You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (894)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- Mythomann Invoice 48940470 PDFDocument1 pageMythomann Invoice 48940470 PDFSusana GarciaNo ratings yet

- Epicor ERP Order Management Course 10.0.700.2Document67 pagesEpicor ERP Order Management Course 10.0.700.2nerz8830100% (1)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Body Shop Case StudyDocument3 pagesThe Body Shop Case StudysahilsureshNo ratings yet

- Romanian Cosmetics Industry PDFDocument0 pagesRomanian Cosmetics Industry PDFMd Raisul AzamNo ratings yet

- Bond Report 3-11-18Document2 pagesBond Report 3-11-18api-278033882No ratings yet

- Bond Report 3-4-18Document2 pagesBond Report 3-4-18api-278033882No ratings yet

- Bond Report 4th Week of SeptemberDocument2 pagesBond Report 4th Week of Septemberapi-278033882No ratings yet

- Macroeconomic Overview April Week 4Document2 pagesMacroeconomic Overview April Week 4api-278033882No ratings yet

- Bond Report 11-05-20127Document2 pagesBond Report 11-05-20127api-278033882No ratings yet

- Macro4 18Document2 pagesMacro4 18api-278033882No ratings yet

- Bond Report 10-29-17Document2 pagesBond Report 10-29-17api-278033882No ratings yet

- Bond Report 12-4-17Document2 pagesBond Report 12-4-17api-278033882No ratings yet

- Bond Report 11-12-2017Document2 pagesBond Report 11-12-2017api-278033882No ratings yet

- Bond Report 10-08017Document2 pagesBond Report 10-08017api-278033882No ratings yet

- Analyst Ranking Spring 2017 FinalDocument1 pageAnalyst Ranking Spring 2017 Finalapi-278033882No ratings yet

- Analyst Ranking Final Fall 2016Document1 pageAnalyst Ranking Final Fall 2016api-278033882No ratings yet

- Bond Report 3rd Week of AprilDocument2 pagesBond Report 3rd Week of Aprilapi-278033882No ratings yet

- Bond Report 4th Week of AprilDocument2 pagesBond Report 4th Week of Aprilapi-278033882No ratings yet

- Macro March WK 1Document2 pagesMacro March WK 1api-278033882No ratings yet

- Macroeconomic Overview March WK 4Document2 pagesMacroeconomic Overview March WK 4api-278033882No ratings yet

- Macro-Bond Feb WK 4-17Document3 pagesMacro-Bond Feb WK 4-17api-278033882No ratings yet

- Bond Report April Week 1Document2 pagesBond Report April Week 1api-278033882No ratings yet

- Bond Report 4th Week of MarchDocument2 pagesBond Report 4th Week of Marchapi-278033882No ratings yet

- Macro March WK 3Document2 pagesMacro March WK 3api-278033882No ratings yet

- Thesis Summary Template FinalDocument4 pagesThesis Summary Template Finalapi-278033882No ratings yet

- Bond Report 3nd Week of MarchDocument2 pagesBond Report 3nd Week of Marchapi-278033882No ratings yet

- Bond Report 3Document2 pagesBond Report 3api-278033882No ratings yet

- Bond Report 2nd Week of DecemberDocument2 pagesBond Report 2nd Week of Decemberapi-278033882No ratings yet

- Bond Report 3rd Week of FebruaryDocument2 pagesBond Report 3rd Week of Februaryapi-278033882No ratings yet

- Thesis Summary TemplateDocument2 pagesThesis Summary Templateapi-278033882No ratings yet

- Market Report FinalDocument2 pagesMarket Report Finalapi-278033882No ratings yet

- Bond Report 1st Week of MarchDocument2 pagesBond Report 1st Week of Marchapi-278033882No ratings yet

- Macro11 6Document2 pagesMacro11 6api-278033882No ratings yet

- Bond Report Nov 27Document2 pagesBond Report Nov 27api-278033882No ratings yet

- Gasbill 7849961000 202307 20230726135704Document1 pageGasbill 7849961000 202307 20230726135704AaFi SoomroNo ratings yet

- Using Digital Marketing To Develop A Modern Marketing Strategy For A StartupDocument76 pagesUsing Digital Marketing To Develop A Modern Marketing Strategy For A StartupDalji SaimNo ratings yet

- Numericals - SS DD-Set IIDocument20 pagesNumericals - SS DD-Set IIudit singhNo ratings yet

- Project Title: Octorich Dairy Products Executive SummaryDocument46 pagesProject Title: Octorich Dairy Products Executive SummaryArun SavukarNo ratings yet

- Market Report BriteDocument46 pagesMarket Report Britesyedtahashah0% (2)

- Walmart Case StudyDocument9 pagesWalmart Case StudySama KurimNo ratings yet

- Resume 1Document2 pagesResume 1api-298164137No ratings yet

- Ag Mktg-AEBoardExamReviewDocument115 pagesAg Mktg-AEBoardExamReviewDarenNo ratings yet

- IKEA's Business and Operating Models: Product Design ProcessDocument5 pagesIKEA's Business and Operating Models: Product Design ProcessTioNo ratings yet

- Producer's Equilibrium ExplainedDocument14 pagesProducer's Equilibrium Explainedrohitbatra100% (1)

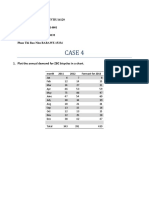

- Case 4: Luyen Ngoc Do Quyen BTFTIU14129 Ngo Khanh Duy BTARIU14601 Pham Gia Huy BTFTIU14132 Phan Thi Bao Nhu BABAWE 15334Document4 pagesCase 4: Luyen Ngoc Do Quyen BTFTIU14129 Ngo Khanh Duy BTARIU14601 Pham Gia Huy BTFTIU14132 Phan Thi Bao Nhu BABAWE 15334HuynhGiangNo ratings yet

- MS MCQS - WatermarkDocument55 pagesMS MCQS - WatermarkHari SoloNo ratings yet

- Sales professional with expertise in cold calling, sales force effectiveness, and customer focusDocument2 pagesSales professional with expertise in cold calling, sales force effectiveness, and customer focusindercappyNo ratings yet

- Smith, Bell & Co. vs. Vicente Sotelo MattiDocument6 pagesSmith, Bell & Co. vs. Vicente Sotelo Mattides_0212No ratings yet

- The Extended Marketing MixDocument6 pagesThe Extended Marketing MixMAHENDRA SHIVAJI DHENAK50% (2)

- Trade Sales PromotionDocument29 pagesTrade Sales PromotionashishNo ratings yet

- ITC's Strategy to Diversify Beyond TobaccoDocument27 pagesITC's Strategy to Diversify Beyond Tobaccorohan48No ratings yet

- MN - 2015 07 14Document36 pagesMN - 2015 07 14mooraboolNo ratings yet

- Writing A Business Plan 20130314Document35 pagesWriting A Business Plan 20130314Mohd FadhilullahNo ratings yet

- Oligopoly Is The Most Prevalent Form of Market Organization in The Manufacturingsector of Most NationsDocument9 pagesOligopoly Is The Most Prevalent Form of Market Organization in The Manufacturingsector of Most NationsBhagyashree MohiteNo ratings yet

- Tutorial Miroeconomics - StuDocument14 pagesTutorial Miroeconomics - StuD Dávíd FungNo ratings yet

- SMDocument7 pagesSMShashi SharmaNo ratings yet

- Resale Price Lor Lew LianDocument2 pagesResale Price Lor Lew LianAlex Ng W HNo ratings yet

- Concept of Anti-Profiteering Measures Under GST RegimeDocument3 pagesConcept of Anti-Profiteering Measures Under GST RegimemuskanNo ratings yet

- AIS Midterm PDFDocument7 pagesAIS Midterm PDFGlennizze GalvezNo ratings yet