Professional Documents

Culture Documents

CH 06 SM

Uploaded by

api-267019092Original Title

Copyright

Available Formats

Share this document

Did you find this document useful?

Is this content inappropriate?

Report this DocumentCopyright:

Available Formats

CH 06 SM

Uploaded by

api-267019092Copyright:

Available Formats

CHAPTER 6

DISCUSSION QUESTIONS

Q6-1. The basic objective of process costing is to

determine the costs of the products manufactured by the company. Determining the cost of

the products manufactured is necessary in

order to properly cost ending inventories for

external reporting purposes (i.e., reporting to

creditors and owners of the company, the

SEC, and the IRS) and to evaluate the profitability of the manufacturing activity. In order

to cost products, the costs must be determined for materials, labor, and factory overhead used to process each unit of product

through each department.

Q6-2. The products manufactured within a department (or cost center) during the period can be

heterogeneous if job order costing is used,

but must be homogeneous if process costing

is used. In job order costing, products are

accounted for in batches. The cost of each

unit of product manufactured on a job is determined by dividing the total cost charged to the

job by the number of units produced on the

job. Since the manufacturing cost of each job

is accounted for separately, accurate and

useful product cost can be determined even

when the products manufactured on different

jobs are substantially different. By contrast, in

process costing, all manufacturing costs are

charged to the department, and the unit cost

is determined by dividing the cost charged to

the department by the number of units produced. As a consequence, the units of product manufactured within a department must

be essentially alike in order for the cost allocated to each unit to be meaningful (i.e., to

reasonably reflect the actual cost of the

resources used to manufacture the product).

Q6-3. (a) Process

(b) Process, unless significantly different

models are manufactured

(c) Process

(d) Job order

(e) Process

(f) Process

(g) Job order

(h) Process, unless different fabrics are used

for different models, in which case the

conversion costs may be accounted for

using process, but the materials using job

order

Q6-4. Three product flow formats are: sequential,

parallel, and selective.

Sequential means that the product flows or is

manufactured in an unchanging fixed set of

operations, going from one department to the

next.

Parallel means that certain operational

phases take place simultaneously in other

departments and the partially completed units

or parts are brought together in subsequent

departments.

Selective refers to the fact that a product does

not necessarily move through every department. Depending upon the character or shape

of the final product, different departments are

engaged in completing the desired product.

Q6-5. Materials CostsIn job order costing, materials requisitions are used and charges are

made to jobs; in process costing, charges for

materials issued to production are made to

departments, with infrequent use of materials

requisitions.

Labor CostsTime tickets are used in job

order costing to accumulate labor costs for

each job; in process costing, labor costs are

charged to departments, and, therefore,

detailed time records are not necessary.

Factory OverheadJob order costing

requires the use of predetermined rates for

charging overhead to jobs; in process costing,

actual overhead may be used. (However, predetermined rates are often used in order to

smooth overhead that is not incurred at the

same rate as production activity.)

Summarizing CostsA job order cost sheet is

used to accumulate the costs of an order in job

order costing; a cost of production report is

used in process costing. In job order costing,

costs are summarized on completion of the

job; in process costing, costs charged to the

6-1

6-2

department and costs accounted for are summarized in the cost of production report each

month (or sometimes each week).

Q6-6. Predetermined overhead rates can and

should be used if the pattern of overhead cost

incurrence does not follow the pattern of production activity. Some items of overhead are

fixed and not responsive to changes in production activity. If production volume varies each

month, then predetermined overhead rates

should be used. Some items of overhead are

incurred only at certain times during the year,

but benefit production throughout the year

(e.g., payroll taxes, insurance, property taxes,

vacation pay, etc.). These items can be

recorded as prepaid expenses and amortized

uniformly to each month if actual overhead is

charged to production. Alternatively, estimates

of such costs can be included in the predetermined overhead rate, and the actual cost

charged to overhead when incurred. The use

of predetermined rates is often simpler than

the allocation of actual costs because a single

predetermined rate requires only one overhead charge to each department each month.

In contrast, the capitalization and amortization of each item of actual overhead would

require numerous charges each month.

Q6-7. A cost of production report is an effective

monthly (or weekly) summary of the cost of

materials, labor, and overhead consumed by

each department or cost center, along with a

record of the quantity of products manufactured.

It provides information necessary to cost

Chapter 6

products, prepare journal entries to record the

transfer of costs between departments, and

control costs.

Q6-8. The sections commonly found in a cost of production report are: (a) a quantity schedule

indicating the source and disposition of the

units of product, (b) a cost charged to the

department section, indicating the cost in total

and per unit for the cost transferred in from

the preceding department, as well as materials, labor and overhead charged to the

department, and (c) a cost accounted for section indicating the amount of cost assigned to

the units transferred out of the department, as

well as the cost of ending inventory.

Q6-9. Separate departmental cost of production

reports are used to accumulate costs more

accurately and to provide more detailed data

for cost control purposes than a plant-wide

cost of production report could provide. In

some cases (e.g., a manufacturing plant that

has a selective production flow for its products), a plant-wide cost of production report

cannot be used.

Q6-10. An equivalent unit of production is the amount

of a resource (e.g., materials, labor, or overhead) that would be required to complete one

unit of the product with respect to the cost element being considered. The total number of

equivalent units, with respect to a particular

element of cost, represents the number of

units of the product that could have been

completed with the resources used during the

period.

Chapter 6

6-3

EXERCISES

E6-1

(1)

Equivalent units transferred out .................

Equivalent units in ending inventory:

Cost from preceding department

(100% 5,000) ................................

Materials (100% 5,000) ....................

Labor (80% 5,000) ..............................

Factory overhead (60% 5,000) .........

Total equivalent units...................................

(2)

Cost in beginning inventory........................

Cost added during current period ..............

Total cost to be accounted for ....................

Divided by total equivalent units ................

Cost per equivalent unit ..............................

Cost from

Preceding

Department

20,000

Materials

Labor

Factory

Overhead

20,000

20,000

20,000

5,000

5,000

4,000

25,000

Cost from

Preceding

Department

0

$40,000

$40,000

25,000

$ 1.60

25,000

24,000

Materials

Labor

0

$15,000

$15,000

25,000

$

.60

E6-2

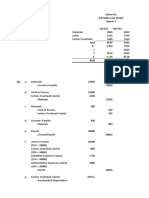

Work in ProcessDepartment X .............................................

Work in ProcessDepartment Y .............................................

Materials ........................................................................

0

$ 9,600

$ 9,600

24,000

$

.40

3,000

23,000

Factory

Overhead

0

$16,330

$16,330

23,000

$

.71

50,000

40,000

90,000

Work in ProcessDepartment X .............................................

Work in ProcessDepartment Y .............................................

Payroll ............................................................................

80,000

70,000

Work in ProcessDepartment X .............................................

Work in ProcessDepartment Y .............................................

Factory Overhead ........................................................

180,000

70,000

Work in ProcessDepartment Y .............................................

Work in ProcessDepartment X ................................

300,000

Finished Goods Inventory........................................................

Work in ProcessDepartment Y.................................

448,000

150,000

250,000

300,000

448,000

6-4

E6-3

Chapter 6

Tyndol Fabricators Inc.

Cutting and Forming Department

Cost of Production Report

For November

Quantity Schedule

Beginning inventory................................

Started in process this period ...............

Transferred to Assembling Department

Ending Inventory .....................................

Materials

Labor

75%

40%

Overhead

25%

Quantity

800

3,200

4,000

3,400

600

4,000

Cost Charged to Department

Beginning inventory:

Materials .....................................................................................

Labor ..........................................................................................

Factory overhead.......................................................................

Total cost in beginning inventory....................................

Total

Cost

$ 17,923

2,352

3,800

$ 24,075

Equivalent

Units*

Unit

Cost**

Cost added during current period:

Materials .....................................................................................

Labor...........................................................................................

Factory overhead.......................................................................

Total cost added during current period............................

Total cost charged to department ..................................................

$ 68,625

14,756

29,996

$113,377

$137,452

3,850

3,640

3,550

$22.48

4.70

9.52

Cost Accounted for as Follows

Transferred to Assembling Department

Work in Process, ending inventory:

Materials ............................................

Labor ..................................................

Factory overhead ..............................

Total cost accounted for ........................

Units

3,400

600

600

600

$36.70

%

Complete Unit Cost

100%

$36.70

75%

40%

25%

$22.48

4.70

9.52

Total Cost

$124,780

$10,116

1,128

1,428

12,672

$137,452

*Total number of equivalent units required in the cost accounted for section determined as follows:

Equivalent units transferred out ............

Equivalent units in ending inventory ....

Total equivalent units..............................

Materials

3,400

450

3,850

Labor

3,400

240

3,640

Overhead

3,400

150

3,550

** Total cost (i.e., the cost in beginning inventory plus the cost added during the current period)

divided by the total number of equivalent units required in the cost accounted for section

Chapter 6

E6-4

6-5

Tokyo Manufacturing Company

Molding Department

Cost of Production Report

For August

Quantity Schedule

Beginning inventory................................

Started in process this period ...............

Transferred to Finishing Department ....

Ending inventory .....................................

Materials

75%

Labor

25%

Overhead

25%

Quantity

1,000

9,000

10,000

9,200

800

10,000

Cost Charged to Department

Beginning inventory:

Materials .....................................................................................

Labor...........................................................................................

Factory overhead.......................................................................

Total cost in beginning inventory....................................

Total

Cost

$ 4,120

522

961

$ 5,603

Equivalent

Units*

Unit

Cost**

Cost added during current period:

Materials .....................................................................................

Labor...........................................................................................

Factory overhead.......................................................................

$39,980

12,638

18,779

9,800

9,400

9,400

$4.50

1.40

2.10

Total cost added during current period............................

Total cost charged to department ..................................................

$71,397

$77,000

$8.00

%

Complete Unit Cost

100%

$8.00

Total Cost

$73,600

Cost Accounted for as Follows

Transferred to Finishing Department ....

Work in Process, ending inventory:

Materials ..............................................

Labor ....................................................

Factory overhead ................................

Total cost accounted for ........................

Units

9,200

800

800

800

75%

25%

25%

$4.50

1.40

2.10

$2,700

280

420

3,400

$77,000

*Total number of equivalent units required in the cost accounted for section determined as follows:

Equivalent units transferred out .......

Equivalent units in ending inventory

Total equivalent units ........................

Materials

9,200

600

9,800

Labor

9,200

200

9,400

Overhead

9,200

200

9,400

** Total cost (i.e., the cost in beginning inventory plus the cost added during the current period)

divided by the total number of equivalent units required in the cost accounted for section

6-6

E6-5

Chapter 6

Stanislov Corporation

Forming Department

Cost of Production Report

For September

Quantity Schedule

Beginning inventory................................

Received from Cutting Department.......

Transferred to Painting Department ......

Ending inventory .....................................

Materials

60%

Labor

30%

Overhead

30%

Quantity

1,400

4,600

6,000

5,000

1,000

6,000

Cost Charged to Department

Beginning inventory:

Cost from preceding department.............................................

Materials ....................................................................................

Labor...........................................................................................

Factory overhead.......................................................................

Total cost in beginning inventory......................................

Total

Cost

$ 21,120

5,880

2,614

5,228

$ 34,842

Equivalent

Units*

Unit

Cost**

Cost added during current period:

Cost from preceding department.............................................

Materials .....................................................................................

Labor...........................................................................................

Factory overhead ......................................................................

Total cost added during current period............................

Total cost charged to department .................................................

$ 68,280

20,440

17,526

35,052

$141,298

$176,140

6,000

5,600

5,300

5,300

$14.90

4.70

3.80

7.60

Cost Accounted for as Follows

Transferred to Painting Department ......

Work in Process, ending inventory:

Cost from preceding department ....

Materials ............................................

Labor ..................................................

Factory overhead ..............................

Total cost accounted for.........................

Units

5,000

%

Complete

100%

Unit Cost

$31.00

1,000

1,000

1,000

1,000

100%

60%

30%

30%

$14.90

4.70

3.80

7.60

$31.00

Total Cost

$155,000

$14,900

2,820

1,140

2,280

21,140

$176,140

*Total number of equivalent units required in the cost accounted for section determined as follows:

Equivalent units transferred out ............

Equivalent units in ending inventory ....

Total equivalent units..............................

Prior Dept.

Cost

Materials

5,000

5,000

1,000

600

6,000

5,600

Labor

5,000

300

5,300

Overhead

5,000

300

5,300

** Total cost (i.e., the cost in beginning inventory plus the cost added during the current period)

divided by the total number of equivalent units required in the cost accounted for section

Chapter 6

E6-6

6-7

Sonneli Corporation

Assembly Department

Cost of Production Report

For February

Quantity Schedule

Beginning inventory................................

Received from Cutting Department.......

Transferred to Finished Goods ..............

Ending inventory ....................................

Materials

80%

Labor

60%

Cost Charged to Department

Beginning inventory:

Overhead

60%

Total

Cost

Cost from preceding department.............................................

Materials .....................................................................................

Labor ..........................................................................................

Factory overhead.......................................................................

Total cost in beginning inventory......................................

$11,800

4,000

1,200

2,400

$19,400

Cost added during current period:

Cost from preceding department.............................................

Materials .....................................................................................

Labor ..........................................................................................

Factory overhead ......................................................................

Total cost added during current period ..........................

Total cost charged to department ..................................................

$63,200

21,200

17,660

35,320

$137,380

$156,780

Cost Accounted for as Follows

Transferred to Finished Goods ..............

Work in Process, ending inventory:

Cost from preceding department ....

Materials ............................................

Labor ..................................................

Factory overhead ..............................

Total cost accounted for.........................

Units

2,000

500

500

500

500

Quantity

400

2,100

2,500

2,000

500

2,500

Equivalent

Units*

Unit

Cost**

2,500

2,400

2,300

2,300

$30.00

10.50

8.20

16.40

$65.10

%

Complete Unit Cost

100%

$65.10

100%

80%

60%

60%

$30.00

10.50

8.20

16.40

Total Cost

$130,200

$15,000

4,200

2,460

4,920

26,580

$156,780

*Total number of equivalent units required in the cost accounted for section determined as follows:

Equivalent units transferred out ............

Equivalent units in ending inventory ....

Total equivalent units..............................

Prior Dept.

Cost

Materials

2,000

2,000

500

400

2,500

2,400

Labor

2,000

300

2,300

Overhead

2,000

300

2,300

** Total cost (i.e., the cost in beginning inventory plus the cost added during the current period)

divided by the total number of equivalent units required in the cost accounted for section

6-8

E6-7

Chapter 6

Saleri Manufacturing Corporation

Forming Department

Cost of Production Report

For June

Quantity Schedule

Beginning inventory................................

Received from Cutting Department.......

Transferred to Finishing Department ....

Ending inventory .....................................

Material A

100%

Material B

0%

Labor

30%

Overhead

30%

Quantity

600

3,900

4,500

4,100

400

4,500

Cost Charged to Department

Beginning inventory:

Cost from preceding department.............................................

Material A ...................................................................................

Material B ...................................................................................

Labor...........................................................................................

Factory overhead.......................................................................

Total cost in beginning inventory ....................................

Total

Cost

$ 4,422

2,805

0

1,250

1,875

10,352

Equivalent

Units*

Unit

Cost**

Cost added during current period:

Cost from preceding department.............................................

Material A ...................................................................................

Material B ...................................................................................

Labor...........................................................................................

Factory overhead ......................................................................

Total cost added during current period............................

Total cost charged to department ..................................................

$ 29,328

19,695

10,250

15,630

23,445

$ 98,348

$108,700

4,500

4,500

4,100

4,220

4,220

$ 7.50

5.00

2.50

4.00

6.00

Cost Accounted for as Follows

Transferred to Finishing Department ....

Work in Process, ending inventory:

Cost from preceding department ....

Material A ..........................................

Material B ..........................................

Labor ..................................................

Factory overhead .............................

Total cost accounted for ........................

Units

4,100

400

400

400

400

400

$25.00

%

Complete Unit Cost

100%

$25.00

100%

100%

0%

30%

30%

$7.50

5.00

2.50

4.00

6.00

Total Cost

$102,500

$3,000

2,000

0

480

720

6,200

$108,700

*Total number of equivalent units required in the cost accounted for section determined as follows:

Equivalent units transferred out ............

Equivalent units in ending inventory ....

Total equivalent units..............................

Prior Dept.

Cost

Material A

4,100

4,100

400

400

4,500

4,500

Material B

4,100

0

4,100

Labor

4,100

120

4,220

Overhead

4,100

120

4,220

** Total cost (i.e., the cost in beginning inventory plus the cost added during the current period)

divided by the total number of equivalent units required in the cost accounted for section

Chapter 6

E6-8

6-9

Canoli Cola Company

Carbonation Department

Cost of Production Report

For October

Quantity Schedule

Beginning inventory ................................................

Received from Syrup Department ..........................

Added to process in Carbonation Department .....

Transferred to Bottling Department .......................

Ending inventory ......................................................

Materials

100%

Cost Charged to Department

Beginning inventory:

Cost from preceding department ...........................................

Materials .....................................................................................

Labor ..........................................................................................

Factory overhead.......................................................................

Total cost in beginning inventory ....................................

Cost added during current period:

Cost from preceding department.............................................

Materials .....................................................................................

Labor...........................................................................................

Factory overhead.......................................................................

Total cost added during current period............................

Total cost charged to department ..................................................

Cost Accounted for as Follows

Transferred to Bottling Department ......

Work in Process, ending inventory:

Cost from preceding department ....

Materials ...........................................

Labor ..................................................

Factory overhead .............................

Total cost accounted for ........................

Units

7,800

1,200

1,200

1,200

1,200

Labor

25%

Overhead

25%

7,800

1,200

9,000

Total

Cost

$ 1,120

140

65

120

$ 1,445

Equivalent

Units*

Unit

Cost**

$ 9,680

1,210

1,960

3,120

$15,970

$17,415

9,000

9,000

8,100

8,100

$1.20

.15

.25

.40

$2.00

%

Complete Unit Cost

100%

$2.00

100%

100%

25%

25%

Quantity

1,000

2,000

6,000

9,000

$1.20

.15

.25

.40

Total Cost

$15,600

$1,440

180

75

120

1,815

$17,415

*Total number of equivalent units required in the cost accounted for section determined as follows:

Equivalent units transferred out ............

Equivalent units in ending inventory ....

Total equivalent units..............................

Prior Dept.

Cost

Materials

7,800

7,800

1,200

1,200

9,000

9,000

Labor

7,800

300

8,100

Overhead

7,800

300

8,100

** Total cost (i.e., the cost in beginning inventory plus the cost added during the current period)

divided by the total number of equivalent units required in the cost accounted for section

6-10

E6-9

Chapter 6

Menezes Chemical Company

Blending Department

Cost of Production Report

For March

Quantity Schedule

Beginning inventory .................................................

Received from Refining Department ......................

Added to process in Blending Department ...........

Transferred to Finishing Department .....................

Ending inventory ......................................................

Materials

100%

Cost Charged to Department

Beginning inventory:

Cost from preceding department.............................................

Materials .....................................................................................

Labor...........................................................................................

Factory overhead.......................................................................

Total cost in beginning inventory ....................................

Cost added during current period:

Cost from preceding department.............................................

Materials .....................................................................................

Labor ..........................................................................................

Factory overhead.......................................................................

Total cost added during current period............................

Total cost charged to department ..................................................

Cost Accounted for as Follows

Transferred to Finishing Department ....

Work in Process, ending inventory:

Cost from preceding department ....

Materials ............................................

Labor ..................................................

Factory overhead ..............................

Total cost accounted for.........................

Units

26,000

4,000

4,000

4,000

4,000

Labor

Overhead

80%

90%

26,000

4,000

30,000

Total

Cost

$4,750

2,415

180

787

$8,112

Equivalent

Units*

Unit

Cost**

$25,250

12,885

2,740

8,113

$48,988

$57,100

30,000

30,000

29,200

29,600

$1.00

.51

.10

.30

$1.91

%

Complete Unit Cost

100%

$1.91

100%

100%

80%

90%

Quantity

5,000

20,000

5,000

30,000

$1.00

.51

.10

.30

Total Cost

$49,660

$4,000

2,040

320

1,080

7,440

$57,100

*Total number of equivalent units required in the cost accounted for section determined as follows:

Equivalent units transferred out ............

Equivalent units in ending inventory ....

Total equivalent units..............................

Prior Dept.

Cost

Materials

26,000

26,000

4,000

4,000

30,000

30,000

Labor

26,000

3,200

29,200

Overhead

26,000

3,600

29,600

** Total cost (i.e., the cost in beginning inventory plus the cost added during the current period)

divided by the total number of equivalent units required in the cost accounted for section

Chapter 6

6-11

E6-10 APPENDIX

Shankar Manufacturing Company

Cutting Department

Cost of Production Report

For July

Quantity Schedule

Beginning inventory................................

Started in process this period ...............

Transferred to Assembly Department ...

Ending inventory .....................................

Materials

60%

100%

Labor

20%

60%

Cost Charged to Department

Beginning inventory:

Materials .....................................................................................

Labor...........................................................................................

Factory overhead ......................................................................

Total cost in beginning inventory......................................

Cost added during current period:

Materials .....................................................................................

Labor...........................................................................................

Factory overhead.......................................................................

Total cost added during current period............................

Total cost charged to department ..................................................

Cost Accounted for as Follows

Transferred to Assembly Department:

Beginning inventory ........................

Cost to complete:

Materials ...............................

Labor .....................................

Factory overhead .................

Started and completed this period .

Total cost transferred to Assembly

Department ................................

Work in Process, ending inventory:

Materials ............................................

Labor ..................................................

Factory overhead .............................

Total cost accounted for ........................

Units

Overhead

20%

50%

Total

Cost

$2,940

390

585

$3,915

$46,530

18,860

27,150

$92,540

$96,455

Quantity

100

900

1,000

850

150

1,000

Equivalent

Units*

Unit

Cost**

940

920

905

$49.50

20.50

30.00

$100.00

Current % Unit Cost

Total Cost

$3,915

100

100

100

750

40%

80%

80%

100%

$49.50

20.50

30.00

100.00

1,980

1,640

2,400

$ 9,935

75,000

$84,935

150

150

150

100%

60%

50%

$49.50

20.50

30.00

$7,425

1,845

2,250

11,520

$96,455

*Number of equivalent units of cost added during the current period determined as follows:

To complete beginning inventory ..........

Started and completed this period........

Ending inventory .....................................

Total equivalent units..............................

Materials

40

750

150

940

Labor

80

750

90

920

Overhead

80

750

75

905

** Cost added during the current period divided by the number of equivalent units of cost added during the current period

6-12

Chapter 6

E6-11 APPENDIX

Cantach Tool Company

Assembly Department

Cost of Production Report

For November

Quantity Schedule

Beginning inventory................................

Received from Cutting Department.......

Transferred to Finished Goods ..............

Ending inventory .....................................

Materials

50%

90%

Labor

40%

80%

Cost Charged to Department

Beginning inventory:

Cost from preceding department...........................................

Materials .....................................................................................

Labor...........................................................................................

Factory overhead.......................................................................

Total cost in beginning inventory....................................

Cost added during current period:

Cost from preceding department.............................................

Materials .....................................................................................

Labor...........................................................................................

Factory overhead.......................................................................

Total cost added during current period............................

Total cost charged to department ..................................................

Overhead

40%

80%

Quantity

1,200

2,800

4,000

3,000

1,000

4,000

Total

Cost

$ 17,280

5,550

2,400

3,600

$ 28,830

Equivalent

Units*

Unit

Cost**

$ 40,600

29,700

16,932

25,398

$112,630

$141,460

2,800

3,300

3,320

3,320

$14.50

9.00

5.10

7.65

$36.25

Chapter 6

6-13

E6-11 APPENDIX (Concluded)

Cost Accounted for as Follows

Transferred to Finished Goods:

Beginning inventory .........................

Cost to complete:

Materials ...............................

Labor .....................................

Factory overhead .................

Started and completed this period

Total cost transferred to Finished Goods

Work in Process, ending inventory:

Cost from preceding department ....

Materials ............................................

Labor .................................................

Factory overhead ..............................

Total cost accounted for ........................

Units

Current % Unit Cost

Total Cost

$28,830

1,200

1,200

1,200

1,800

50%

60%

60%

100%

$9.00

5.10

7.65

36.25

1,000

1,000

1,000

1,000

100%

90%

80%

80%

$14.50

9.00

5.10

7.65

5,400

3,672

5,508

$14,500

8,100

4,080

6,120

$ 43,410

65,250

$108,660

32,800

$141,460

*Number of equivalent units of cost added during the current period determined as follows:

To complete beginning inventory ..........

Started and completed this period........

Ending inventory .....................................

Total equivalent units..............................

Prior Dept.

Cost

Materials

0

600

1,800

1,800

1,000

900

2,800

3,300

Labor

720

1,800

800

3,320

Overhead

720

1,800

800

3,320

** Cost added during the current period divided by the number of equivalent units of cost added during the current period

6-14

Chapter 6

E6-12 APPENDIX

Southwell Chemical Corporation

Blending Department

Cost of Production Report

For May

Quantity Schedule

Beginning inventory................................

Received from Refining Department .....

Added to process in Blending Department

Transferred to Finished Goods .............

Ending inventory .....................................

Materials

100%

100%

Cost Charged to Department

Beginning inventory:

Cost from preceding department.............................................

Materials .....................................................................................

Labor...........................................................................................

Factory overhead.......................................................................

Total cost in beginning inventory......................................

Cost added during current period:

Cost from preceding department.............................................

Materials .....................................................................................

Labor...........................................................................................

Factory overhead.......................................................................

Total cost added during current period............................

Total cost charged to department ..................................................

Labor

20%

60%

Overhead

40%

80%

Quantity

2,000

5,000

5,000

12,000

10,500

1,500

12,000

Total

Cost

$2,460

500

150

600

$3,710

Equivalent

Units*

Unit

Cost**

$12,500

2,500

3,300

7,630

$25,930

$29,640

10,000

10,000

11,000

10,900

$1.25

.25

.30

.70

$2.50

Chapter 6

6-15

E6-12 APPENDIX (Concluded)

Cost Accounted for as Follows

Transferred to Finished Goods:

Beginning inventory .........................

Cost to complete:

Materials ...............................

Labor ....................................

Factory overhead .................

Started and completed this period

Total cost transferred to Finished

Goods ..........................................

Work in Process, ending inventory:

Cost from preceding department ....

Materials ............................................

Labor ..................................................

Factory overhead ..............................

Total cost accounted for ........................

Units

Current % Unit Cost

Total Cost

$3,710

2,000

2,000

2,000

8,500

0%

80%

60%

100%

$ .25

.30

.70

2.50

0

480

840

$ 5,030

21,250

$26,280

1,500

1,500

1,500

1,500

100%

100%

60%

80%

$1.25

.25

.30

.70

$1,875

375

270

840

3,360

$29,640

*Number of equivalent units of cost added during the current period determined as follows:

To complete beginning inventory ..........

Started and completed this period........

Ending inventory .....................................

Total equivalent units..............................

Prior Dept.

Cost

Materials

0

0

8,500

8,500

1,500

1,500

10,000

10,000

Labor

1,600

8,500

900

11,000

Overhead

1,200

8,500

1,200

10,900

** Cost added during the current period divided by the number of equivalent units of cost added during the current period

6-16

Chapter 6

PROBLEMS

P6-1

(1)

Meninquez Cabinet Company

Cutting Department

Cost of Production Report

For August

Quantity Schedule

Beginning inventory................................

Started in process this period ..............

Transferred to Assembly Department ...

Ending inventory .....................................

Materials

90%.

Labor

60%

Cost Charged to Department

Beginning inventory:

Materials .....................................................................................

Labor...........................................................................................

Factory overhead.......................................................................

Total cost in beginning inventor........................................

Cost added during current period:

Materials .....................................................................................

Labor...........................................................................................

Factory overhead.......................................................................

Total cost added during current period............................

Total cost charged to department ..................................................

Cost Accounted for as Follows

Transferred to Assembly Department ...

Work in Process, ending inventory:

Materials ............................................

Labor ..................................................

Factory overhead ..............................

Total cost accounted for.........................

Units

650

150

150

150

Overhead

60%

Total

Cost

$ 5,365

530

795

$6,690

$26,035

8,350

12,525

$46,910

$53,600

Quantity

200

600

800

650

150

800

Equivalent

Units*

785

740

740

$40.00

12.00

18.00

$ 40.00

12.00

18.00

$ 70.00

%

Complete Unit Cost

100%

$70.00

90%

60%

60%

Unit

Cost**

Total Cost

$45,500

$5,400

1,080

1,620

8,100

$53,600

*Total number of equivalent units required in the cost accounted for section determined as follows:

Equivalent units transferred out .....

Equivalent units in ending inventory

Total equivalent units .......................

Materials

650

135

785

Labor

650

90

740

Overhead

650

90

740

** Total cost (i.e., the cost in beginning inventory plus the cost added during the current period)

divided by the total number of equivalent units required in the cost accounted for section

Chapter 6

6-17

P6-1 (Continued)

Meninquez Cabinet Company

Assembly Department

Cost of Production Report

For August

Quantity Schedule

Beginning inventory................................

Received from Cutting Department.......

Transferred to Finished Goods ..............

Ending inventory .....................................

Materials

Labor

Overhead

40%

20%

20%

Cost Charged to Department

Beginning inventory:

Cost from preceding department ...........................................

Materials ....................................................................................

Labor...........................................................................................

Factory overhead.......................................................................

Total cost in beginning inventory ....................................

Cost added during current period:

Cost from preceding department.............................................

Materials ....................................................................................

Labor...........................................................................................

Factory overhead.......................................................................

Total cost added during current period .........................

Total cost charged to department ..................................................

Total

Cost

$ 17,410

3,451

3,611

3,611

$ 28,083

$ 45,500

14,273

20,989

20,989

$101,751

$129,834

Quantity

250

650

900

800

100

900

Equivalent

Units*

900

840

820

820

Unit

Cost**

$ 69.90

21.10

30.00

30.00

$151.00

6-18

Chapter 6

P6-1 (Concluded)

Cost Accounted for as Follows

Transferred to Finished Goods ..............

Work in Process, ending inventory:

Cost from preceding department ....

Materials ............................................

Labor ..................................................

Factory overhead ..............................

Total cost accounted for ........................

Units

800

100

100

100

100

%

Complete Unit Cost

100%

$151.00

100%

40%

20%

20%

$69.90

21.10

30.00

30.00

Total Cost

$120,800

$6,990

844

600

600

9,034

$129,834

*Total number of equivalent units required in the cost accounted for section determined as follows:

Equivalent units transferred out .....

Equivalent units in ending inventory

Total equivalent units .......................

Prior Dept.

Cost

Materials

800

800

100

40

900

840

Labor

800

20

820

Overhead

800

20

820

** Total cost (i.e., the cost in beginning inventory plus the cost added during the current period)

divided by the total number of equivalent units required in the cost accounted for section

(2)

Work in ProcessCutting Department ......................

Work in ProcessAssembly Department ..................

Materials ..............................................................

26,035

14,273

Work in ProcessCutting Department ......................

Work in ProcessAssembly Department ..................

Payroll ..................................................................

8,350

20,989

Work in ProcessCutting Department ......................

Work in ProcessAssembly Department ..................

Applied Factory Overhead..................................

12,525

20,989

Work in ProcessAssembly Department ..................

Work in ProcessCutting Department .............

45,500

Finished Goods Inventory ...........................................

Work in ProcessAssembly Department ........

120,800

40,308

29,339

33,514

45,500

120,800

Chapter 6

P6-2

(1)

6-19

Rimirez Tool Corporation

Casting Department

Cost of Production Report

For December

Quantity Schedule

Materials

Labor

Overhead

Beginning inventory................................

Started in process this period ..............

Transferred to Finishing Department ....

Ending inventory .....................................

1,000

8,000

9,000

100%

80%

Cost Charged to Department

Beginning inventory:

Materials .....................................................................................

Labor...........................................................................................

Factory overhead.......................................................................

Total cost in beginning inventory......................................

Cost added during current period:

Materials .....................................................................................

Labor...........................................................................................

Factory overhead.......................................................................

Total cost added during current period............................

Total cost charged to department ..................................................

Cost Accounted for as Follows

Transferred to Finishing Department ....

Work in Process, ending inventory:

Materials ............................................

Labor ..................................................

Factory overhead ..............................

Total cost accounted for ........................

Quantity

Units

7,500

1,500

1,500

1,500

80%

7,500

1,500

9,000

Total

Cost

$915

60

90

$ 1,085

Equivalent

Units*

Unit

Cost**

$17,085

4,290

6,435

$27,810

$28,875

9,000

8,700

8,700

$2.00

.50

.75

$3.25

%

Complete Unit Cost

100%

$3.25

100%

80%

80%

$2.00

.50

.75

Total Cost

$24,375

$3,000

600

900

4,500

$28,875

*Total number of equivalent units required in the cost accounted for section determined as follows:

Equivalent units transferred out .............................

Equivalent units in ending inventory......................

Total equivalent units ...............................................

Materials

7,500

1,500

9,000

Labor

7,500

1,200

8,700

Overhead

7,500

1,200

8,700

** Total cost (i.e., the cost in beginning inventory plus the cost added during the current period)

divided by the total number of equivalent units required in the cost accounted for section

6-20

Chapter 6

P6-2 (Continued)

Rimirez Tool Corporation

Finishing Department

Cost of Production Report

For December

Quantity Schedule

Labor

Overhead

Beginning inventory

Received from Casting Department .........................

Transferred to Finished Goods ................................

Ending inventory ........................................................

Quantity

1,500

7,500

9,000

40%

Cost Charged to Department

Beginning inventory:

Cost from preceding department.............................................

Labor...........................................................................................

Factory overhead ......................................................................

Total cost in beginning inventory......................................

Cost added during current period:

Cost from preceding department.............................................

Labor...........................................................................................

Factory overhead.......................................................................

Total cost added during current period............................

Total cost charged to department ..................................................

50%

7,000

2,000

9,000

Total

Cost

$ 4,785

201

555

$ 5,541

Equivalent

Units*

Unit

Cost**

$24,375

2,919

3,125

$30,419

$35,960

9,000

7,800

8,000

$3.24

.40

.46

$4.10

Chapter 6

6-21

P6-2 (Concluded)

Cost Accounted for as Follows

Transferred to Finished Goods ..............

Work in Process, ending inventory:

Cost from preceding department ....

Labor ..................................................

Factory overhead ..............................

Total cost accounted for.........................

Units

7,000

2,000

2,000

2,000

%

Complete Unit Cost

100%

$4.10

100%

40%

50%

$3.24

.40

.46

Total Cost

$28,700

$6,480

320

460

7,260

$35,960

*Total number of equivalent units required in the cost accounted for section determined as follows:

Equivalent units transferred out.........................

Equivalent units in ending inventory .................

Total equivalent units .........................................

Prior Dept.

Cost

7,000

2,000

9,000

Labor

7,000

800

7,800

Overhead

7,000

1,000

8,000

** Total cost (i.e., the cost in beginning inventory plus the cost added during the current period)

divided by the total number of equivalent units required in the cost accounted for section

(2)

Work in ProcessCasting Department......................

Materials ..............................................................

17,085

Work in ProcessCasting Department......................

Work in ProcessFinishing Department...................

Payroll ..................................................................

4,290

2,919

Work in ProcessCasting Department......................

Work in ProcessFinishing Department...................

Applied Factory Overhead..................................

6,435

3,125

Work in ProcessFinishing Department...................

Work in ProcessCasting Department ............

24,375

Finished Goods Inventory ...........................................

Work in ProcessFinishing Department..........

28,700

17,085

7,209

9,560

24,375

28,700

6-22

P6-3

(1)

Chapter 6

Jetter Engine Corporation

Casting Department

Cost of Production Report

For February

Quantity Schedule

Beginning inventory................................

Started in process this period ...............

Transferred to Assembly Department ...

Ending inventory .....................................

Materials

100%

Labor

80%

Cost Charged to Department

Beginning inventory:

Materials .....................................................................................

Labor...........................................................................................

Factory overhead ......................................................................

Total cost in beginning inventory......................................

Cost added during current period:

Materials .....................................................................................

Labor...........................................................................................

Factory overhead.......................................................................

Total cost added during current period............................

Total cost charged to department ..................................................

Cost Accounted for as Follows

Transferred to Assembly Department ...

Work in Process, ending inventory:

Materials ...........................................

Labor ..................................................

Factory overhead ..............................

Total cost accounted for.........................

Units

2,700

800

800

800

Overhead

90%

Quantity

500

3,000

3,500

2,700

800

3,500

Total

Cost

$ 10,925

338

2,839

$ 14,102

Equivalent

Units*

$146,575

16,362

48,461

$211,398

$225,500

3,500

3,340

3,420

%

Complete Unit Cost

100%

$65.00

100%

80%

90%

$45.00

5.00

15.00

Unit

Cost**

45.00

5.00

15.00

65.00

Total Cost

$175,500

$36,000

3,200

10,800

50,000

$225,500

*Total number of equivalent units required in the cost accounted for section determined as follows:

Equivalent units transferred out ...............................

Equivalent units in ending inventory........................

Total equivalent units ................................................

Materials

2,700

800

3,500

Labor

2,700

640

3,340

Overhead

2,700

720

3,420

** Total cost (i.e., the cost in beginning inventory plus the cost added during the current period)

divided by the total number of equivalent units required in the cost accounted for section

Chapter 6

6-23

P6-3 (Continued)

Jetter Engine Corporation

Assembly Department

Cost of Production Report

For February

Quantity Schedule

Beginning inventory................................

Received from Casting Department .....

Transferred to Finishing Department ....

Ending inventory .....................................

Materials

70%

Labor

30%

Cost Charged to Department

Beginning inventory:

Cost from preceding department ...........................................

Materials .....................................................................................

Labor ..........................................................................................

Factory overhead ......................................................................

Total cost in beginning inventory....................................

Cost added during current period:

Cost from preceding department.............................................

Materials .....................................................................................

Labor...........................................................................................

Factory overhead.......................................................................

Total cost added during current period............................

Total cost charged to department .................................................

Cost Accounted for as Follows

Transferred to Finishing Department ....

Work in Process, ending inventory

Cost from preceding department ....

Materials ............................................

Labor ..................................................

Factory overhead ..............................

Total cost accounted for.........................

Units

2,900

800

800

800

800

Overhead

30%

Quantity

1,000

2,700

3,700

2,900

800

3,700

Total

Cost

$ 63,150

40,258

12,426

12,426

$128,260

Equivalent

Units*

Unit

Cost**

$175,500

116,480

44,408

44,408

$380,796

$509,056

3,700

3,460

3,140

3,140

$64.50

45.30

18.10

18.10

$146.00

%

Complete Unit Cost

100%

$146.00

100%

70%

30%

30%

64.50

45.30

18.10

18.10

Total Cost

$423,400

$51,600

25,368

4,344

4,344

85,656

$509,056

*Total number of equivalent units required in the cost accounted for section determined as follows:

Equivalent units transferred out ............

Equivalent units in ending inventory ....

Total equivalent units..............................

Prior Dept.

Cost

Materials

2,900

2,900

800

560

3,700

3,460

Labor

2,900

240

3,140

Overhead

2,900

240

3,140

** Total cost (i.e., the cost in beginning inventory plus the cost added during the current period)

divided by the total number of equivalent units required in the cost accounted for section

6-24

Chapter 6

P6-3 (Continued)

Jetter Engine Corporation

Finishing Department

Cost of Production Report

For February

Quantity Schedule

Beginning inventory ...................................................

Received from Assembly Department ......................

Transferred to Finished Goods ................................

Ending inventory.........................................................

Labor

50%

Cost Charged to Department

Beginning inventory:

Cost from preceding department.............................................

Labor...........................................................................................

Factory overhead.......................................................................

Total cost in beginning inventory ...................................

Cost added during current period:

Cost from preceding department.............................................

Labor...........................................................................................

Factory overhead.......................................................................

Total cost added during current period............................

Total cost charged to department .................................................

Cost Accounted for as Follows

Transferred to Finished Goods ..............

Work in Process, ending inventory:

Cost from preceding department ....

Labor ..................................................

Factory overhead ..............................

Total cost accounted for.........................

Units

2,800

400

400

400

Overhead

50%

Quantity

300

2,900

3,200

2,800

400

3,200

Total

Cost

$ 42,840

2,760

4,140

$ 49,740

Equivalent

Units*

$423,400

12,240

18,360

$454,000

$503,740

3,200

3,000

3,000

$ 145.70

5.00

7.50

$ 145.70

5.00

7.50

$ 158.20

%

Complete Unit Cost

100%

$ 158.20

100%

50%

50%

Unit

Cost**

Total Cost

$442,960

$58,280

1,000

1,500

60,780

$503,740

*Total number of equivalent units required in the cost accounted for section determined as follows:

Equivalent units transferred out ...............................

Equivalent units in ending inventory........................

Total equivalent units .................................................

Prior Dept.

Cost

2,800

400

3,200

Labor

2,800

200

3,000

Overhead

2,800

200

3,000

** Total cost (i.e., the cost in beginning inventory plus the cost added during the current period)

divided by the total number of equivalent units required in the cost accounted for section

Chapter 6

6-25

P6-3 (Concluded)

(2)

Work in ProcessCasting Department......................

Work in ProcessAssembly Department ..................

Materials ...............................................................

146,575

116,480

Work in ProcessCasting Department......................

Work in ProcessAssembly Department ..................

Work in ProcessFinishing Department...................

Payroll ..................................................................

16,362

44,408

12,240

Work in ProcessCasting Department......................

Work in ProcessAssembly Department ..................

Work in ProcessFinishing Department...................

Applied Factory Overhead..................................

48,461

44,408

18,360

Work in ProcessAssembly Department ..................

Work in ProcessCasting Department.............

175,500

Work in ProcessFinishing Department...................

Work in ProcessAssembly Department .........

423,400

Finished Goods inventory ...........................................

Work in ProcessFinishing Department..........

442,960

263,055

73,010

111,229

175,500

423,400

442,960

6-26

P6-4

(1)

Chapter 6

Peneli Cologne Company

Blending Department

Cost of Production Report

For June

Quantity Schedule

Beginning inventory................................

Started in process this period ...............

Transferred to Finishing Department ....

Ending inventory .....................................

Materials

60%

Labor

20%

Cost Charged to Department

Beginning inventory:

Materials .....................................................................................

Labor...........................................................................................

Factory overhead.......................................................................

Total cost in beginning inventory......................................

Cost added during current period:

Materials .....................................................................................

Labor...........................................................................................

Factory overhead.......................................................................

Total cost added during current period ...........................

Total cost charged to department .................................................

Cost Accounted for as Follows

Transferred to Finishing Department ....

Work in Process, ending inventory:

Materials ............................................

Labor ..................................................

Factory overhead ..............................

Total cost accounted for.........................

Units

6,400

600

600

600

Overhead

25%

Quantity

1,000

6,000

7,000

6,400

600

7,000

Total

Cost

$ 19,620

944

2,375

$ 22,939

Equivalent

Units*

Unit

Cost**

$129,100

6,880

29,065

$165,045

$187,984

6,760

6,520

6,550

$22.00

1.20

4.80

$28.00

%

Complete Unit Cost

100%

$28.00

60%

20%

25%

$22.00

1.20

4.80

Total Cost

$179,200

$7,920

144

720

8,784

$187,984

*Total number of equivalent units required in the cost accounted for section determined as follows:

Equivalent units transferred out.........................

Equivalent units in ending inventory .................

Total equivalent units...........................................

Materials

6,400

360

6,760

Labor

6,400

120

6,520

Overhead

6,400

150

6,550

** Total cost (i.e., the cost in beginning inventory plus the cost added during the current period)

divided by the total number of equivalent units required in the cost accounted for section

Chapter 6

6-27

P6-4 (Continued)

Peneli Cologne Company

Finishing Department

Cost of Production Report

For June

Quantity Schedule

Beginning inventory ...................................................

Received from Blending Department ......................

Added to process in Finishing Department.............

Transferred to Finished Goods .................................

Ending inventory .......................................................

Materials

100%

Cost Charged to Department

Beginning inventory:

Cost from preceding department ...........................................

Materials .....................................................................................

Labor...........................................................................................

Factory overhead.......................................................................

Total cost in beginning inventory......................................

Cost added during current period:

Cost from preceding department.............................................

Materials .....................................................................................

Labor...........................................................................................

Factory overhead.......................................................................

Total cost added during current period............................

Total cost charged to department ..................................................

Labor

70%

Overhead

70%

Quantity

1,400

6,400

19,200

27,000

26,000

1,000

27,000

Total

Cost

$ 8,450

1,395

106

659

$ 10,610

Equivalent

Units*

Unit

Cost**

$179,200

28,305

19,919

60,751

$288,175

$298,785

27,000

27,000

26,700

26,700

$ 6.95

1.10

.75

2.30

$11.10

6-28

Chapter 6

P6-4 (Concluded)

Cost Accounted for as Follows

Transferred to Finished Goods ..............

Work in Process, ending inventory:

Cost from preceding department ....

Materials ............................................

Labor ..................................................

Factory overhead ..............................

Total cost accounted for ........................

Units

26,000

1,000

1,000

1,000

1,000

%

Complete Unit Cost

100%

$11.10

100%

100%

70%

70%

$ 6.95

1.10

.75

2.30

Total Cost

$288,600

$6,950

1,100

525

1,610

10,185

$298,785

*Total number of equivalent units required in the cost accounted for section determined as follows:

Equivalent units transferred out ............

Equivalent units in ending inventory ....

Total equivalent units..............................

Prior Dept.

Cost

Materials

26,000

26,000

1,000

1,000

27,000

27,000

Labor

26,000

700

26,700

Overhead

26,000

700

26,700

** Total cost (i.e., the cost in beginning inventory plus the cost added during the current period)

divided by the total number of equivalent units required in the cost accounted for section

(2)

Work in ProcessBlending Department ...................

Work in ProcessFinishing Department...................

Materials ..............................................................

129,100

28,305

Work in ProcessBlending Department ...................

Work in ProcessFinishing Department...................

Payroll ...................................................................

6,880

19,919

Work in ProcessBlending Department ...................

Work in ProcessFinishing Department...................

Applied Factory Overhead .................................

29,065

60,751

Work in ProcessFinishing Department...................

Work in ProcessBlending Department ..........

179,200

Finished Goods inventory ...........................................

Work in ProcessFinishing Department..........

288,600

157,405