You might also like

- Legal Aid Service AuthorityDocument28 pagesLegal Aid Service AuthoritysajNo ratings yet

- CPC AssignmentDocument10 pagesCPC AssignmentDharu LilawatNo ratings yet

- Income Under The Head Salary2Document142 pagesIncome Under The Head Salary2OnlineNo ratings yet

- Doctrine of RestitutionDocument3 pagesDoctrine of RestitutionBhumanjay TomarNo ratings yet

- Perquisites and Allowances Under The Head SalariesDocument15 pagesPerquisites and Allowances Under The Head SalariesAYUSHI TYAGINo ratings yet

- When Does A Court Take CognizanceDocument2 pagesWhen Does A Court Take CognizancerohanNo ratings yet

- Advocates Act, 1961 ShortDocument4 pagesAdvocates Act, 1961 ShortArun .cNo ratings yet

- Environment Project Sem6Document15 pagesEnvironment Project Sem6Amit RawlaniNo ratings yet

- Income Tax AuthorityDocument15 pagesIncome Tax AuthorityMahin HasanNo ratings yet

- Critical Analysis Judicial Review and Abuse of PowerDocument21 pagesCritical Analysis Judicial Review and Abuse of PowerSri Nur HariNo ratings yet

- Adjudication and Appeal Under FemaDocument17 pagesAdjudication and Appeal Under FemaRohit GargNo ratings yet

- Industrial Disputes ActDocument5 pagesIndustrial Disputes ActMegha LalNo ratings yet

- Appointment of ReceiverDocument9 pagesAppointment of ReceiverrahulNo ratings yet

- Constitution FDDocument47 pagesConstitution FDABhishek KUmar0% (1)

- Types of EvidencesDocument16 pagesTypes of EvidencesGaurav PandeyNo ratings yet

- It Project SidhiDocument24 pagesIt Project SidhiSHREYABANSAL18No ratings yet

- Chapter XXII Indian Penal CodeDocument15 pagesChapter XXII Indian Penal CodeRamakrishnan VishwanathanNo ratings yet

- Grounds For Challenge To Arbitral AwardDocument6 pagesGrounds For Challenge To Arbitral AwardNikhil GulianiNo ratings yet

- Aligarh Muslim University Malappuram Centre, Kerala: Intellectual Property Rights ProjectDocument15 pagesAligarh Muslim University Malappuram Centre, Kerala: Intellectual Property Rights ProjectSadhvi SinghNo ratings yet

- Right To Information Act, 2005Document9 pagesRight To Information Act, 2005Sourav paulNo ratings yet

- Assignment Taxation LawDocument4 pagesAssignment Taxation LawAbhishek PathakNo ratings yet

- Section-10: Income Exempt From TaxDocument21 pagesSection-10: Income Exempt From TaxRakesh SharmaNo ratings yet

- Doctrine of ProportionalityDocument8 pagesDoctrine of Proportionalityanshita maniNo ratings yet

- Jurisprudence II ProjectDocument17 pagesJurisprudence II ProjectVishwaja RaoNo ratings yet

- Appeal Reference and RevisionDocument8 pagesAppeal Reference and RevisionVíshál RánáNo ratings yet

- RestrictionDocument12 pagesRestrictionadiNo ratings yet

- Inter-State Trade, Commerce, and Intercourse: Arvind P DatarDocument13 pagesInter-State Trade, Commerce, and Intercourse: Arvind P DatarAadhitya NarayananNo ratings yet

- Public International Law Assignment: Topic: Relationship Between International Law and Municipal LawDocument10 pagesPublic International Law Assignment: Topic: Relationship Between International Law and Municipal LawTaiyabaNo ratings yet

- A Case Study On Vellore Citizens Welfare Forum Vs Union of India With Special Reference To Polluters Pay Principle J.Sabitha J.Tamil SelviDocument11 pagesA Case Study On Vellore Citizens Welfare Forum Vs Union of India With Special Reference To Polluters Pay Principle J.Sabitha J.Tamil SelviJ Sab IthaNo ratings yet

- The Culture of Adr in IndiaDocument7 pagesThe Culture of Adr in IndiashariqueNo ratings yet

- Company LawDocument29 pagesCompany LawAnonymous lzwNwkpNo ratings yet

- Environmental Law Project-3Document19 pagesEnvironmental Law Project-3lakshayNo ratings yet

- Utilitarian and Kantian Theory of PunishmentDocument15 pagesUtilitarian and Kantian Theory of Punishmentsatyam krNo ratings yet

- Receiver AssignmentDocument5 pagesReceiver AssignmentAdv Riad Hossain RanaNo ratings yet

- CPCDocument6 pagesCPCAnonymous C2ZcHJbKNo ratings yet

- Case Commentary L Chandra Kumar Vs UOI AIR 1997 SCDocument27 pagesCase Commentary L Chandra Kumar Vs UOI AIR 1997 SCALOK RAONo ratings yet

- Growth of Legal Profession InindiaDocument13 pagesGrowth of Legal Profession InindiaAnonymous100% (1)

- Article On Section - 165 of E. Act PDFDocument54 pagesArticle On Section - 165 of E. Act PDFNoXiouSGT GamingNo ratings yet

- Project Report: Freedom of Speech and Expression Under Article 19 (1) (A)Document12 pagesProject Report: Freedom of Speech and Expression Under Article 19 (1) (A)jaishreeNo ratings yet

- Advocates Right To Strike in The Light of Ex Captain Harrishuppal v. Union of India and Anr. 3Document9 pagesAdvocates Right To Strike in The Light of Ex Captain Harrishuppal v. Union of India and Anr. 3Kalyani dasariNo ratings yet

- Scheme of CPCDocument3 pagesScheme of CPCsubham agrawalNo ratings yet

- It ProjectDocument23 pagesIt ProjectsoumilNo ratings yet

- The Right To Information ActDocument10 pagesThe Right To Information ActsimranNo ratings yet

- I.C. Golaknath and Ors. Vs State of Punjab and Anrs. - Wikipedia PDFDocument18 pagesI.C. Golaknath and Ors. Vs State of Punjab and Anrs. - Wikipedia PDFHarshdeep SinghNo ratings yet

- Notes On PO ActDocument11 pagesNotes On PO ActManas Ranjan SamantarayNo ratings yet

- Case Commentary On Vishakha Vs State of RajasthanDocument6 pagesCase Commentary On Vishakha Vs State of RajasthanDebapom PurkayasthaNo ratings yet

- Law of EvidenceDocument40 pagesLaw of EvidenceDipanshu KambojNo ratings yet

- What Is Obscene in IndiaDocument5 pagesWhat Is Obscene in IndiaRadhika SinghNo ratings yet

- Role of Cci in Banking Mergers With Special Reference To Banking Law AmendmentDocument17 pagesRole of Cci in Banking Mergers With Special Reference To Banking Law AmendmentranjuNo ratings yet

- AbhinavDocument11 pagesAbhinavShubham AgrawalNo ratings yet

- Dr. Ram Manohar Lohiya National Law University Lucknow: Forest Conservation and The LawsDocument14 pagesDr. Ram Manohar Lohiya National Law University Lucknow: Forest Conservation and The Lawslokesh4nigamNo ratings yet

- Administrative Law Delegated LegislationDocument30 pagesAdministrative Law Delegated LegislationAkhilAhujaNo ratings yet

- CRPC Law - Rough DraftDocument3 pagesCRPC Law - Rough DraftAman KumarNo ratings yet

- Sheetal (Constitution Term Paper)Document11 pagesSheetal (Constitution Term Paper)Evil VipersNo ratings yet

- Subject The Code of Civil Procedure, 1908: Icfai University, Dehradun Icfai Law SchoolDocument15 pagesSubject The Code of Civil Procedure, 1908: Icfai University, Dehradun Icfai Law SchoolAshwina NamtaNo ratings yet

- The Doctrine of Pith and SubstanceDocument6 pagesThe Doctrine of Pith and SubstanceRathin BanerjeeNo ratings yet

- Doctrine of Separability in IndiaDocument4 pagesDoctrine of Separability in IndiaPolsani Ajit RaoNo ratings yet

- Delegated Legislation in India - Analysis and OverviewDocument22 pagesDelegated Legislation in India - Analysis and OverviewAditya RautNo ratings yet

- Criminal Law ProjectDocument12 pagesCriminal Law ProjectHrishikesh100% (1)

- Achmad Ardanu 20080694029 Chapter5Document13 pagesAchmad Ardanu 20080694029 Chapter5Achmad ArdanuNo ratings yet

- Easy Problem Chapter 6Document4 pagesEasy Problem Chapter 6Natally LangfeldtNo ratings yet

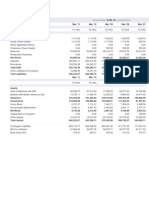

- Balance Sheet of ICICI BankDocument3 pagesBalance Sheet of ICICI Banknikitagupta44No ratings yet

- CH 08 PDFDocument37 pagesCH 08 PDFErizal WibisonoNo ratings yet

- AFA 3e PPT Chap04Document24 pagesAFA 3e PPT Chap04Phạm Ngọc ÁnhNo ratings yet

- Capstone - Edmonton Capital Project PrioritizationDocument41 pagesCapstone - Edmonton Capital Project PrioritizationMahesh KumarNo ratings yet

- iDempiereDocBook PDFDocument2,572 pagesiDempiereDocBook PDFDJ JAMNo ratings yet

- Divestiture SDocument26 pagesDivestiture SJoshua JoelNo ratings yet

- Business Plan Outline & FormatDocument5 pagesBusiness Plan Outline & FormatMichelle TagalogNo ratings yet

- Profits & Gains From Business/Profession: Important Amendments/ Notifications/CircularsDocument16 pagesProfits & Gains From Business/Profession: Important Amendments/ Notifications/CircularsHemant AherNo ratings yet

- Godrej Consumer Products Limited 44 QuarterUpdateDocument9 pagesGodrej Consumer Products Limited 44 QuarterUpdateKhushboo SharmaNo ratings yet

- 157 28395 EY111 2013 4 2 1 Chap004Document91 pages157 28395 EY111 2013 4 2 1 Chap004David SelfanyNo ratings yet

- 11 3 Demands For Grants Appropriations Current Exp Vol III 2021 22Document837 pages11 3 Demands For Grants Appropriations Current Exp Vol III 2021 22Aamir HamaadNo ratings yet

- A Study On The Financial Analysis of Reliance Industries LimitedDocument13 pagesA Study On The Financial Analysis of Reliance Industries LimitedIJAR JOURNAL100% (1)

- A Guide To Basic Procedures of Corporate Law For Young LawyersDocument72 pagesA Guide To Basic Procedures of Corporate Law For Young LawyersMaulik shahNo ratings yet

- Partnership and Corporation Accounting Chapter 1 SolManDocument11 pagesPartnership and Corporation Accounting Chapter 1 SolManDavid BarletaNo ratings yet

- Barber Shop Business PlanDocument25 pagesBarber Shop Business PlanStephen FrancisNo ratings yet

- UT Dallas Syllabus For Aim2301.003 06s Taught by Xiaohui Liu (xxl046000)Document5 pagesUT Dallas Syllabus For Aim2301.003 06s Taught by Xiaohui Liu (xxl046000)UT Dallas Provost's Technology GroupNo ratings yet

- Timex Case StudyDocument36 pagesTimex Case StudyShrey KashyapNo ratings yet

- Investments Background and IssuesDocument9 pagesInvestments Background and Issuespiepkuiken-knipper0jNo ratings yet

- CH 07Document29 pagesCH 07varunragav85No ratings yet

- Allen Stanford Criminal Trial Transcript Volume 8 Feb. 1, 2012Document332 pagesAllen Stanford Criminal Trial Transcript Volume 8 Feb. 1, 2012Stanford Victims CoalitionNo ratings yet

- CIT, Kolkata V Smifs SecuritiesDocument4 pagesCIT, Kolkata V Smifs SecuritiesBar & BenchNo ratings yet

- Biological AssetDocument4 pagesBiological AssetSherilyn Maligson100% (1)

- Cosmetics Manufacturing Business PlanDocument63 pagesCosmetics Manufacturing Business PlanShihabul Islam ShihabNo ratings yet

- Module 7 - Prob A-C Valuation and Concepts AnswersDocument2 pagesModule 7 - Prob A-C Valuation and Concepts Answersvenice cambryNo ratings yet

- Unit 3-Recording of TransactionDocument20 pagesUnit 3-Recording of Transactionanamikarajendran441998No ratings yet

- Tata Motors: 2. Impairment of Tangible and Intangible AssetsDocument2 pagesTata Motors: 2. Impairment of Tangible and Intangible AssetsTanishq RijalNo ratings yet

- Top 100 Questions of AccountsDocument75 pagesTop 100 Questions of Accountschauhanthakur554No ratings yet

- Amalgamation SummaryDocument26 pagesAmalgamation SummaryPrashant SharmaNo ratings yet