You might also like

- ICICI Merchant ServicesDocument4 pagesICICI Merchant ServicesPranav GandhiNo ratings yet

- Merchant BankingDocument76 pagesMerchant Bankingleen_badiger911No ratings yet

- Indian Bank AssociationDocument29 pagesIndian Bank AssociationBankNo ratings yet

- Permanent Account Number (PAN) GuideDocument13 pagesPermanent Account Number (PAN) GuideAli Shaikh AbdulNo ratings yet

- Fixed DepositDocument119 pagesFixed Depositshreeya salunkeNo ratings yet

- Online Payment SystemDocument30 pagesOnline Payment SystemDjks YobNo ratings yet

- Repoprt On Loans & Advances PDFDocument66 pagesRepoprt On Loans & Advances PDFTitas Manower50% (4)

- Online Blood Bank Management System HomepageDocument41 pagesOnline Blood Bank Management System HomepageamritaNo ratings yet

- A Project Report On Credit CardDocument26 pagesA Project Report On Credit CardKGF SARTH ARMYNo ratings yet

- Innovations of ATM Banking Services and Upcoming Challenges: Bangladesh PerspectiveDocument67 pagesInnovations of ATM Banking Services and Upcoming Challenges: Bangladesh PerspectiveRahu RayhanNo ratings yet

- A B C D of E-BankingDocument75 pagesA B C D of E-Bankinglove tannaNo ratings yet

- Yes Bank (Case)Document6 pagesYes Bank (Case)naviiiiiNo ratings yet

- FX Market Impact on Indian EconomyDocument51 pagesFX Market Impact on Indian Economynikitapatil420No ratings yet

- Study of Cash Management at Standard Chartered BankDocument115 pagesStudy of Cash Management at Standard Chartered BankVishnu Prasad100% (2)

- Karnataka Bank Vishal Chopra 05110Document64 pagesKarnataka Bank Vishal Chopra 05110Kiran Gowda100% (1)

- Project On Merchant BankingDocument56 pagesProject On Merchant BankingBronil W DabreoNo ratings yet

- Plastic Money Report on Credit and Debit CardsDocument55 pagesPlastic Money Report on Credit and Debit CardsDisha100% (1)

- GMP ListDocument1 pageGMP ListIan JamesNo ratings yet

- Financial Services by BOMDocument71 pagesFinancial Services by BOMmsb homeNo ratings yet

- SCC Banking Information Sheet SpaDocument1 pageSCC Banking Information Sheet SpaJonathan ObandoNo ratings yet

- Ranson Dantis Project Black Book TybmsDocument87 pagesRanson Dantis Project Black Book Tybmsranson dantisNo ratings yet

- Plastic Money Full Project Copy ARNABDocument41 pagesPlastic Money Full Project Copy ARNABarnab_b8767% (3)

- A Study On Plastic MoneyDocument18 pagesA Study On Plastic MoneyPreshita VaithyNo ratings yet

- Axis Bank Debit and Credit Card SonamDocument81 pagesAxis Bank Debit and Credit Card SonamsonamNo ratings yet

- Plastic Money in IndiaDocument71 pagesPlastic Money in IndiaDexter LoboNo ratings yet

- Black BookDocument85 pagesBlack BookVinayak ArchanapalliNo ratings yet

- International Wire Transfer Quick Tips and FAQDocument4 pagesInternational Wire Transfer Quick Tips and FAQEmanuelNo ratings yet

- Understanding the Credit Card IndustryDocument18 pagesUnderstanding the Credit Card IndustryheadpncNo ratings yet

- Code ListDocument192 pagesCode ListMohammad Alamgir HossainNo ratings yet

- GL PL Code ChartDocument12 pagesGL PL Code ChartengrlumanNo ratings yet

- Banking FraudDocument24 pagesBanking FraudchaitudscNo ratings yet

- Customers' Satisfaction with Standard Chartered Bank's Service QualityDocument55 pagesCustomers' Satisfaction with Standard Chartered Bank's Service QualityAftab MohammedNo ratings yet

- Project by BrincyDocument64 pagesProject by BrincyJeeva VargheseNo ratings yet

- Mobile BankingDocument66 pagesMobile BankingNalini SharmaNo ratings yet

- project-on-Merchant-BankingV FINALDocument89 pagesproject-on-Merchant-BankingV FINALTrive-d VIkNo ratings yet

- Investment BankingDocument32 pagesInvestment BankingRavi SharmaNo ratings yet

- Unit 5 E Commerce Payment SystemDocument4 pagesUnit 5 E Commerce Payment SystemAltaf HyssainNo ratings yet

- Blackbook FinalDocument61 pagesBlackbook FinalSanjali MukadamNo ratings yet

- Axis BankDocument117 pagesAxis BankGufran Shaikh100% (2)

- Brand Management (BRAND AUDIT) BankIslamiDocument59 pagesBrand Management (BRAND AUDIT) BankIslamiBilawal ShabbirNo ratings yet

- Cis - PJSPDocument3 pagesCis - PJSPLaert Ruttemberg100% (2)

- Internship Report On "Credit Risk Management" of Prime Bank Limited, Head OfficeDocument59 pagesInternship Report On "Credit Risk Management" of Prime Bank Limited, Head OfficeSamuel Sourav100% (1)

- Banking FraudDocument75 pagesBanking FraudAbhishek KanereNo ratings yet

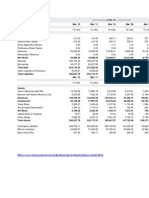

- Balance Sheet of Axis BankDocument8 pagesBalance Sheet of Axis BankKushal GuptaNo ratings yet

- Credit Card Icici Bank: Membership GuideDocument14 pagesCredit Card Icici Bank: Membership GuideAnand RajNo ratings yet

- Project Net BankingDocument37 pagesProject Net Bankingsamrat1988100% (1)

- Jana Bank General Terms and Conditions For AccountsDocument18 pagesJana Bank General Terms and Conditions For AccountsArc En CielNo ratings yet

- International Bank Account Number (IBAN)Document2 pagesInternational Bank Account Number (IBAN)Flaviub23No ratings yet

- Radhika Growth of Banking SectorDocument36 pagesRadhika Growth of Banking SectorPranav ViraNo ratings yet

- Mahindara Katak BankDocument48 pagesMahindara Katak BankChirag KarkateNo ratings yet

- QL QVK MR SGJF 3 DXDocument8 pagesQL QVK MR SGJF 3 DXNimish SrivastavaNo ratings yet

- Bank details with account numbers and PANDocument2 pagesBank details with account numbers and PANsuneethaNo ratings yet

- HCBC CC InfoDocument5 pagesHCBC CC Infooninx26No ratings yet

- Customer Satisfaction with ATM Services in SolanDocument75 pagesCustomer Satisfaction with ATM Services in Solandinesh_v_0076945100% (2)

- Electronic Financial Services: Technology and ManagementFrom EverandElectronic Financial Services: Technology and ManagementRating: 5 out of 5 stars5/5 (1)

- Review of Some SMS Verification Services and Virtual Debit/Credit Cards Services for Online Accounts VerificationsFrom EverandReview of Some SMS Verification Services and Virtual Debit/Credit Cards Services for Online Accounts VerificationsNo ratings yet

- Previos Bank Po Solved Papers Completee Book 610 PagesDocument610 pagesPrevios Bank Po Solved Papers Completee Book 610 PagesSwati TewtiyaNo ratings yet

- MacroDocument1 pageMacrosshishirkumarNo ratings yet

- Month: Date Activity Duration in HrsDocument34 pagesMonth: Date Activity Duration in HrssshishirkumarNo ratings yet

- EMI Using SolverDocument15 pagesEMI Using SolversshishirkumarNo ratings yet

- Calendar ProblemsDocument31 pagesCalendar ProblemsvaranasilkoNo ratings yet

- 108 Facts About TelanganaDocument11 pages108 Facts About TelanganasshishirkumarNo ratings yet

- Obermiller Brand Loyalty MsDocument29 pagesObermiller Brand Loyalty MssshishirkumarNo ratings yet

- The Duckworth-Lewis Method and Twenty20 CricketDocument44 pagesThe Duckworth-Lewis Method and Twenty20 CricketsshishirkumarNo ratings yet

- Justice S U KhanDocument1 pageJustice S U KhanKapil SethiNo ratings yet

- Pension Field Verification FormDocument1 pagePension Field Verification FormRaj TejNo ratings yet

- Anthony VixayoDocument2 pagesAnthony Vixayoapi-533975078No ratings yet

- SAS HB 06 Weapons ID ch1 PDFDocument20 pagesSAS HB 06 Weapons ID ch1 PDFChris EfstathiouNo ratings yet

- BusLaw Chapter 1Document4 pagesBusLaw Chapter 1ElleNo ratings yet

- Introduction to Social Media AnalyticsDocument26 pagesIntroduction to Social Media AnalyticsDiksha TanejaNo ratings yet

- Critical Perspectives On AccountingDocument17 pagesCritical Perspectives On AccountingUmar Amar100% (2)

- European Gunnery's Impact on Artillery in 16th Century IndiaDocument9 pagesEuropean Gunnery's Impact on Artillery in 16th Century Indiaharry3196No ratings yet

- 721-1002-000 Ad 0Document124 pages721-1002-000 Ad 0rashmi mNo ratings yet

- People of The Philippines vs. OrsalDocument17 pagesPeople of The Philippines vs. OrsalKTNo ratings yet

- Hookah Bar Business PlanDocument34 pagesHookah Bar Business PlanAbdelkebir LabyadNo ratings yet

- Phil Pharma Health Vs PfizerDocument14 pagesPhil Pharma Health Vs PfizerChristian John Dela CruzNo ratings yet

- Practical Accounting Problems SolutionsDocument11 pagesPractical Accounting Problems SolutionsjustjadeNo ratings yet

- Lancaster University: January 2014 ExaminationsDocument6 pagesLancaster University: January 2014 Examinationswhaza7890% (1)

- Microsoft Word - I'm Secretly Married To A Big S - Light DanceDocument4,345 pagesMicrosoft Word - I'm Secretly Married To A Big S - Light DanceAliah LeaNo ratings yet

- Lord Kuthumi UnifiedTwinFlameGrid Bali2013 Ubud 5 Part11 StGermain 24-04-2013Document6 pagesLord Kuthumi UnifiedTwinFlameGrid Bali2013 Ubud 5 Part11 StGermain 24-04-2013Meaghan MathewsNo ratings yet

- Unique and Interactive EffectsDocument14 pagesUnique and Interactive EffectsbinepaNo ratings yet

- Arabic Letters Practice WorksheetsDocument3 pagesArabic Letters Practice Worksheetsvinsensius soneyNo ratings yet

- Decathlon - Retail Management UpdatedDocument15 pagesDecathlon - Retail Management UpdatedManu SrivastavaNo ratings yet

- RA MEWP 0003 Dec 2011Document3 pagesRA MEWP 0003 Dec 2011Anup George Thomas100% (1)

- 5 City Sheriff of Iligan City v. Fortunado (CANE)Document2 pages5 City Sheriff of Iligan City v. Fortunado (CANE)Jerry CaneNo ratings yet

- Florida SUS Matrix Guide 2020Document3 pagesFlorida SUS Matrix Guide 2020mortensenkNo ratings yet

- 4.1A. Satoshi Nakamoto and PeopleDocument58 pages4.1A. Satoshi Nakamoto and PeopleEman100% (1)

- Time Value of Money - TheoryDocument7 pagesTime Value of Money - TheoryNahidul Islam IUNo ratings yet

- Fta Checklist Group NV 7-6-09Document7 pagesFta Checklist Group NV 7-6-09initiative1972No ratings yet

- Comparing Education Systems WorldwideDocument22 pagesComparing Education Systems WorldwideJhing PacudanNo ratings yet

- Membership Form فہر ثھئگھتایDocument2 pagesMembership Form فہر ثھئگھتایETCNo ratings yet

- The Emergence of Provincial PoliticsDocument367 pagesThe Emergence of Provincial PoliticsHari Madhavan Krishna KumarNo ratings yet

- Musical Plays: in The PhilippinesDocument17 pagesMusical Plays: in The Philippinesgabby ilaganNo ratings yet

- KSDL RameshDocument10 pagesKSDL RameshRamesh KumarNo ratings yet

- Service Culture Module 2Document2 pagesService Culture Module 2Cedrick SedaNo ratings yet