You might also like

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Ratio Analysis Pre by Kuldeep GhanghasDocument11 pagesRatio Analysis Pre by Kuldeep Ghanghaskuldeep ghanghasNo ratings yet

- Inflation+& +unemployment by KULDEEP GhanghasDocument17 pagesInflation+& +unemployment by KULDEEP Ghanghaskuldeep ghanghasNo ratings yet

- EoM8+Oligopoly1 ByKuldeep GhanghasDocument14 pagesEoM8+Oligopoly1 ByKuldeep Ghanghaskuldeep ghanghasNo ratings yet

- Budgeting by Kuldeep GhanghasDocument20 pagesBudgeting by Kuldeep Ghanghaskuldeep ghanghasNo ratings yet

- EoM7+Monopoly by Kuldeep GhanghasDocument11 pagesEoM7+Monopoly by Kuldeep Ghanghaskuldeep ghanghasNo ratings yet

- EoM9+Monopolistic+Competition BY Kuldeep GHANGHASDocument12 pagesEoM9+Monopolistic+Competition BY Kuldeep GHANGHASkuldeep ghanghasNo ratings yet

- EoM6 Perfectly Competitive Markets by Kuldeep GhanghasDocument10 pagesEoM6 Perfectly Competitive Markets by Kuldeep Ghanghaskuldeep ghanghasNo ratings yet

- EoM5 Theory of The Firm by Kuldeep GhanghasDocument19 pagesEoM5 Theory of The Firm by Kuldeep Ghanghaskuldeep ghanghasNo ratings yet

- EoM3 Elasticity of Demand by Kuldeep GhanghasDocument18 pagesEoM3 Elasticity of Demand by Kuldeep Ghanghaskuldeep ghanghasNo ratings yet

- EoM2 DemandSupply by KuldeepDocument21 pagesEoM2 DemandSupply by Kuldeepkuldeep ghanghasNo ratings yet

- EoM4 Theory of The Consumer by Kuldeep GhanghasDocument18 pagesEoM4 Theory of The Consumer by Kuldeep Ghanghaskuldeep ghanghasNo ratings yet

- EoM1 Intro by Kuldeep GhanghasDocument17 pagesEoM1 Intro by Kuldeep Ghanghaskuldeep ghanghasNo ratings yet

- Eco National+Income+Accounting by Kuldeep GhanghasDocument17 pagesEco National+Income+Accounting by Kuldeep Ghanghaskuldeep ghanghasNo ratings yet

- Bio Metrics by KuldeepDocument6 pagesBio Metrics by Kuldeepkuldeep ghanghasNo ratings yet

- Pricing Strategies & ProgramsDocument33 pagesPricing Strategies & Programskuldeep ghanghasNo ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Advanced Financial Management PDFDocument6 pagesAdvanced Financial Management PDFSmag SmagNo ratings yet

- Chapter 02 - Basic Financial StatementsDocument111 pagesChapter 02 - Basic Financial Statementsyujia ZhaiNo ratings yet

- Nse Research Analysis 2020Document53 pagesNse Research Analysis 2020Anuj ThapaNo ratings yet

- Overview IASDocument12 pagesOverview IASButt ArhamNo ratings yet

- Dolat Capital Market - Vinati Organics - Q2FY20 Result Update - 1Document6 pagesDolat Capital Market - Vinati Organics - Q2FY20 Result Update - 1Bhaveek OstwalNo ratings yet

- Chapter 9 PowerPointDocument101 pagesChapter 9 PowerPointcheuleee100% (2)

- IA1 - 1st Mock Quiz (With Suggested Answers)Document6 pagesIA1 - 1st Mock Quiz (With Suggested Answers)Rogienel ReyesNo ratings yet

- Ycoa Accdet Docu XXDocument2,071 pagesYcoa Accdet Docu XXMamata DasNo ratings yet

- XJF1 1Document51 pagesXJF1 1Ching YuewNo ratings yet

- Exercises I - Journalizing and PostingDocument7 pagesExercises I - Journalizing and PostingJowjie TV50% (2)

- 21.12.07 Jawaban PT SejahteraDocument76 pages21.12.07 Jawaban PT Sejahtera202010415109 ADITYA FIRNANDO100% (1)

- Dividend Policy & Traditional PolicyDocument34 pagesDividend Policy & Traditional PolicyVaidyanathan RavichandranNo ratings yet

- Lucknow Seission Ending Project 2021-22 Name:Aditi Shukla Class:Xith-D Roll No:04 Submitted To: MR - Kush SrivastavaDocument24 pagesLucknow Seission Ending Project 2021-22 Name:Aditi Shukla Class:Xith-D Roll No:04 Submitted To: MR - Kush SrivastavaAdisha's100% (1)

- Cost Accounting Labor Costs AssignmentDocument3 pagesCost Accounting Labor Costs AssignmentGabriel EvannNo ratings yet

- Sample EquityDocument13 pagesSample EquityMinhajNo ratings yet

- Abbl3144 Tutorial 3 AnswerDocument9 pagesAbbl3144 Tutorial 3 AnswerSooXueJiaNo ratings yet

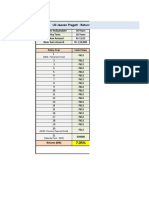

- LIC Jeevan Pragati - Returns Calculation - Example: (2010: Policy Start Year)Document2 pagesLIC Jeevan Pragati - Returns Calculation - Example: (2010: Policy Start Year)Ravi bNo ratings yet

- Capital Structure and Factors Affecting Capital Structure: Bhadrappa Haralayya, Jeelan Basha V, Nitesh S VibhuteDocument32 pagesCapital Structure and Factors Affecting Capital Structure: Bhadrappa Haralayya, Jeelan Basha V, Nitesh S VibhuteDr Bhadrappa HaralayyaNo ratings yet

- FABM2 1st Half of 1st Quarter Reviewer ACRSDocument2 pagesFABM2 1st Half of 1st Quarter Reviewer ACRSAfeiyha Czarina SantiagoNo ratings yet

- Occupied 500: Area FT.) Light PointsDocument10 pagesOccupied 500: Area FT.) Light PointsAbhijit HoroNo ratings yet

- Far160 Pyq July2023Document8 pagesFar160 Pyq July2023nazzyusoffNo ratings yet

- Part 2A Form AdvDocument16 pagesPart 2A Form AdvDavid KeresztesNo ratings yet

- FinmartDocument3 pagesFinmartAngelica Faye DuroNo ratings yet

- Module 4 - Going Concern Asset Based Valuation - Comparable Company AnalysisDocument3 pagesModule 4 - Going Concern Asset Based Valuation - Comparable Company AnalysisLiaNo ratings yet

- Dividend PolicyDocument51 pagesDividend PolicyMmonower HosenNo ratings yet

- HMPSA TALE (Tutoring and Learning Ease) : Accounting For Merchandising OperationsDocument53 pagesHMPSA TALE (Tutoring and Learning Ease) : Accounting For Merchandising OperationsKevin Chandra100% (1)

- ANSWERDocument9 pagesANSWERLeesaa88No ratings yet

- Itc Clsa Oct2020Document100 pagesItc Clsa Oct2020ksatishbabuNo ratings yet

- Ceo or Coo or CfoDocument2 pagesCeo or Coo or Cfoapi-121403662No ratings yet

- Problem 1 San Pedro: AssetsDocument9 pagesProblem 1 San Pedro: AssetsGastelyn JacintoNo ratings yet