You might also like

- Value Added Tax AUDITDocument40 pagesValue Added Tax AUDITBhagwat Thakker60% (5)

- VAT Audit ProceduresDocument3 pagesVAT Audit ProceduresAnthony Martinez OrasaNo ratings yet

- Audit Trade Receivables Sales BalancesDocument2 pagesAudit Trade Receivables Sales BalancesDiane VillarmaNo ratings yet

- Audit & Tax Lec 1 & 2Document9 pagesAudit & Tax Lec 1 & 2Shoumik MahmudNo ratings yet

- Accounts Payable Sox TestingDocument2 pagesAccounts Payable Sox TestingStephen JonesNo ratings yet

- Accounts Payable Audit ProgramDocument15 pagesAccounts Payable Audit ProgramdannielNo ratings yet

- Ftbend Payroll Audit ProgghframDocument6 pagesFtbend Payroll Audit ProgghframJenofDulwnNo ratings yet

- Audit of PayrollDocument5 pagesAudit of Payrollnano_revor93No ratings yet

- Revenue Cycle AuditDocument13 pagesRevenue Cycle AuditSulav PoudelNo ratings yet

- Account PayableDocument11 pagesAccount PayableShintia Ayu PermataNo ratings yet

- E7 - TreasuryRCM TemplateDocument30 pagesE7 - TreasuryRCM Templatenazriya nasarNo ratings yet

- Accounting Level 3 Assessment - Cluster 8Document8 pagesAccounting Level 3 Assessment - Cluster 8Stephen PommellsNo ratings yet

- Audit AP CompletenessDocument7 pagesAudit AP CompletenessMacmilan Trevor Jamu0% (1)

- Insurance Audit ProgrammeDocument5 pagesInsurance Audit ProgrammeCheick Abdoul100% (1)

- Hartford Payroll Audit ReportDocument10 pagesHartford Payroll Audit ReportkevinhfdNo ratings yet

- The Auditing ProfessionDocument10 pagesThe Auditing Professionmqondisi nkabindeNo ratings yet

- Bank Audit ProgramDocument6 pagesBank Audit Programramu9999100% (1)

- Chapter 1 Multiple-Choice Questions AccountingDocument29 pagesChapter 1 Multiple-Choice Questions Accountingthangdongquay152100% (2)

- Ifrs at A Glance IFRS 15 Revenue From Contracts: With CustomersDocument7 pagesIfrs at A Glance IFRS 15 Revenue From Contracts: With CustomersManoj GNo ratings yet

- Audit Program Bank and CashDocument4 pagesAudit Program Bank and CashFakhruddin Young Executives0% (1)

- Agreed Upon Procedures vs. Consulting EngagementsDocument49 pagesAgreed Upon Procedures vs. Consulting EngagementsCharles B. Hall100% (1)

- A Cpas & Controllers Checklist For Closing Your Books at Year-End Part One: Closing The Books at Year-EndDocument3 pagesA Cpas & Controllers Checklist For Closing Your Books at Year-End Part One: Closing The Books at Year-EndDurbanskiNo ratings yet

- Presentation On Pre-Audit of PaymentDocument55 pagesPresentation On Pre-Audit of Paymentsanjay_sbi100% (1)

- Fixed Asset Acquisition FormDocument1 pageFixed Asset Acquisition FormJack L. JohnsonNo ratings yet

- Accounts PayableDocument44 pagesAccounts Payablethat_glossmk100% (2)

- IFC PPT AhmedabadDocument57 pagesIFC PPT AhmedabadPrashant JainNo ratings yet

- Audit Procedure in BangladeshDocument14 pagesAudit Procedure in BangladeshSahed UzzamanNo ratings yet

- Payroll AuditDocument12 pagesPayroll AuditmazorodzesNo ratings yet

- Control Matrix - Premiums (PC)Document9 pagesControl Matrix - Premiums (PC)Jose SasNo ratings yet

- External Audit AssignmentDocument8 pagesExternal Audit Assignmentishah1No ratings yet

- Auditing The Expenditure Cycle: Expenditure Cycle Audit Objectives, Controls, and Test of ControlsDocument9 pagesAuditing The Expenditure Cycle: Expenditure Cycle Audit Objectives, Controls, and Test of ControlsYoite MiharuNo ratings yet

- Audit of Hospital - Mcom Part II ProjectDocument28 pagesAudit of Hospital - Mcom Part II ProjectKunal KapoorNo ratings yet

- Auditors' DutiesDocument15 pagesAuditors' DutiesSyad Shahidah100% (1)

- 02.1 Taxes RCMDocument6 pages02.1 Taxes RCMacasumitchhabraNo ratings yet

- Topic 11 Audit of Payroll & Personnel CycleDocument14 pagesTopic 11 Audit of Payroll & Personnel Cyclebutirkuaci100% (1)

- BDO Internal Audit Manual SummaryDocument7 pagesBDO Internal Audit Manual SummaryAdolph Christian GonzalesNo ratings yet

- Audit Programme 1Document20 pagesAudit Programme 1Neelam Goel0% (1)

- Payroll CycleDocument8 pagesPayroll CyclePauline Keith Paz ManuelNo ratings yet

- Key Roles & Responsibilities of Accounts Receivable - Finance in Erp and CRMDocument35 pagesKey Roles & Responsibilities of Accounts Receivable - Finance in Erp and CRMABT SuppNo ratings yet

- Fixed Asset VeificationDocument12 pagesFixed Asset Veificationnarasi64No ratings yet

- Statutory Audit ChecklistDocument6 pagesStatutory Audit ChecklistCA SwaroopNo ratings yet

- Working Papers - Top Tips PDFDocument3 pagesWorking Papers - Top Tips PDFYus Ceballos100% (1)

- Airline Industry Guidance Ifrs 15Document37 pagesAirline Industry Guidance Ifrs 15Raghavendra AcharyaNo ratings yet

- Accounts Receivable, Credit and Collections Audit Report - Sample 2Document29 pagesAccounts Receivable, Credit and Collections Audit Report - Sample 2Audit Department100% (2)

- AIS Chapter 4 - PAYROLL & FIXED ASSETSDocument54 pagesAIS Chapter 4 - PAYROLL & FIXED ASSETSnatalie clyde mates100% (1)

- TESTING PAYROLL CONTROLSDocument4 pagesTESTING PAYROLL CONTROLSCristopherson PerezNo ratings yet

- PURCHASE-TO-PAYMENT PROCESS ASSESSMENT REVIEWDocument36 pagesPURCHASE-TO-PAYMENT PROCESS ASSESSMENT REVIEWviswaja100% (1)

- Internal Controls and ERPDocument5 pagesInternal Controls and ERPapi-3748088No ratings yet

- A0 Background Information and Document Request ChecklistDocument11 pagesA0 Background Information and Document Request Checklistabdul syukurNo ratings yet

- Protect Your BusinessDocument19 pagesProtect Your BusinessEiron AlmeronNo ratings yet

- Finance AccountsDocument13 pagesFinance AccountsVishal ChaudharyNo ratings yet

- FLSA Audit ProgramDocument4 pagesFLSA Audit ProgramDascalu OvidiuNo ratings yet

- NIA R12 Finance FlowchartDocument6 pagesNIA R12 Finance FlowchartAngelita BarcelonaNo ratings yet

- AU Locks Auditing Services: Audit Program Batangas Bestfeeds Multipurpose CooperativeDocument5 pagesAU Locks Auditing Services: Audit Program Batangas Bestfeeds Multipurpose CooperativeMirai KuriyamaNo ratings yet

- Walk-Through Accounts Payable/Expenses FormDocument4 pagesWalk-Through Accounts Payable/Expenses FormCharles B. HallNo ratings yet

- Controlling Payroll Cost - Critical Disciplines for Club ProfitabilityFrom EverandControlling Payroll Cost - Critical Disciplines for Club ProfitabilityNo ratings yet

- CH 18 and 19 HWDocument14 pagesCH 18 and 19 HWmonika1yustiawisdanaNo ratings yet

- AC414 - Audit and Investigations II - Audit of Payables, Capital and Reserves IIDocument18 pagesAC414 - Audit and Investigations II - Audit of Payables, Capital and Reserves IITsitsi AbigailNo ratings yet

- FA II - Chapter 1, Current LiabilitiesDocument94 pagesFA II - Chapter 1, Current LiabilitiesBeamlak WegayehuNo ratings yet

- Involuntary Loss of Employment Brochure ILOEDocument20 pagesInvoluntary Loss of Employment Brochure ILOESaileshNo ratings yet

- Di New Pattern BFPDocument245 pagesDi New Pattern BFPDeepak LohiaNo ratings yet

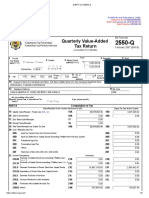

- Value Added TaxDocument46 pagesValue Added TaxBoss NikNo ratings yet

- 04-Duty Free Phils. v. Bureau of Internal Revenue. GR No 197228Document6 pages04-Duty Free Phils. v. Bureau of Internal Revenue. GR No 197228ryanmeinNo ratings yet

- KASHATODocument39 pagesKASHATOUser 101No ratings yet

- Sap Fi Ques N AnswersDocument67 pagesSap Fi Ques N AnswersRANAGADONGA100% (1)

- Ba JFG Bals59 GDDocument5 pagesBa JFG Bals59 GDgenericipguyNo ratings yet

- Budget Highlights FY 2080 811Document13 pagesBudget Highlights FY 2080 811Sushant AdhikariNo ratings yet

- Transfer Duty BotswanaDocument8 pagesTransfer Duty BotswanaFrancis0% (1)

- Mining Sector TanzaniaDocument141 pagesMining Sector TanzaniaRegnald MponziNo ratings yet

- Composition Scheme Under GST ExplainedDocument3 pagesComposition Scheme Under GST ExplainedrgurvareddyNo ratings yet

- User'S Manual: Fiscal PrinterDocument23 pagesUser'S Manual: Fiscal PrinterFric TechnologiesNo ratings yet

- Tax Code Determination in CCSDocument2 pagesTax Code Determination in CCSSOUMEN DASNo ratings yet

- Tender Specification of Surge ArresterDocument68 pagesTender Specification of Surge ArresterGuru MishraNo ratings yet

- Current Affairs Q&A PDF - January 2018 by AffairsCloudDocument199 pagesCurrent Affairs Q&A PDF - January 2018 by AffairsCloudJEE REV RAJAULINo ratings yet

- Tax Invoice for HeadphonesDocument1 pageTax Invoice for HeadphonesPV VimalNo ratings yet

- Additonal Disclosure RR 15 2010Document5 pagesAdditonal Disclosure RR 15 2010Emil A. MolinaNo ratings yet

- Polymatic Plastics & Packaging Market Deepening Versus Geography ExpansionDocument14 pagesPolymatic Plastics & Packaging Market Deepening Versus Geography ExpansionAkash BhambareNo ratings yet

- Abdul Basit: Work ExperienceDocument1 pageAbdul Basit: Work ExperienceMuhammad ZakiNo ratings yet

- Utility Bill AnywhereDocument1 pageUtility Bill AnywhereAjit RawalNo ratings yet

- Bsbfim601 - Task 2Document7 pagesBsbfim601 - Task 2Ghie Morales50% (4)

- Contoh Latihan Soal Studi Kasus MYOB AccountingDocument8 pagesContoh Latihan Soal Studi Kasus MYOB AccountingLight YagamiNo ratings yet

- MSC Computer Science ProspectusDocument12 pagesMSC Computer Science ProspectusEdmond MalataNo ratings yet

- EFPS Home - EFiling and Payment SystemDocument2 pagesEFPS Home - EFiling and Payment Systemmelanie venturaNo ratings yet

- Percentage Taxes NotesDocument4 pagesPercentage Taxes Notesrajahmati_28No ratings yet

- Pagcor Vs Bir 2011Document3 pagesPagcor Vs Bir 2011CARLOSPAULADRIANNE MARIANONo ratings yet

- Silicon Philippines V CirDocument2 pagesSilicon Philippines V CirKia BiNo ratings yet

- Sap Fi 4.6 Exercises Financial Accounting - Chapter 29 Appendix 1. Sales & Use TaxDocument3 pagesSap Fi 4.6 Exercises Financial Accounting - Chapter 29 Appendix 1. Sales & Use TaxVaibhavNo ratings yet

- Peter Taylor - Book-Keeping & Accounting For Small Business, 7th EditionDocument190 pagesPeter Taylor - Book-Keeping & Accounting For Small Business, 7th EditionMarcos Besteiro López100% (3)