You might also like

- Central Excise Act valuation methodsDocument6 pagesCentral Excise Act valuation methodsChandu Aradhya S RNo ratings yet

- Latest Updates in Indirect Tax Law – 30.04.2014Document12 pagesLatest Updates in Indirect Tax Law – 30.04.2014Saurav KakkarNo ratings yet

- What Is Assess Able ValueDocument3 pagesWhat Is Assess Able ValueMM_Ritesh0% (2)

- IDT UPDATESDocument21 pagesIDT UPDATESsivanpillai ganesanNo ratings yet

- Job Work ValuationDocument3 pagesJob Work Valuationpr_abhatNo ratings yet

- Implications On The Industries IFRS 15Document11 pagesImplications On The Industries IFRS 15Liyana ChuaNo ratings yet

- Tax IshritaDocument15 pagesTax IshritaManeesh ReddyNo ratings yet

- Impact of New Revenue Rules for FranchisorsDocument25 pagesImpact of New Revenue Rules for FranchisorsTag SenNo ratings yet

- CAS - 15 Cost Accounting Standard On Selling and Distribution OverheadsDocument5 pagesCAS - 15 Cost Accounting Standard On Selling and Distribution Overheadsumesh hivreNo ratings yet

- 4 Recognition PrinciplesDocument7 pages4 Recognition PrinciplesShamae Duma-anNo ratings yet

- Ifrs 15 (Telecom Industry)Document19 pagesIfrs 15 (Telecom Industry)Emezi Francis Obisike100% (2)

- IFRS 15 - Revenue From Contracts With CustomersDocument5 pagesIFRS 15 - Revenue From Contracts With CustomersAnkur MittalNo ratings yet

- OECD Discussion Draft Implementation Guidance On HTVIDocument8 pagesOECD Discussion Draft Implementation Guidance On HTVIMario AlfaroNo ratings yet

- PWC Reportinginbrief Companies Indian Accounting Standards Amendment Rules 2018Document12 pagesPWC Reportinginbrief Companies Indian Accounting Standards Amendment Rules 2018sourabhbansal108No ratings yet

- Module 7 - Revenue Recognition - StudentsDocument10 pagesModule 7 - Revenue Recognition - StudentsLuisito CorreaNo ratings yet

- Philippine Interpretations Committee (Pic) Questions and Answers (Q&A) Q&A No. 2018-12 Pfrs 15 Implementation Issues Affecting The Real Estate IndustryDocument54 pagesPhilippine Interpretations Committee (Pic) Questions and Answers (Q&A) Q&A No. 2018-12 Pfrs 15 Implementation Issues Affecting The Real Estate IndustryJaey EmmNo ratings yet

- Engage - Revenue Recognition-1Document129 pagesEngage - Revenue Recognition-1Johhahawie jajwiNo ratings yet

- Ifrs 2Document4 pagesIfrs 2v0524 vNo ratings yet

- Central Excise: Meenal P WagleDocument15 pagesCentral Excise: Meenal P WagleMeenal Prasad WagleNo ratings yet

- Recent Advances in Cost Accounting and Cost SystemDocument6 pagesRecent Advances in Cost Accounting and Cost SystemDeepak ChandekarNo ratings yet

- Valuation MethodDocument3 pagesValuation MethodviganjorebicNo ratings yet

- IAS 18 Part B RevenueDocument10 pagesIAS 18 Part B RevenueKatreena Mae ConstantinoNo ratings yet

- CASE OF VALUATION UNDER CUSTOM sc2015 (1)Document40 pagesCASE OF VALUATION UNDER CUSTOM sc2015 (1)Anurag PandeyNo ratings yet

- PFRS 15, MarbellaDocument3 pagesPFRS 15, MarbellaDazzelle BasarteNo ratings yet

- Tax Planning Mgt. DecisionsDocument18 pagesTax Planning Mgt. Decisionsnandan velankarNo ratings yet

- Transfer Pricing CasesDocument6 pagesTransfer Pricing CasesShreya SinghNo ratings yet

- Question On IFRS 15Document2 pagesQuestion On IFRS 15Adeleke TemitayoNo ratings yet

- Ifrs 2 Share-Based PaymentDocument8 pagesIfrs 2 Share-Based Paymentmomentsof_joyNo ratings yet

- Conceptual Framework (Part 2) : AssetsDocument3 pagesConceptual Framework (Part 2) : AssetsEui KimNo ratings yet

- Historical Cost of Property, Plant and EquipmentDocument9 pagesHistorical Cost of Property, Plant and EquipmentChinchin Ilagan DatayloNo ratings yet

- RefundDocument6 pagesRefundManish K JadhavNo ratings yet

- US Internal Revenue Service: 20070601fDocument7 pagesUS Internal Revenue Service: 20070601fIRSNo ratings yet

- IFRS 15 Bill-and-Hold Guidance for Custodial ServicesDocument4 pagesIFRS 15 Bill-and-Hold Guidance for Custodial Servicesiqbal.ais152No ratings yet

- Dec 2011: Qualitative Evaluation To Determine The Necessity of Step 1 of The Goodwill Impairment TestDocument6 pagesDec 2011: Qualitative Evaluation To Determine The Necessity of Step 1 of The Goodwill Impairment TestSingerLewakNo ratings yet

- IFRS Industry Insights MiningDocument4 pagesIFRS Industry Insights MiningKevin LukitoNo ratings yet

- Studet Practical Accounting Ch17 PPE AcquisitionDocument16 pagesStudet Practical Accounting Ch17 PPE Acquisitionsabina del monteNo ratings yet

- Chapter 6 - IFRS 15Document21 pagesChapter 6 - IFRS 15SaiNo ratings yet

- Summary of IFRS 2Document11 pagesSummary of IFRS 2Juanito TanamorNo ratings yet

- Revenue Recognition: Accounting Standard (AS) 9Document13 pagesRevenue Recognition: Accounting Standard (AS) 9Abhishek SinghNo ratings yet

- FB Mytashanfb348#$Document9 pagesFB Mytashanfb348#$RatanaRoulNo ratings yet

- Chapter 17 - Ppe - AssignmentDocument16 pagesChapter 17 - Ppe - Assignmentsabina del monteNo ratings yet

- Chapter 3 Revenue From Contracts With CustomersDocument6 pagesChapter 3 Revenue From Contracts With CustomersClint AbenojaNo ratings yet

- Name:: Faisal Masoud Hussein Sous University ID: 1835648 Division / Seat Number: 1/46Document8 pagesName:: Faisal Masoud Hussein Sous University ID: 1835648 Division / Seat Number: 1/46زهرة البنفسجNo ratings yet

- 28548vol3stvatcp14 PDFDocument5 pages28548vol3stvatcp14 PDFNaveed AnsariNo ratings yet

- Accounting of ReceivableDocument34 pagesAccounting of ReceivableAnnette Marie Noprada RosasNo ratings yet

- Capital GainsDocument8 pagesCapital GainsSarfaraz Singh LegaNo ratings yet

- Chapter 38 Revenue From Contracts With CustomersDocument10 pagesChapter 38 Revenue From Contracts With CustomersEllen MaskariñoNo ratings yet

- Vol 3 Secaidtccp 9Document7 pagesVol 3 Secaidtccp 9timirkantaNo ratings yet

- EY Devel80 Revenue May2014Document4 pagesEY Devel80 Revenue May2014Tanjim TanimNo ratings yet

- Discounts Incentives GST ImplicationsDocument12 pagesDiscounts Incentives GST ImplicationsVrajesh PatelNo ratings yet

- GST Unit 3Document61 pagesGST Unit 3SANSKRITI YADAV 22DM236No ratings yet

- IFRS 15 Revenue From Contracts With CustomersDocument5 pagesIFRS 15 Revenue From Contracts With CustomersADEYANJU AKEEMNo ratings yet

- Caterpillar Cost of Poor Quality (Copq) AgreementDocument6 pagesCaterpillar Cost of Poor Quality (Copq) AgreementMy Dad My WorldNo ratings yet

- Ifrs 15Document10 pagesIfrs 15Kuti KuriNo ratings yet

- CFAS Unit 1 - Module 5.1Document11 pagesCFAS Unit 1 - Module 5.1Ralph Lefrancis DomingoNo ratings yet

- MODULE 3 - NotesDocument5 pagesMODULE 3 - NotesAravind YogeshNo ratings yet

- Merge and Acquisition 2Document4 pagesMerge and Acquisition 2Bryan Ivann MacasinagNo ratings yet

- 1040 Exam Prep Module III: Items Excluded from Gross IncomeFrom Everand1040 Exam Prep Module III: Items Excluded from Gross IncomeRating: 1 out of 5 stars1/5 (1)

- VinayShraff CVDocument2 pagesVinayShraff CVapi-3822396No ratings yet

- VinayShraff ProfileDocument4 pagesVinayShraff Profileapi-3822396No ratings yet

- Vinay Shraff CVDocument4 pagesVinay Shraff CVapi-3822396No ratings yet

- Service Tax - 2003Document13 pagesService Tax - 2003api-3822396No ratings yet

- Securitization 2002Document26 pagesSecuritization 2002api-3822396No ratings yet

- Value Added TaxationDocument6 pagesValue Added Taxationapi-3822396No ratings yet

- Transfer PricingDocument1 pageTransfer Pricingapi-3822396No ratings yet

- Show Cause Mandatory Requirement For Raising DemandDocument5 pagesShow Cause Mandatory Requirement For Raising Demandapi-3822396No ratings yet

- SSI BenefitDocument3 pagesSSI Benefitapi-3822396No ratings yet

- Tax Planning - CEDocument10 pagesTax Planning - CEapi-3822396No ratings yet

- Securitization ACTDocument9 pagesSecuritization ACTapi-3822396100% (1)

- Service TaxDocument3 pagesService Taxapi-3822396No ratings yet

- Fema-17 1Document43 pagesFema-17 1api-3822396No ratings yet

- NRI InvestmentDocument9 pagesNRI Investmentapi-3822396100% (2)

- Professional Opportunities in Central ExciseDocument8 pagesProfessional Opportunities in Central Exciseapi-3822396100% (1)

- Transfer PricingDocument3 pagesTransfer Pricingapi-3822396No ratings yet

- Production of Additional EvidenceDocument2 pagesProduction of Additional Evidenceapi-3822396No ratings yet

- Music 3d-VeDocument4 pagesMusic 3d-Veapi-3822396100% (3)

- Why VATDocument10 pagesWhy VATapi-3822396No ratings yet

- Financial Due DiligenceDocument10 pagesFinancial Due Diligenceapi-3822396100% (6)

- Central Excise ScopeDocument2 pagesCentral Excise Scopeapi-3822396100% (3)

- Incentives - New Industrial UnitDocument3 pagesIncentives - New Industrial Unitapi-3822396No ratings yet

- Capital Gain - Land or Building or BothDocument4 pagesCapital Gain - Land or Building or Bothapi-3822396No ratings yet

- Applicability of ST On ISPDocument3 pagesApplicability of ST On ISPapi-3822396No ratings yet

- Budget 2004-05 UpdateDocument5 pagesBudget 2004-05 Updateapi-3822396No ratings yet

- Taxation BelanisDocument3 pagesTaxation Belanisapi-3822396No ratings yet

- Benefit Sales TaxDocument3 pagesBenefit Sales Taxapi-3822396No ratings yet

- Tax Holiday Provisions in Respect of Newly Established Hundred Percent Export Oriented UndertakingsDocument1 pageTax Holiday Provisions in Respect of Newly Established Hundred Percent Export Oriented Undertakingsapi-3822396No ratings yet

- Partition Deed (Huf)Document3 pagesPartition Deed (Huf)api-382239685% (13)

- Zegeye TadesseDocument117 pagesZegeye Tadessedagim ayenewNo ratings yet

- Elderly SeminarDocument20 pagesElderly SeminarPriyanka NilewarNo ratings yet

- Suppose That, in Certain Economy, One Firm Is The ...Document1 pageSuppose That, in Certain Economy, One Firm Is The ...waniNo ratings yet

- GuideWire PolicyCenter Academy Course V1.0 Version 9 1031Document320 pagesGuideWire PolicyCenter Academy Course V1.0 Version 9 1031Amudha Nataraj100% (2)

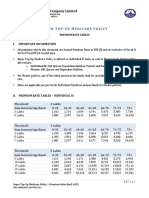

- Super Top-Up Medicare Policy Premium Chart - Including GSTDocument6 pagesSuper Top-Up Medicare Policy Premium Chart - Including GSTvinay_814585077No ratings yet

- Demystifying IFRS 17 - Philip JacksonDocument26 pagesDemystifying IFRS 17 - Philip JacksonWubneh AlemuNo ratings yet

- Leaflet - Medisure Plus - 150914Document2 pagesLeaflet - Medisure Plus - 150914Rajarshi GuhaNo ratings yet

- Chapter 10 SlidesDocument35 pagesChapter 10 SlidesEmily AirhartNo ratings yet

- PCE Sample Questions (Eng) - Set 1Document20 pagesPCE Sample Questions (Eng) - Set 1Thennarasu Don100% (1)

- TAX UPDATE ON SALARY IN PAKISTAN FOR TAX YEAR 2020Document1 pageTAX UPDATE ON SALARY IN PAKISTAN FOR TAX YEAR 2020Malik Muhammad MuzamilNo ratings yet

- CIR V Lincoln Philippine LifeDocument2 pagesCIR V Lincoln Philippine LifeViolet Parker100% (3)

- Travel Guard BrochureDocument2 pagesTravel Guard BrochureAnjali GuptaNo ratings yet

- Loadstar Shipping Co., Inc. vs. Court of Appeals (1999)Document14 pagesLoadstar Shipping Co., Inc. vs. Court of Appeals (1999)Angelette BulacanNo ratings yet

- List of Attorneys March 2018Document21 pagesList of Attorneys March 2018LOVETH KONNIANo ratings yet

- Presented By:-: Nandini Verma & Shabnam Sultana Begum SemesterDocument8 pagesPresented By:-: Nandini Verma & Shabnam Sultana Begum SemesterNandini VermaNo ratings yet

- IFRS 17 - Insurance Contacts Technical Summary of IFRS 17: ObjectiveDocument8 pagesIFRS 17 - Insurance Contacts Technical Summary of IFRS 17: ObjectiveAhmadi SemahNo ratings yet

- Taxation ProblemsDocument6 pagesTaxation ProblemsanggandakonohNo ratings yet

- All Hazards Risk and Resilience - Prioritizing Critical Infrastructure Using The RAMCAP Plus (SM) ApproachDocument169 pagesAll Hazards Risk and Resilience - Prioritizing Critical Infrastructure Using The RAMCAP Plus (SM) Approachlijl620902No ratings yet

- Manage Workplace Health for Legal, Moral and Financial ReasonsDocument4 pagesManage Workplace Health for Legal, Moral and Financial ReasonsAbd Errahmane100% (3)

- Case DigestDocument138 pagesCase DigestMelani Chiquillo CalcetaNo ratings yet

- Deel-Vonzelle Brown-Contract-M7np4nnDocument16 pagesDeel-Vonzelle Brown-Contract-M7np4nnMaryam AmbaliNo ratings yet

- Unum Selects Majesco Policy For L&A and Group and Majesco Billing To Transform Its U.S. Business (Company Update)Document4 pagesUnum Selects Majesco Policy For L&A and Group and Majesco Billing To Transform Its U.S. Business (Company Update)Shyam SunderNo ratings yet

- Investments in Debt Securities and Other Non-Current AssetsDocument14 pagesInvestments in Debt Securities and Other Non-Current AssetsMarjorie NepomucenoNo ratings yet

- Guingon V Del MonteDocument1 pageGuingon V Del MonteCzar Ian AgbayaniNo ratings yet

- JCT 2011 - GuideDocument36 pagesJCT 2011 - GuideHelloNo ratings yet

- Overseas Mediclaim Policy (Business and Holiday) Policy ScheduleDocument6 pagesOverseas Mediclaim Policy (Business and Holiday) Policy Schedulemohamed arabathNo ratings yet

- A Complaint Is A GiftDocument8 pagesA Complaint Is A GiftSRIDHAR SUBRAMANIAMNo ratings yet

- Deposit InsuranceBrochure FinalDocument2 pagesDeposit InsuranceBrochure FinalKatreena Mae ConstantinoNo ratings yet

- Jamil InsuranceDocument5 pagesJamil InsuranceAli HamzaNo ratings yet

- ULTRA AgreementDocument19 pagesULTRA Agreemental_crespoNo ratings yet