Q&A, Explanations + 13 Interactive TestsRating: 4 out of 5 stars4/5 (4)

- Minding Your Own Business: A Common Sense Guide to Home Management and IndustryFrom EverandMinding Your Own Business: A Common Sense Guide to Home Management and IndustryRating: 5 out of 5 stars5/5 (1)

- Debt Freedom: A Realistic Guide On How To Eliminate Debt, Including Credit Card Debt ForeverFrom EverandDebt Freedom: A Realistic Guide On How To Eliminate Debt, Including Credit Card Debt ForeverRating: 3 out of 5 stars3/5 (2)

- Personal Finance for Beginners - A Simple Guide to Take Control of Your Financial SituationFrom EverandPersonal Finance for Beginners - A Simple Guide to Take Control of Your Financial SituationRating: 4.5 out of 5 stars4.5/5 (18)

- Money Management: An Essential Guide on How to Get out of Debt and Start Building Financial Wealth, Including Budgeting and Investing Tips, Ways to Save and Frugal Living IdeasFrom EverandMoney Management: An Essential Guide on How to Get out of Debt and Start Building Financial Wealth, Including Budgeting and Investing Tips, Ways to Save and Frugal Living IdeasRating: 4 out of 5 stars4/5 (2)

- Rich Nurse Poor Nurses: The Critical Stuff Nursing School Forgot To Teach YouFrom EverandRich Nurse Poor Nurses: The Critical Stuff Nursing School Forgot To Teach YouRating: 4 out of 5 stars4/5 (2)

- Inflation Hacking: Inflation Investing Techniques to Benefit from High InflationFrom EverandInflation Hacking: Inflation Investing Techniques to Benefit from High InflationRating: 4.5 out of 5 stars4.5/5 (5)