You might also like

- Audit Risk Alert: Government Auditing Standards and Single Audit Developments: Strengthening Audit Integrity 2018/19From EverandAudit Risk Alert: Government Auditing Standards and Single Audit Developments: Strengthening Audit Integrity 2018/19No ratings yet

- Audit Risk Alert: General Accounting and Auditing Developments 2018/19From EverandAudit Risk Alert: General Accounting and Auditing Developments 2018/19No ratings yet

- UntitledDocument5 pagesUntitledKriztel Loriene TribianaNo ratings yet

- Tqs Finals Operations-AuditDocument46 pagesTqs Finals Operations-AuditCristel TannaganNo ratings yet

- Long Quiz On Internal AuditingDocument4 pagesLong Quiz On Internal Auditingrizzamaybacarra.birNo ratings yet

- Iath PrelimDocument7 pagesIath PrelimMara LacsamanaNo ratings yet

- At.02 Introduction To Audit of Historical Financial InformationDocument4 pagesAt.02 Introduction To Audit of Historical Financial InformationAngelica Sanchez de VeraNo ratings yet

- Unit TestDocument6 pagesUnit TestMajoy BantocNo ratings yet

- Intro To IA Quiz 1Document16 pagesIntro To IA Quiz 1Jao FloresNo ratings yet

- Audit Assessment True or False and MCQ - CompressDocument8 pagesAudit Assessment True or False and MCQ - CompressHazel BawasantaNo ratings yet

- Short Quiz 1Document11 pagesShort Quiz 1AMNo ratings yet

- AUDITTHEODocument13 pagesAUDITTHEOAlisonNo ratings yet

- Practice PeDocument12 pagesPractice PeRhea EnocNo ratings yet

- Acctg 14 Final ExamDocument8 pagesAcctg 14 Final ExamErineNo ratings yet

- 111年會考 審計學題庫Document15 pages111年會考 審計學題庫張巧薇No ratings yet

- Auditing Theory Quiz Final PrintDocument6 pagesAuditing Theory Quiz Final Printnda0403No ratings yet

- Final Exam Gbermic Multiple ChoiceDocument5 pagesFinal Exam Gbermic Multiple ChoiceMarie GarpiaNo ratings yet

- AUDITINGDocument20 pagesAUDITINGAngelieNo ratings yet

- Quizzer GOvernance Student Copy 1Document9 pagesQuizzer GOvernance Student Copy 1Mella FranciscoNo ratings yet

- Practice Questions - Module 5Document8 pagesPractice Questions - Module 5Rosda DhangNo ratings yet

- Irector's First Task Is To Develop A Charter. Identify The Item That Should BeDocument105 pagesIrector's First Task Is To Develop A Charter. Identify The Item That Should BeNICELLE TAGLENo ratings yet

- Questions and AnswersDocument20 pagesQuestions and AnswersJi YuNo ratings yet

- 01 Definition of Internal AuditingDocument11 pages01 Definition of Internal AuditingMhmd Habbosh100% (2)

- Audit 1Document1 pageAudit 1zennongraeNo ratings yet

- Trắc nghiệm kiểmDocument8 pagesTrắc nghiệm kiểmJF FNo ratings yet

- Auditing Theory-2018Document26 pagesAuditing Theory-2018Suzette VillalinoNo ratings yet

- Considerations of Internal Control Psa-Based QuestionsDocument28 pagesConsiderations of Internal Control Psa-Based QuestionsNoro75% (4)

- Introduction To Internal Auditing: Practice Questions and AnswersDocument3 pagesIntroduction To Internal Auditing: Practice Questions and AnswersPeter CR7No ratings yet

- Asr-Prelim ExamDocument11 pagesAsr-Prelim ExamCyndy VillapandoNo ratings yet

- Auditing TheoryDocument6 pagesAuditing TheoryJoy AbingNo ratings yet

- Consideration of Internal ControlDocument4 pagesConsideration of Internal ControlMary Grace SalcedoNo ratings yet

- CHAP 26. Internal and Government Financial Auditing and Operational AuditinDocument16 pagesCHAP 26. Internal and Government Financial Auditing and Operational AuditinNoroNo ratings yet

- Auditing Theory - Quiz 1Document5 pagesAuditing Theory - Quiz 1MA ValdezNo ratings yet

- Long Quiz 2Document8 pagesLong Quiz 2KathleenNo ratings yet

- Aud 1.1.1Document3 pagesAud 1.1.1Marjorie BernasNo ratings yet

- Auditing 2nd Sem AY 2020-2021 Institutional Mock Board ExamDocument10 pagesAuditing 2nd Sem AY 2020-2021 Institutional Mock Board ExamGet BurnNo ratings yet

- Department of Accounting Education: JULY 17, 2017Document4 pagesDepartment of Accounting Education: JULY 17, 2017Jao FloresNo ratings yet

- AT Quiz 1Document2 pagesAT Quiz 1CattleyaNo ratings yet

- IIa CIA Part1Document7 pagesIIa CIA Part1AMIT_AGRAHARI111987No ratings yet

- Quiz 2 Set ADocument3 pagesQuiz 2 Set AShiela RengelNo ratings yet

- AT ReviewerDocument10 pagesAT Reviewerfer maNo ratings yet

- Auditing ReviewerDocument8 pagesAuditing ReviewerSeanaNo ratings yet

- AUD ReviewerDocument9 pagesAUD ReviewerMhaybelle JovellanoNo ratings yet

- Quiz 1 & 2 (Aud) - MarcoletaDocument4 pagesQuiz 1 & 2 (Aud) - MarcoletaLeane MarcoletaNo ratings yet

- Question in Auditing TheoryDocument20 pagesQuestion in Auditing TheoryJeric YangNo ratings yet

- Auditing Theory Q and ADocument28 pagesAuditing Theory Q and ANyra BeldoroNo ratings yet

- Reviewer Auditing TheoryDocument59 pagesReviewer Auditing Theoryunexpected thingsNo ratings yet

- Auditing Theory SalosagcolDocument4 pagesAuditing Theory SalosagcolYuki CrossNo ratings yet

- Basic AudDocument3 pagesBasic AudMary Rose JuanNo ratings yet

- Seatwork#1Document14 pagesSeatwork#1Tricia Mae FernandezNo ratings yet

- Operations Auditing Quiz #1: A. Exercise Their Individual JudgmentDocument5 pagesOperations Auditing Quiz #1: A. Exercise Their Individual JudgmentCharleene GutierrezNo ratings yet

- Chapter 6 MC Bank For Opportunity-Student VersionDocument8 pagesChapter 6 MC Bank For Opportunity-Student VersionLivia WangNo ratings yet

- CPAR 1stPBDocument12 pagesCPAR 1stPBMae Danica CalunsagNo ratings yet

- Comprehensive Reviewer Auditing TheoryDocument91 pagesComprehensive Reviewer Auditing TheoryMary Rose JuanNo ratings yet

- Auditing Theory - 1Document9 pagesAuditing Theory - 1Kageyama HinataNo ratings yet

- True / False QuestionsDocument19 pagesTrue / False QuestionsRizza OmalinNo ratings yet

- Annual Update and Practice Issues for Preparation, Compilation, and Review EngagementsFrom EverandAnnual Update and Practice Issues for Preparation, Compilation, and Review EngagementsNo ratings yet

- Mastering Internal Audit Fundamentals A Step-by-Step ApproachFrom EverandMastering Internal Audit Fundamentals A Step-by-Step ApproachRating: 4 out of 5 stars4/5 (1)

- Acceptance Payment Form: Tax Amnesty On DelinquenciesDocument1 pageAcceptance Payment Form: Tax Amnesty On DelinquenciesJennyMariedeLeonNo ratings yet

- C2 PPT Pipe Jacking PVCDocument43 pagesC2 PPT Pipe Jacking PVCvroogh primeNo ratings yet

- MGP Paranoia - Troubles by The BoxloadDocument26 pagesMGP Paranoia - Troubles by The BoxloadAurik Frey100% (1)

- 200400: Company Accounting Topic 3: Accounting For Company Income TaxDocument15 pages200400: Company Accounting Topic 3: Accounting For Company Income TaxEhtesham HaqueNo ratings yet

- BioplasticDocument5 pagesBioplasticclaire bernadaNo ratings yet

- Sample Fryer Rabbit Budget PDFDocument2 pagesSample Fryer Rabbit Budget PDFGrace NacionalNo ratings yet

- Role of Financial Markets and InstitutionsDocument15 pagesRole of Financial Markets and Institutionsনাহিদ উকিল জুয়েলNo ratings yet

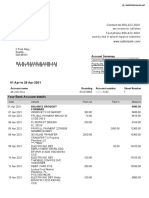

- Sutton Bank StatementDocument2 pagesSutton Bank StatementNadiia AvetisianNo ratings yet

- Awnser KeyDocument3 pagesAwnser KeyChristopher FulbrightNo ratings yet

- JPM - Economic Data AnalysisDocument11 pagesJPM - Economic Data AnalysisAvid HikerNo ratings yet

- Guidance Note On GSTDocument50 pagesGuidance Note On GSTkjs gurnaNo ratings yet

- Dao29 2004Document17 pagesDao29 2004Quinnee VallejosNo ratings yet

- 2010-02-01 IAPMO Green Plumbing and Mechanical Code SupplementDocument1 page2010-02-01 IAPMO Green Plumbing and Mechanical Code SupplementnedalmasaderNo ratings yet

- Case AnalysisDocument3 pagesCase AnalysisAnurag KhandelwalNo ratings yet

- 5% Compound PlanDocument32 pages5% Compound PlanArvind SinghNo ratings yet

- Education and Social DevelopmentDocument30 pagesEducation and Social DevelopmentMichelleAlejandroNo ratings yet

- Travel and Expense Policy: PurposeDocument9 pagesTravel and Expense Policy: Purposeabel_kayelNo ratings yet

- Annexure - VI Deed of Hypothecation (To Be Executed On Non Judicial Stamp Paper of Appropriate Value)Document3 pagesAnnexure - VI Deed of Hypothecation (To Be Executed On Non Judicial Stamp Paper of Appropriate Value)Deepesh MittalNo ratings yet

- AssignmentDocument13 pagesAssignmentabdur RahmanNo ratings yet

- 140 048 WashingtonStateTobaccoRetailerListDocument196 pages140 048 WashingtonStateTobaccoRetailerListAli MohsinNo ratings yet

- Indian MFTrackerDocument1,597 pagesIndian MFTrackerAnkur Mittal100% (1)

- Folder Gründen in Wien Englisch Web 6-10-17Document6 pagesFolder Gründen in Wien Englisch Web 6-10-17rodicabaltaNo ratings yet

- Aid For TradeDocument6 pagesAid For TradeRajasekhar AllamNo ratings yet

- Biznis Plan MLIN EngDocument16 pagesBiznis Plan MLIN EngBoris ZecNo ratings yet

- Macroeconomics - Assignment IIDocument6 pagesMacroeconomics - Assignment IIRahul Thapa MagarNo ratings yet

- SaleDocument1 pageSaleMegan HerreraNo ratings yet

- Mackinac Center Exposed: Who's Running Michigan?Document19 pagesMackinac Center Exposed: Who's Running Michigan?progressmichiganNo ratings yet

- The Simple Keynesian ModelDocument9 pagesThe Simple Keynesian ModelRudraraj MalikNo ratings yet

- Project Profile ON Roasted Rice FlakesDocument7 pagesProject Profile ON Roasted Rice FlakesPrafulla ChandraNo ratings yet

- Assignment - Engro CorpDocument18 pagesAssignment - Engro CorpUmar ButtNo ratings yet