You might also like

- IM Ch14-7e - WRLDocument25 pagesIM Ch14-7e - WRLCharry RamosNo ratings yet

- Solution Manual For Practical Financial Management 8th Edition by LasherDocument6 pagesSolution Manual For Practical Financial Management 8th Edition by Lashera161631812No ratings yet

- 12 LasherIM Ch12Document23 pages12 LasherIM Ch12asgharhamid75% (4)

- Capital Budgeting Techniques and Discounted Cash Flow AnalysisDocument30 pagesCapital Budgeting Techniques and Discounted Cash Flow AnalysisErica Mae Vista100% (1)

- Financial Planning Techniques and AssumptionsDocument30 pagesFinancial Planning Techniques and AssumptionsCharmaine Gamban100% (2)

- 15 LasherIM Ch15Document14 pages15 LasherIM Ch15advaniamrita67% (3)

- Analyze Cash Flows and Financial RatiosDocument49 pagesAnalyze Cash Flows and Financial RatiosAnonymous Lih1laax0% (1)

- Financial Management Chap16 William LasherDocument24 pagesFinancial Management Chap16 William LasherMichelle de Guzman100% (3)

- 08 LasherIM Ch08Document20 pages08 LasherIM Ch08Ed Donaldy100% (2)

- 07 LasherIM Ch07Document29 pages07 LasherIM Ch07Mohamed El Ghandour100% (1)

- 03 LasherIM Ch03Document47 pages03 LasherIM Ch03Maryam Bano100% (5)

- 11 LasherIM Ch11Document26 pages11 LasherIM Ch11Goran Gothai75% (4)

- Chapter 13 - HW With SolutionsDocument9 pagesChapter 13 - HW With Solutionsa882906100% (1)

- Chapter 2 Review of Accounting, Financial Statements, TaxesDocument25 pagesChapter 2 Review of Accounting, Financial Statements, TaxesRohit SinghaniaNo ratings yet

- Chapter 13Document17 pagesChapter 13Aly SyNo ratings yet

- Escanear 0003Document8 pagesEscanear 0003JanetCruces0% (4)

- Academia - Week 2 - Assignment - UnderstDocument12 pagesAcademia - Week 2 - Assignment - UnderstLovey AgarwalNo ratings yet

- Revenue Recognition: Assignment Classification Table (By Topic)Document102 pagesRevenue Recognition: Assignment Classification Table (By Topic)Fajar RamadhanNo ratings yet

- Gitman pmf13 ppt05Document79 pagesGitman pmf13 ppt05moonaafreenNo ratings yet

- Cost of Capital Calculations for Preference Shares, Bonds, Common Stock & WACCDocument5 pagesCost of Capital Calculations for Preference Shares, Bonds, Common Stock & WACCshikha_asr2273No ratings yet

- Calculating Bond Prices, Yields, and ValuesDocument14 pagesCalculating Bond Prices, Yields, and ValuesMaylene Salac AlfaroNo ratings yet

- Chapter 11: Cash Flow Estimation and Risk Analysis: Page 1Document68 pagesChapter 11: Cash Flow Estimation and Risk Analysis: Page 1nouraNo ratings yet

- Gitman Ch09 01 StudentDocument42 pagesGitman Ch09 01 StudentFatima AdamNo ratings yet

- E. Patrick Assignment 4.1Document3 pagesE. Patrick Assignment 4.1Alex100% (2)

- Finance Chapter 15Document34 pagesFinance Chapter 15courtdubs100% (1)

- Valuing Bonds Chapter with 30 Multiple Choice QuestionsDocument21 pagesValuing Bonds Chapter with 30 Multiple Choice QuestionsBasa Tany100% (1)

- Cash Flow Estimation BrighamDocument77 pagesCash Flow Estimation BrighamDianne GalarosaNo ratings yet

- The Dilemma at Day 21Document4 pagesThe Dilemma at Day 21Christian AndreNo ratings yet

- Liquidity Ratios: What They Are and How to Calculate ThemDocument4 pagesLiquidity Ratios: What They Are and How to Calculate ThemLanpe100% (1)

- Finance Chapter 18Document35 pagesFinance Chapter 18courtdubs100% (1)

- Chap 5Document52 pagesChap 5jacks ocNo ratings yet

- Capital Budgeting Techniques 1Document42 pagesCapital Budgeting Techniques 1Cyrille Keith FranciscoNo ratings yet

- Valuation of Stocks & Bonds: Bfinma2: Financial Management P-2Document47 pagesValuation of Stocks & Bonds: Bfinma2: Financial Management P-2Dufuxwerr WerrNo ratings yet

- Analyze Common Stocks and Industries for Investment OpportunitiesDocument23 pagesAnalyze Common Stocks and Industries for Investment OpportunitiesHannah Jane UmbayNo ratings yet

- Chapter 9Document12 pagesChapter 9Cianne Alcantara100% (2)

- Case #84 Risk and Rates of Return - Filmore EnterprisesDocument9 pagesCase #84 Risk and Rates of Return - Filmore Enterprises3happy3100% (5)

- 032431986X 104971Document5 pages032431986X 104971Nitin JainNo ratings yet

- 2017 Acf - Revision1Document15 pages2017 Acf - Revision1Leezel100% (1)

- Financial Management: Week 10Document10 pagesFinancial Management: Week 10sanjeev parajuliNo ratings yet

- MBA711 - Answers To All Chapter 7 ProblemsDocument21 pagesMBA711 - Answers To All Chapter 7 Problemssalehin19690% (1)

- 08 Corporate BondsDocument4 pages08 Corporate Bondspriandhita asmoro75% (4)

- BH Ffm13 TB Ch02Document14 pagesBH Ffm13 TB Ch02Umer Ali KhanNo ratings yet

- Capital Budgeting: Decision Criteria: True-FalseDocument40 pagesCapital Budgeting: Decision Criteria: True-Falsedavid80dcnNo ratings yet

- CH 15 Practice MCQ - S Financial Management by BrighamDocument59 pagesCH 15 Practice MCQ - S Financial Management by BrighamShahmir AliNo ratings yet

- Can One Size Fit All?Document21 pagesCan One Size Fit All?Abhimanyu ChoudharyNo ratings yet

- Case QuestionsDocument5 pagesCase Questionsaditi_sharma_65No ratings yet

- Capital Structure: Capital Structure Refers To The Amount of Debt And/or Equity Employed by ADocument12 pagesCapital Structure: Capital Structure Refers To The Amount of Debt And/or Equity Employed by AKath LeynesNo ratings yet

- Capital StructureDocument28 pagesCapital Structureluvnica6348No ratings yet

- Capital Structure Theories ExplainedDocument10 pagesCapital Structure Theories ExplainedMd. Nazmul Kabir100% (1)

- Maximizing shareholder wealth and corporate governanceDocument3 pagesMaximizing shareholder wealth and corporate governanceyechue67% (6)

- InvestopidiaDocument18 pagesInvestopidiatinasoni11No ratings yet

- CH 13Document28 pagesCH 13lupavNo ratings yet

- Capital Stucture: Compiled To Fulfill The Duties of Marketing Management CoursesDocument8 pagesCapital Stucture: Compiled To Fulfill The Duties of Marketing Management Coursesizzah mariamiNo ratings yet

- Chapter 15Document35 pagesChapter 15Jariwala BhaveshNo ratings yet

- Capital Structure: Definition: Capital Structure Is The Mix of Financial Securities Used To Finance The FirmDocument11 pagesCapital Structure: Definition: Capital Structure Is The Mix of Financial Securities Used To Finance The FirmArun NairNo ratings yet

- University of Central Punjab: F 2020 Course Title: Financial Strategy Course Code: IVA5833Document8 pagesUniversity of Central Punjab: F 2020 Course Title: Financial Strategy Course Code: IVA5833Ayesha HamidNo ratings yet

- Capital Structure and Firm PerformanceDocument15 pagesCapital Structure and Firm PerformanceAcademicNo ratings yet

- Chapter 2 - CompleteDocument29 pagesChapter 2 - Completemohsin razaNo ratings yet

- If I Would Like To Protect My Downside, How Would I Structure The Investment?Document7 pagesIf I Would Like To Protect My Downside, How Would I Structure The Investment?helloNo ratings yet

- Financial Mathematics Unit III: Capital Structure and LeverageDocument4 pagesFinancial Mathematics Unit III: Capital Structure and Leverageharish chandraNo ratings yet

- 1) Income Statement: Nature, Forms and Uses of Income StatementDocument6 pages1) Income Statement: Nature, Forms and Uses of Income StatementPaulineBiroselNo ratings yet

- BDO Products and ServicesDocument3 pagesBDO Products and ServicesPaulineBiroselNo ratings yet

- Project Charter Group 10Document1 pageProject Charter Group 10PaulineBiroselNo ratings yet

- Philippine Environmental Laws ListDocument5 pagesPhilippine Environmental Laws ListPaulineBiroselNo ratings yet

- Theory of Accounts-Case StudyDocument2 pagesTheory of Accounts-Case StudyPaulineBiroselNo ratings yet

- 14 LasherIM Ch14-1Document25 pages14 LasherIM Ch14-1PaulineBirosel100% (1)

- Reported By: Arago - Birosel - Clemente Garcia - Geronimo - MajadasDocument11 pagesReported By: Arago - Birosel - Clemente Garcia - Geronimo - MajadasPaulineBiroselNo ratings yet

- Sample Problems With Suggested AnswersDocument9 pagesSample Problems With Suggested AnswersRenato GivenNo ratings yet

- Report in Accrev (Ppe)Document18 pagesReport in Accrev (Ppe)PaulineBiroselNo ratings yet

- 08 LasherIM Ch08 1Document20 pages08 LasherIM Ch08 1PaulineBiroselNo ratings yet

- BS Horizontal Analysis (PALTONGAN)Document3 pagesBS Horizontal Analysis (PALTONGAN)PaulineBiroselNo ratings yet

- Globe Telecom Working CapitalDocument6 pagesGlobe Telecom Working CapitalPaulineBiroselNo ratings yet

- Risk and ReturnDocument75 pagesRisk and ReturnPaulineBiroselNo ratings yet

- Computer Scope StatementDocument2 pagesComputer Scope StatementPaulineBiroselNo ratings yet

- Presentation3 FINMAN Working CapitalDocument5 pagesPresentation3 FINMAN Working CapitalPaulineBiroselNo ratings yet

- Financial Disclosures Checklist: General InstructionsDocument35 pagesFinancial Disclosures Checklist: General InstructionsPaulineBiroselNo ratings yet

- Theory of Accounts (Income Statement)Document49 pagesTheory of Accounts (Income Statement)PaulineBiroselNo ratings yet

- Case Study of McdoDocument16 pagesCase Study of McdoPaulineBirosel60% (5)

- Theory of Accounts (Income Statment)Document6 pagesTheory of Accounts (Income Statment)PaulineBirosel0% (1)

- Starbucks Social Relations and Environment Responsibilities. Thesis Market ShareDocument25 pagesStarbucks Social Relations and Environment Responsibilities. Thesis Market SharePaulineBiroselNo ratings yet

- Obligations and Contract (Law1)Document7 pagesObligations and Contract (Law1)PaulineBiroselNo ratings yet

- Tax QuestionsDocument10 pagesTax QuestionsUdit VarshneyNo ratings yet

- Cambridge IGCSE ™: Accounting 0452/21 October/November 2022Document18 pagesCambridge IGCSE ™: Accounting 0452/21 October/November 2022Muhammad AhmadNo ratings yet

- PayslipDocument2 pagesPayslipWelson TeNo ratings yet

- Public Borrowing 4Document14 pagesPublic Borrowing 4Corpuz Tyrone0% (1)

- VAT RefundDocument45 pagesVAT RefundPatrick Tan100% (1)

- Problem Set 2: FIN 401: Financial Management Syed Waqar AhmedDocument3 pagesProblem Set 2: FIN 401: Financial Management Syed Waqar AhmedJiteshNo ratings yet

- Module 7 AssignmentDocument3 pagesModule 7 AssignmentRosario CabarrubiasNo ratings yet

- Why BPCDocument42 pagesWhy BPCJay BocagoNo ratings yet

- Determine if Partnership ExistsDocument7 pagesDetermine if Partnership ExistsNova MarasiganNo ratings yet

- Chapter 16Document15 pagesChapter 16Jesse AndersonNo ratings yet

- Financial Due Diligence ChecklistDocument1 pageFinancial Due Diligence ChecklistgauravNo ratings yet

- Project Report of Financial Analysis of Blue Star and HitachiDocument16 pagesProject Report of Financial Analysis of Blue Star and HitachiAman VermaNo ratings yet

- Wage and Tax StatementDocument4 pagesWage and Tax StatementRich1781No ratings yet

- Taxation of Income in NepalDocument24 pagesTaxation of Income in NepalSophiya PrabinNo ratings yet

- 2-Webinar QuestionsDocument11 pages2-Webinar QuestionshusseinNo ratings yet

- PCT01 - Introduction To TrustsDocument23 pagesPCT01 - Introduction To Trusts2Plus100% (2)

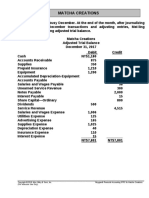

- MC4 Matcha Creations: (For Instructor Use Only)Document2 pagesMC4 Matcha Creations: (For Instructor Use Only)Reza eka PutraNo ratings yet

- Factors to Analyze a Company for Long-Term InvestmentDocument51 pagesFactors to Analyze a Company for Long-Term InvestmentmallinlrNo ratings yet

- Malak Anf Fatma Part ITFDocument9 pagesMalak Anf Fatma Part ITFMohga .FNo ratings yet

- Answers Homework # 21 - Financial Reporting III-CashflowDocument6 pagesAnswers Homework # 21 - Financial Reporting III-CashflowRaman ANo ratings yet

- GOVBUSMAN MODULE 9 (12) - Chapter 15Document4 pagesGOVBUSMAN MODULE 9 (12) - Chapter 15Rohanne Garcia AbrigoNo ratings yet

- Weak Student Material - MacroDocument14 pagesWeak Student Material - MacroP Janaki RamanNo ratings yet

- CFOs Guide To Measuring The Finance FunctionDocument1 pageCFOs Guide To Measuring The Finance FunctionHitesh UppalNo ratings yet

- Group Accounts: IFRS 10 Consolidated Financial StatementsDocument9 pagesGroup Accounts: IFRS 10 Consolidated Financial StatementsHunairArshadNo ratings yet

- Time Value of Money OutlineDocument14 pagesTime Value of Money OutlineEmman LubisNo ratings yet

- Acc 3 - RRNDDocument27 pagesAcc 3 - RRNDHistory and EventNo ratings yet

- E. Break-Even PointDocument2 pagesE. Break-Even PointMarfe BlancoNo ratings yet

- Npo Class 12 Ncert AnswersDocument61 pagesNpo Class 12 Ncert Answersrxcha.josephNo ratings yet

- Practice SetDocument5 pagesPractice SetgnlynNo ratings yet

- Acct 2301 FinaDocument42 pagesAcct 2301 FinaFabian NonesNo ratings yet