You might also like

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Millennial Media Q1'13 Mobile Mix ReportDocument7 pagesMillennial Media Q1'13 Mobile Mix ReportMobileLeadersNo ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- AdTheorent Real Time Learning Machine: White PaperDocument10 pagesAdTheorent Real Time Learning Machine: White PaperMobileLeadersNo ratings yet

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Millennial Media: Special January Mix Report - Mobile Gaming ApplicationsDocument5 pagesMillennial Media: Special January Mix Report - Mobile Gaming ApplicationsMobileLeadersNo ratings yet

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Appcelerator Report Q3 2012 FinalDocument13 pagesAppcelerator Report Q3 2012 FinalMobileLeadersNo ratings yet

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- q2 12 Rhythm Insights WebsiteDocument21 pagesq2 12 Rhythm Insights WebsiteMobileLeadersNo ratings yet

- SBA-RFID Feasibility StudyDocument13 pagesSBA-RFID Feasibility StudyMobileLeadersNo ratings yet

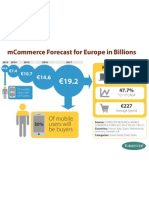

- Mobile Commerce Infographic GillDocument1 pageMobile Commerce Infographic GillMobileLeadersNo ratings yet

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- TheConnectedMillennials JiWireINFOGRAPHIC 10-10-11Document1 pageTheConnectedMillennials JiWireINFOGRAPHIC 10-10-11MobileLeadersNo ratings yet

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Components of .Net Framework, CLR, CTS, CLS, Base Class LibraryDocument14 pagesComponents of .Net Framework, CLR, CTS, CLS, Base Class LibraryShruti Daddy's AngelNo ratings yet

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Vista Plus Windows Client Users GuideDocument295 pagesVista Plus Windows Client Users Guideparvathi12100% (1)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Vlsi2022 C19-4Document76 pagesVlsi2022 C19-4himmel17No ratings yet

- Audiocodes Mediant Sbcs For Service ProvidersDocument9 pagesAudiocodes Mediant Sbcs For Service ProvidersrAVINo ratings yet

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Cloud Computing Assignment-1 (Virtualization)Document18 pagesCloud Computing Assignment-1 (Virtualization)DarshpreetKaurNo ratings yet

- Hikvision DDNS Management System20130216Document8 pagesHikvision DDNS Management System20130216Ankush TandonNo ratings yet

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- CCNA Exp3 - Chapter02 - Basic Switch Concepts and Configurations - DPFDocument132 pagesCCNA Exp3 - Chapter02 - Basic Switch Concepts and Configurations - DPFhttp://heiserz.com/No ratings yet

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- Guias de PracticaDocument71 pagesGuias de PracticaCarlos VillonNo ratings yet

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- AngularJS Tutorial W3SchoolsDocument43 pagesAngularJS Tutorial W3SchoolsAnonymous 7r9SDmn7Ee100% (1)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Sangoma Transcoder Installation GuideDocument4 pagesSangoma Transcoder Installation Guideedgar_3372No ratings yet

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Manual Proficore InstallationDocument19 pagesManual Proficore InstallationEng. Eletronics MscNo ratings yet

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Samsung UE40C8000 ManualDocument66 pagesSamsung UE40C8000 ManualChisvasiSebastianNo ratings yet

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- 50pug6513 77 Fhi AspDocument2 pages50pug6513 77 Fhi Aspgiovanniusach631No ratings yet

- Paper By:: Thunuguntla Gayathri Vusthepalli SravaniDocument7 pagesPaper By:: Thunuguntla Gayathri Vusthepalli SravaniNaga Neelima ThunuguntlaNo ratings yet

- Matched FilterDocument30 pagesMatched FilterLavanya GangadharanNo ratings yet

- Yerrapothu Gnana Sai Raghu: ND STDocument2 pagesYerrapothu Gnana Sai Raghu: ND STSai RaghuNo ratings yet

- F2y DatabaseDocument28 pagesF2y Databaseapi-272851576No ratings yet

- Avr 1612 1622Document146 pagesAvr 1612 1622Ronald100% (1)

- ICT Premium Products Passwords SY 2019-2020Document8 pagesICT Premium Products Passwords SY 2019-2020Dharen Job CornelioNo ratings yet

- Multi Threading PDFDocument48 pagesMulti Threading PDFShweta Nikhar67% (3)

- ASHIDA RMU Automation BrochureDocument3 pagesASHIDA RMU Automation Brochurerahulyadav2121545No ratings yet

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- PVR PLUS User Manual (English)Document26 pagesPVR PLUS User Manual (English)Rel TabornalNo ratings yet

- Network Protocols PDFDocument39 pagesNetwork Protocols PDFMohan PreethNo ratings yet

- 2012 TV Firmware Upgrade Guide PDFDocument10 pages2012 TV Firmware Upgrade Guide PDFFauzi100% (1)

- Resource Allocation For Linux With Cgroups PresentationDocument25 pagesResource Allocation For Linux With Cgroups Presentationmyslef1234No ratings yet

- Intro Modeler Lab Manual 11.0 v3Document102 pagesIntro Modeler Lab Manual 11.0 v3Cecilia Camarena QuispeNo ratings yet

- PDFDocument28 pagesPDFMiraNo ratings yet

- Jenkins Fundamentals by Joseph MuliDocument263 pagesJenkins Fundamentals by Joseph MuliAnonymous H9062snl100% (2)

- Unit-III Micro-Programmed ControlDocument17 pagesUnit-III Micro-Programmed ControlchaitanyaNo ratings yet

- (Introducing Voice Over Ip Networks) : Voip FundamentalsDocument8 pages(Introducing Voice Over Ip Networks) : Voip FundamentalsRodmar Ferol MaligayaNo ratings yet

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)