You might also like

- Lucky Cement Merge With Dadabhoy CementDocument9 pagesLucky Cement Merge With Dadabhoy CementMuhammad NaveedNo ratings yet

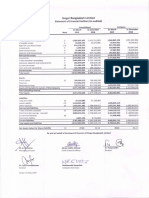

- MBA Local Compnay Presentation - Financial - AccountingDocument7 pagesMBA Local Compnay Presentation - Financial - AccountingAliza RizviNo ratings yet

- Exide Pakistan Five Year Financial AnalysisDocument13 pagesExide Pakistan Five Year Financial AnalysisziaNo ratings yet

- Nestle Financial StatementDocument48 pagesNestle Financial Statementjhenkq100% (2)

- Financial PlanDocument25 pagesFinancial PlanAyesha KanwalNo ratings yet

- Byco Data PDFDocument32 pagesByco Data PDFMuiz SaddozaiNo ratings yet

- Singer 2nd Quarter Financial Statements 2019 - WebsiteDocument12 pagesSinger 2nd Quarter Financial Statements 2019 - WebsiteAhm FerdousNo ratings yet

- MNHD Cons FS 12 2018EDocument40 pagesMNHD Cons FS 12 2018EAhmed El-AdawyNo ratings yet

- Performance Evaluation and Ratio Analysis - Meghna Cement - R1Document11 pagesPerformance Evaluation and Ratio Analysis - Meghna Cement - R1Sayed Abu Sufyan100% (1)

- Finance ProjectDocument9 pagesFinance ProjectToheed TalaNo ratings yet

- Nasr City Cons 12 2020EDocument48 pagesNasr City Cons 12 2020EAly A. SamyNo ratings yet

- Unaudited Consolidated Financial Statements: For The Quarter Ended 31 March 2022Document7 pagesUnaudited Consolidated Financial Statements: For The Quarter Ended 31 March 2022Fuaad DodooNo ratings yet

- Chapter-5 Financial Statement AnalysisDocument5 pagesChapter-5 Financial Statement AnalysisAcchu RNo ratings yet

- Financial Statement Analysis of Kohat Cement CompanyDocument67 pagesFinancial Statement Analysis of Kohat Cement CompanySaif Ali Khan BalouchNo ratings yet

- CP ALL Financial Statements 2018-2017Document3 pagesCP ALL Financial Statements 2018-2017Dave BonkilottiNo ratings yet

- Auditors Report: Financial Result 2005-2006Document11 pagesAuditors Report: Financial Result 2005-2006Hay JirenyaaNo ratings yet

- Analysis of BankDocument15 pagesAnalysis of BankSadiq SayaniNo ratings yet

- Financial Model 3 Statement Model - Final - MotilalDocument13 pagesFinancial Model 3 Statement Model - Final - MotilalSouvik BardhanNo ratings yet

- Directors Report Q3 2018 PerformanceDocument24 pagesDirectors Report Q3 2018 PerformanceMOORTHYNo ratings yet

- SDPK Financial Position Project FinalDocument33 pagesSDPK Financial Position Project FinalAmr Mekkawy100% (1)

- Annual Report 2005Document39 pagesAnnual Report 2005Farhat987No ratings yet

- Annual Report 2006Document65 pagesAnnual Report 2006Farhat987No ratings yet

- Annual Report 2007Document118 pagesAnnual Report 2007Enamul HaqueNo ratings yet

- Financial Report (Un-Audited) 31.03 .2021Document15 pagesFinancial Report (Un-Audited) 31.03 .2021barud jhdjdNo ratings yet

- Standalone Financials 20240111 (Final)Document55 pagesStandalone Financials 20240111 (Final)Sadikshya KhawasNo ratings yet

- Redco Textiles Q1 2022 ReportDocument11 pagesRedco Textiles Q1 2022 ReportTutii FarutiNo ratings yet

- Pakistan Petroleum LTDDocument43 pagesPakistan Petroleum LTDMuheeb AhmadNo ratings yet

- Directors' Report Highlights Q1 2018 Financial ResultsDocument24 pagesDirectors' Report Highlights Q1 2018 Financial ResultsAsma RehmanNo ratings yet

- Reliance Industries LTD.: Balance SheetDocument10 pagesReliance Industries LTD.: Balance SheetAayush PeriwalNo ratings yet

- Standalone Balance Sheet HighlightsDocument9 pagesStandalone Balance Sheet HighlightsLeo SaimNo ratings yet

- Square Textile Limited: (Year) (Year) (Year)Document8 pagesSquare Textile Limited: (Year) (Year) (Year)limon islamNo ratings yet

- Dialog Axiata Q4 2021 Financial ResultsDocument15 pagesDialog Axiata Q4 2021 Financial ResultsgirihellNo ratings yet

- Pak SuzukiDocument17 pagesPak SuzukiSyed Usarim Ali ShahNo ratings yet

- A. Currents Assets 29,760,685 24,261,892: I. II. Iii. IV. V. I. II. Iii. IV. V. VIDocument32 pagesA. Currents Assets 29,760,685 24,261,892: I. II. Iii. IV. V. I. II. Iii. IV. V. VITammy DaoNo ratings yet

- Financial AccountingDocument28 pagesFinancial AccountingsarmadNo ratings yet

- HBL 2005Document46 pagesHBL 2005Momna AmjadNo ratings yet

- Swisstek (Ceylon) PLC Swisstek (Ceylon) PLCDocument7 pagesSwisstek (Ceylon) PLC Swisstek (Ceylon) PLCkasun witharanaNo ratings yet

- EBL Annual Report 2021 208 218Document11 pagesEBL Annual Report 2021 208 218Fardin MarufNo ratings yet

- Directors ReportDocument14 pagesDirectors ReportShujaat AhmadNo ratings yet

- Fsap 8e - Pepsico 2012Document46 pagesFsap 8e - Pepsico 2012Allan Ahmad Sarip100% (1)

- Habib Motors 2022Document6 pagesHabib Motors 2022usmansss_606776863No ratings yet

- Company Information: Board of DirectorsDocument12 pagesCompany Information: Board of Directors03004523983No ratings yet

- Quatar ShippingDocument42 pagesQuatar Shippingben BenmezdadNo ratings yet

- HCG Manavata Oncology LLPDocument19 pagesHCG Manavata Oncology LLPBhushan ToraskarNo ratings yet

- Aisha Steel Mills 2017 balance sheet and income statementDocument33 pagesAisha Steel Mills 2017 balance sheet and income statementqamber18No ratings yet

- Resus Energy PLC: Interim Report 01st Quarter 2022-2023Document13 pagesResus Energy PLC: Interim Report 01st Quarter 2022-2023w.chathura nuwan ranasingheNo ratings yet

- Consolidated Financial Statements For 6 Months of 2022Document63 pagesConsolidated Financial Statements For 6 Months of 2022Tyler DurdenNo ratings yet

- Audit Report For Azahar Trading Ltd.Document11 pagesAudit Report For Azahar Trading Ltd.Muhammad Humayun IslamNo ratings yet

- Balance Sheet: AssetsDocument19 pagesBalance Sheet: Assetssumeer shafiqNo ratings yet

- LGE - 22 1Q - Separate - F - SignedDocument71 pagesLGE - 22 1Q - Separate - F - SignedMariam GaboNo ratings yet

- Financial Statement Analysis of Masan Company Masan GroupDocument24 pagesFinancial Statement Analysis of Masan Company Masan GroupTammy DaoNo ratings yet

- HUBCO Financial Statements Analysis 2015-2020Document97 pagesHUBCO Financial Statements Analysis 2015-2020Omer CrestianiNo ratings yet

- Financial Statement Analysis and WACC CalculationDocument4 pagesFinancial Statement Analysis and WACC CalculationSergio Andres Cortes ContrerasNo ratings yet

- Balance Sheet (MGC) : Assets GegrigationDocument164 pagesBalance Sheet (MGC) : Assets GegrigationRizwan BaigNo ratings yet

- Financial in WebsiteDocument38 pagesFinancial in WebsiteJay prakash ChaudharyNo ratings yet

- Singer Bangladesh Limited Financial Statement AnalysisDocument12 pagesSinger Bangladesh Limited Financial Statement AnalysisAhm FerdousNo ratings yet

- Competitor 1 Sanofi Aventis Pakistan Limited Balance Sheets and Income Statements 2016-2020Document6 pagesCompetitor 1 Sanofi Aventis Pakistan Limited Balance Sheets and Income Statements 2016-2020Ahsan KamranNo ratings yet

- DSML Mar 07Document1 pageDSML Mar 07usman_dhilloNo ratings yet

- Financial AnalysisDocument29 pagesFinancial AnalysisAn NguyễnNo ratings yet

- Alfalah Managerial Policy/Strategic Management SlidesDocument38 pagesAlfalah Managerial Policy/Strategic Management SlidesM.Zuhair AltafNo ratings yet

- What Is Organizational BehaviourDocument16 pagesWhat Is Organizational BehaviourM.Zuhair AltafNo ratings yet

- Alfalah Managerial Policy/Strategic ManagementDocument26 pagesAlfalah Managerial Policy/Strategic ManagementM.Zuhair AltafNo ratings yet

- PTCL N PaknetDocument54 pagesPTCL N PaknetM.Zuhair AltafNo ratings yet

- Strategic Human Resource Management Practices of Standard Chartered BankDocument39 pagesStrategic Human Resource Management Practices of Standard Chartered BankM.Zuhair Altaf63% (19)

- Angro-N-Pakarab (OB)Document40 pagesAngro-N-Pakarab (OB)M.Zuhair AltafNo ratings yet

- MitchellsDocument53 pagesMitchellsM.Zuhair Altaf100% (1)

- ForexDocument48 pagesForexM.Zuhair Altaf100% (2)

- A Term Report: in The Name of Allah, Most Beneficent, Most MercifulDocument33 pagesA Term Report: in The Name of Allah, Most Beneficent, Most MercifulM.Zuhair AltafNo ratings yet

- Alfalah Bank InternshipDocument75 pagesAlfalah Bank InternshipM.Zuhair Altaf100% (5)

- D G CementDocument18 pagesD G CementM.Zuhair AltafNo ratings yet

- Pia N AblDocument33 pagesPia N AblM.Zuhair Altaf40% (5)

- Telecom Cellular SectorDocument32 pagesTelecom Cellular SectorM.Zuhair Altaf100% (1)

- Health& Safety (HRM)Document31 pagesHealth& Safety (HRM)M.Zuhair Altaf60% (5)

- Power N PoliticsDocument31 pagesPower N PoliticsM.Zuhair Altaf100% (5)

- Forex (Foreign Exchange Market)Document22 pagesForex (Foreign Exchange Market)M.Zuhair Altaf50% (4)

- Organizational Behaviour Pak Elektron LimitedDocument41 pagesOrganizational Behaviour Pak Elektron LimitedM.Zuhair Altaf100% (3)

- Internship FormatDocument6 pagesInternship FormatM.Zuhair AltafNo ratings yet

- Every Little Helps? ESG News and Stock Market ReactionDocument23 pagesEvery Little Helps? ESG News and Stock Market ReactionOgan Erkin ErkanNo ratings yet

- W6 Module 5 - Fringe Benefits and Dealings in PropertyDocument13 pagesW6 Module 5 - Fringe Benefits and Dealings in PropertyElmeerajh JudavarNo ratings yet

- CM1 Overview of AccountingDocument14 pagesCM1 Overview of AccountingMark GerwinNo ratings yet

- FEU Annual Report 2019-2020Document370 pagesFEU Annual Report 2019-2020Llanzana EVersonNo ratings yet

- Understanding Order Flow VolatilityDocument18 pagesUnderstanding Order Flow Volatilityitvmw04 itvmw04No ratings yet

- FinanceDocument5 pagesFinancePiyushNo ratings yet

- Capital Structure DecisionsDocument32 pagesCapital Structure Decisionsrimoniba33% (3)

- Housing Equity: Its Impact On Household Net Worth in The US and Anaheim Santa Ana, CADocument7 pagesHousing Equity: Its Impact On Household Net Worth in The US and Anaheim Santa Ana, CAdbeisnerNo ratings yet

- Docshare - Tips 1 Strawman Termination ErsquobookDocument16 pagesDocshare - Tips 1 Strawman Termination ErsquobookBálint Fodor100% (6)

- ArinoLegal PowerPoints Securities Regulation Ver2019Aug03Document89 pagesArinoLegal PowerPoints Securities Regulation Ver2019Aug03KinitDelfinCelestialNo ratings yet

- Trading in The Shadow of The Smart Money BookDocument192 pagesTrading in The Shadow of The Smart Money BookSalvo Nona85% (46)

- Blaine Kitchenware Inc.Document13 pagesBlaine Kitchenware Inc.vishitj100% (4)

- What Is NAV of Mutual Fund, Check Latest MF NAV OnlineDocument7 pagesWhat Is NAV of Mutual Fund, Check Latest MF NAV Onlineakash ThakurNo ratings yet

- Stock Redemption AgreementDocument7 pagesStock Redemption Agreementpeaser0712100% (1)

- SPECULATIVE TRANSACTIONSDocument13 pagesSPECULATIVE TRANSACTIONSMin Ha-riNo ratings yet

- Chilean Fruit and VegetablesDocument38 pagesChilean Fruit and VegetablesBenny DuongNo ratings yet

- Indian Stock MarketDocument8 pagesIndian Stock MarketArpit JainNo ratings yet

- Derivative MarketsDocument143 pagesDerivative MarketsdikshitaNo ratings yet

- IIFL Demat Account FormDocument23 pagesIIFL Demat Account FormSreeram MandavalliNo ratings yet

- Real Estate Accounting PoliciesDocument11 pagesReal Estate Accounting PoliciessadiksunasaraNo ratings yet

- Fdi by MC Donald Presented by Tarun JhalaniDocument28 pagesFdi by MC Donald Presented by Tarun Jhalanikhandelwalmba0% (1)

- Stock Market MechanismDocument30 pagesStock Market MechanismFahim AkhtarNo ratings yet

- 10 28 QuestionsDocument5 pages10 28 QuestionstikaNo ratings yet

- When A Company Holds Between 20Document3 pagesWhen A Company Holds Between 20Eych Mendoza100% (1)

- Always Go in With A PlanDocument8 pagesAlways Go in With A PlanJohny Msa HmarNo ratings yet

- Merger 2Document102 pagesMerger 2dinesh khatriNo ratings yet

- SEC Order on PMMSI stockholders' meeting quorum upheldDocument11 pagesSEC Order on PMMSI stockholders' meeting quorum upheldMegan AglauaNo ratings yet

- Acquisition Finance 2021Document19 pagesAcquisition Finance 2021RAKSHIT CHAUHANNo ratings yet

- Original PDF Financial Management Core Concepts 4th Edition by Raymond Brooks PDFDocument42 pagesOriginal PDF Financial Management Core Concepts 4th Edition by Raymond Brooks PDFmathew.robertson818100% (33)

- Single Entry SystemDocument6 pagesSingle Entry SystemQuestionscastle Friend67% (3)