You might also like

- Analyzing, Recording, Posting and Trial Balance: Normal Balance of AccountsDocument6 pagesAnalyzing, Recording, Posting and Trial Balance: Normal Balance of AccountsMich Binayug100% (1)

- Chapter 3 Basic AccountingDocument35 pagesChapter 3 Basic AccountingDeanna LuiseNo ratings yet

- Simple and Compound EntryDocument4 pagesSimple and Compound EntryJezeil DimasNo ratings yet

- Accounting For Sole Proprietorship Problem3-6Document3 pagesAccounting For Sole Proprietorship Problem3-6Rocel Domingo100% (1)

- C. Identification, Recording, Communication.: ExceptDocument9 pagesC. Identification, Recording, Communication.: ExceptSylvia Al-a'maNo ratings yet

- Economics PrelimsDocument2 pagesEconomics PrelimsYannie Costibolo IsananNo ratings yet

- Basic Financial Accounting and Reporting: Ishmael Y. Reyes, CPADocument32 pagesBasic Financial Accounting and Reporting: Ishmael Y. Reyes, CPAMicaela EncinasNo ratings yet

- Perpetual Transactions: Journal EntriesDocument71 pagesPerpetual Transactions: Journal EntriesRona Mae AnteroNo ratings yet

- Tesorero, Princess Kelly V, HRM 1-4 Baen m9Document6 pagesTesorero, Princess Kelly V, HRM 1-4 Baen m9Kelly TesoreroNo ratings yet

- ACCTG 1 Week 2-3 - Accounting in BusinessDocument13 pagesACCTG 1 Week 2-3 - Accounting in BusinessReygie FabrigaNo ratings yet

- The Accounting CycleDocument34 pagesThe Accounting CycleMarriel Fate CullanoNo ratings yet

- Financial Accounting Ii Sample QuizDocument2 pagesFinancial Accounting Ii Sample QuizThea FloresNo ratings yet

- FundamentalsofAccounting IDSDocument2 pagesFundamentalsofAccounting IDSYu Babylan33% (3)

- Accounting Concepts & PrinciplesDocument8 pagesAccounting Concepts & PrinciplesJonalyn abesNo ratings yet

- PDF Journal Entries Tradingdocx CompressDocument79 pagesPDF Journal Entries Tradingdocx CompressMaskter TwinsetsNo ratings yet

- 24-Month Note Due To BDODocument3 pages24-Month Note Due To BDOEliza CruzNo ratings yet

- Recording Business TransactionsDocument12 pagesRecording Business TransactionsAsh imoNo ratings yet

- ACEFIAR Quiz No. 7Document2 pagesACEFIAR Quiz No. 7Marriel Fate CullanoNo ratings yet

- Accounting: Adjusting EntriesDocument11 pagesAccounting: Adjusting EntriesCamellia100% (2)

- It Quiz Journal EntriesDocument4 pagesIt Quiz Journal EntriesLino Gumpal0% (1)

- Adjusting Entries ExampleDocument5 pagesAdjusting Entries ExampleSiak Ni LynnLadyNo ratings yet

- ADocument57 pagesAAliaJustineIlagan100% (1)

- Chapter 1Document27 pagesChapter 1Catherine RiveraNo ratings yet

- Theories of AccountingDocument4 pagesTheories of AccountingShanine BaylonNo ratings yet

- 2016 14 PPT Acctg1 Adjusting EntriesDocument20 pages2016 14 PPT Acctg1 Adjusting Entriesash wu100% (3)

- Quiz 4 - Statement of Cash FlowsDocument2 pagesQuiz 4 - Statement of Cash FlowsFrancez Anne Guanzon33% (3)

- CHAPTER 1 (Financial Accounting and Reporting)Document2 pagesCHAPTER 1 (Financial Accounting and Reporting)Wawex DavisNo ratings yet

- The DualisticDocument6 pagesThe DualisticFlorence LapinigNo ratings yet

- Exercise 1 - Transaction AnalysisDocument2 pagesExercise 1 - Transaction AnalysistmhoangvnaNo ratings yet

- WorksheetDocument7 pagesWorksheetCamelliaNo ratings yet

- Practice Set I AcctgDocument14 pagesPractice Set I AcctgJan Pearl Hinampas100% (1)

- Journalizing Merchandising TransactionsDocument3 pagesJournalizing Merchandising TransactionsMarian Augelio PolancoNo ratings yet

- CAT-CB Questionnaires (Encoded)Document13 pagesCAT-CB Questionnaires (Encoded)Anob Ehij100% (1)

- Journalizing To Adjusting Entries QuizDocument3 pagesJournalizing To Adjusting Entries QuizNemar Jay Capitania100% (1)

- Accounting 1Document16 pagesAccounting 1Rommel Angelo AgacitaNo ratings yet

- Accounting For Merchandising Operation With Special JournalsDocument33 pagesAccounting For Merchandising Operation With Special JournalsJasmine ActaNo ratings yet

- Handout 6 Accounting For Service Merchandising and Manufacturing BusinessesDocument8 pagesHandout 6 Accounting For Service Merchandising and Manufacturing BusinessesSevi MendezNo ratings yet

- Adjusting The Book of AccountsDocument33 pagesAdjusting The Book of Accountsjoshua zabala100% (1)

- CHP 2 Exam Preparation ProblemsDocument3 pagesCHP 2 Exam Preparation ProblemsShawn JohnstonNo ratings yet

- Module 1 Review of The Accounting Cycle For A Service Business by Marivic ManaloDocument28 pagesModule 1 Review of The Accounting Cycle For A Service Business by Marivic ManaloChing ChongNo ratings yet

- Journal Entries TradingDocument79 pagesJournal Entries TradingAvox EverdeenNo ratings yet

- AccountingDocument5 pagesAccountingAbe Loran PelandianaNo ratings yet

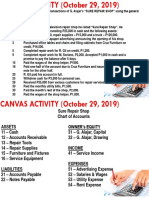

- JD Repair Shop TransactionsDocument14 pagesJD Repair Shop TransactionsAndrew Sy Scott100% (1)

- Accounting Adjusting EntryDocument20 pagesAccounting Adjusting EntryClemencia Masiba100% (1)

- Larry Jones Laundry Shop New FormatDocument18 pagesLarry Jones Laundry Shop New FormatVincent Madrid100% (1)

- Joannamarie Uy ProblemDocument1 pageJoannamarie Uy ProblemFeiya Liu50% (2)

- Santa Rosa Campus City of Santa Rosa, Laguna: Polytechnic University of The PhilippinesDocument19 pagesSanta Rosa Campus City of Santa Rosa, Laguna: Polytechnic University of The Philippinesareum100% (1)

- Comprehensive Accounting Cycle Review Problem-1Document11 pagesComprehensive Accounting Cycle Review Problem-1api-296886708100% (1)

- Adjusting Entries: Circle The Letter of The Best Answer in Each of The Following ItemsDocument2 pagesAdjusting Entries: Circle The Letter of The Best Answer in Each of The Following ItemsAshley RoweNo ratings yet

- General Ledger - Adrianne, Mendoza-BSBA-1 BLK BDocument6 pagesGeneral Ledger - Adrianne, Mendoza-BSBA-1 BLK BJaks ExplorerNo ratings yet

- FAR Chapter4 FinalDocument43 pagesFAR Chapter4 FinalPATRICIA COLINANo ratings yet

- Accounting Cycle, Entries and ConceptDocument64 pagesAccounting Cycle, Entries and Conceptdude devil100% (1)

- Canvas Activity - Journalizing - Oct - 29 PDFDocument2 pagesCanvas Activity - Journalizing - Oct - 29 PDFJian Francisco100% (2)

- I. Matching Type 1: Letter OnlyDocument8 pagesI. Matching Type 1: Letter OnlyJohn Lloyd LlananNo ratings yet

- Quiz On The Accounting EquationDocument5 pagesQuiz On The Accounting EquationCeejay MancillaNo ratings yet

- S. Roces Answer To Journal EntryDocument4 pagesS. Roces Answer To Journal EntryChoco LebbyNo ratings yet

- Midterm 2nd 3rd Meeting RevisedDocument6 pagesMidterm 2nd 3rd Meeting RevisedChristopher CristobalNo ratings yet

- Sem Plang Merchandising Periodic Problem With AnswersDocument21 pagesSem Plang Merchandising Periodic Problem With Answerscole sprouse100% (1)

- Chart of AccountsDocument4 pagesChart of AccountsMikez Diputado100% (1)

- HTTPSWWW Sec GovArchivesedgardata1057791000105779114000008ex991 PDFDocument99 pagesHTTPSWWW Sec GovArchivesedgardata1057791000105779114000008ex991 PDFДмитрий ЮхановNo ratings yet

- United States Geological Survey Certificate of Analysis: Andesite, AGV-2Document3 pagesUnited States Geological Survey Certificate of Analysis: Andesite, AGV-2GimpsNo ratings yet

- Draft Sale Deed PDFDocument10 pagesDraft Sale Deed PDFRicha ThakrarNo ratings yet

- MTD Consultancy Services - RFP Document Word FileDocument179 pagesMTD Consultancy Services - RFP Document Word FileDevanshNuwalNo ratings yet

- Baroda Bhim Upi FAQDocument11 pagesBaroda Bhim Upi FAQabhinav MishraNo ratings yet

- AMY PALINGCOD DOBSON TMobile BillDocument3 pagesAMY PALINGCOD DOBSON TMobile BillJonathan Seagull Livingston100% (1)

- VALUATION PROFESSIONAL FEES of Various BanksDocument12 pagesVALUATION PROFESSIONAL FEES of Various BanksArunKumarVerma100% (2)

- Hotel Grand Central ReportDocument75 pagesHotel Grand Central ReportbodhidcoolNo ratings yet

- CasesDocument3 pagesCasesamyr felipeNo ratings yet

- Current Issues Project: Cashless SocietyDocument4 pagesCurrent Issues Project: Cashless SocietyJohn OMalleyNo ratings yet

- Jailor EngDocument42 pagesJailor EngMuthu SubuNo ratings yet

- 2checkout SB Payment Method CoverageDocument25 pages2checkout SB Payment Method CoveragePaul MccollicNo ratings yet

- Gift Cards Method - APRIL 2023Document9 pagesGift Cards Method - APRIL 2023Gansta Rap50% (2)

- E-Banking: Internet Banking in IndiaDocument4 pagesE-Banking: Internet Banking in IndiaPrasanjeet BhattacharjeeNo ratings yet

- Hand Book On Know Your Circular Andhra Bank PromotionDocument81 pagesHand Book On Know Your Circular Andhra Bank PromotionSubrat Satyaranjan KanungoNo ratings yet

- Acc 216 ReviewerDocument8 pagesAcc 216 ReviewerCristine TanggoyocNo ratings yet

- Bank Al Habib Charges DetailDocument25 pagesBank Al Habib Charges DetailAtif UR RehmanNo ratings yet

- Question No.1: Write The Steps To: Create CompanyDocument15 pagesQuestion No.1: Write The Steps To: Create Companykoshalk88% (8)

- A.C. No. 4904Document5 pagesA.C. No. 4904abcdNo ratings yet

- MCQ FR I - OnsolidatedDocument50 pagesMCQ FR I - OnsolidatedAman GuptaNo ratings yet

- Axis BankDocument31 pagesAxis Bank81000No ratings yet

- Far1 MidtermDocument3 pagesFar1 MidtermCha Eun WooNo ratings yet

- Himali Akarawita Invoice PDFDocument12 pagesHimali Akarawita Invoice PDFAnura PiyatissaNo ratings yet

- AVP - Admin and Finance Support Officer JD - Part Time - FinalDocument2 pagesAVP - Admin and Finance Support Officer JD - Part Time - Finalgayle aldoNo ratings yet

- Private Car/Two Wheeler Insurance Policy - Package: D Dmmy Y Y YDocument5 pagesPrivate Car/Two Wheeler Insurance Policy - Package: D Dmmy Y Y YYash T SmartNo ratings yet

- FAQ Mobile BankingDocument5 pagesFAQ Mobile BankingAshif RejaNo ratings yet

- Payment FieldsDocument28 pagesPayment FieldsdevarajfkNo ratings yet

- Digital Payments - 1S2 - S4HANA2023 - BPD - EN - BRDocument23 pagesDigital Payments - 1S2 - S4HANA2023 - BPD - EN - BRjbatistafreitasNo ratings yet

- Account Summary: Total Due $140.33Document4 pagesAccount Summary: Total Due $140.33CARMEN HULTZNo ratings yet

- School PoliciesDocument39 pagesSchool Policiesmaisie RameetseNo ratings yet

- The Inimitable Jeeves [Classic Tales Edition]From EverandThe Inimitable Jeeves [Classic Tales Edition]Rating: 5 out of 5 stars5/5 (3)

- The House at Pooh Corner - Winnie-the-Pooh Book #4 - UnabridgedFrom EverandThe House at Pooh Corner - Winnie-the-Pooh Book #4 - UnabridgedRating: 4.5 out of 5 stars4.5/5 (5)

- You Can't Joke About That: Why Everything Is Funny, Nothing Is Sacred, and We're All in This TogetherFrom EverandYou Can't Joke About That: Why Everything Is Funny, Nothing Is Sacred, and We're All in This TogetherNo ratings yet

- The Importance of Being Earnest: Classic Tales EditionFrom EverandThe Importance of Being Earnest: Classic Tales EditionRating: 4.5 out of 5 stars4.5/5 (44)

- A**holeology The Cheat Sheet: Put the science into practice in everyday situationsFrom EverandA**holeology The Cheat Sheet: Put the science into practice in everyday situationsRating: 3.5 out of 5 stars3.5/5 (3)

- 1,001 Facts that Will Scare the S#*t Out of You: The Ultimate Bathroom ReaderFrom Everand1,001 Facts that Will Scare the S#*t Out of You: The Ultimate Bathroom ReaderRating: 3.5 out of 5 stars3.5/5 (48)

- The Book of Bad:: Stuff You Should Know Unless You’re a PussyFrom EverandThe Book of Bad:: Stuff You Should Know Unless You’re a PussyRating: 3.5 out of 5 stars3.5/5 (3)

- The Smartest Book in the World: A Lexicon of Literacy, A Rancorous Reportage, A Concise Curriculum of CoolFrom EverandThe Smartest Book in the World: A Lexicon of Literacy, A Rancorous Reportage, A Concise Curriculum of CoolRating: 4 out of 5 stars4/5 (14)

- Sex, Drugs, and Cocoa Puffs: A Low Culture ManifestoFrom EverandSex, Drugs, and Cocoa Puffs: A Low Culture ManifestoRating: 3.5 out of 5 stars3.5/5 (1428)

- The Little Book of Big F*#k Ups: 220 of History's Most-Regrettable MomentsFrom EverandThe Little Book of Big F*#k Ups: 220 of History's Most-Regrettable MomentsNo ratings yet

- The Asshole Survival Guide: How to Deal with People Who Treat You Like DirtFrom EverandThe Asshole Survival Guide: How to Deal with People Who Treat You Like DirtRating: 4 out of 5 stars4/5 (60)