You might also like

- Supply Chain ManagementDocument3 pagesSupply Chain ManagementShameem AnwarNo ratings yet

- Supply Chain ManagementDocument3 pagesSupply Chain ManagementShameem AnwarNo ratings yet

- Balmer LawrieDocument18 pagesBalmer LawrieShameem AnwarNo ratings yet

- Logistics Management Bba Unit 1 NotesDocument6 pagesLogistics Management Bba Unit 1 NotesShameem Anwar83% (6)

- International: Supply Chain ManagementDocument6 pagesInternational: Supply Chain ManagementShameem AnwarNo ratings yet

- International: Supply Chain ManagementDocument6 pagesInternational: Supply Chain ManagementShameem AnwarNo ratings yet

- Working Capital ManagementDocument8 pagesWorking Capital ManagementShameem AnwarNo ratings yet

- ProjectDocument80 pagesProjectShameem AnwarNo ratings yet

- UNIT NO 1 - FM AMSDocument57 pagesUNIT NO 1 - FM AMSShameem AnwarNo ratings yet

- Results of The StudyDocument8 pagesResults of The StudyShameem AnwarNo ratings yet

- Questionnaire Kindly Indicate Your Answer As Follows: Strongly Disagree 1 Disagree 2 Neither Agree Nor Disagree 3 Agree 4 Strongly Agree 5Document2 pagesQuestionnaire Kindly Indicate Your Answer As Follows: Strongly Disagree 1 Disagree 2 Neither Agree Nor Disagree 3 Agree 4 Strongly Agree 5Shameem AnwarNo ratings yet

- A Study On Derivatives and Its Trends in The Indian Capital Market A First Review ReportDocument6 pagesA Study On Derivatives and Its Trends in The Indian Capital Market A First Review ReportShameem AnwarNo ratings yet

- Social Media As HR Recruitment Tool: !CCCC CCC#CC"C C CCC CCCCCCCC C C CCCDocument6 pagesSocial Media As HR Recruitment Tool: !CCCC CCC#CC"C C CCC CCCCCCCC C C CCCShameem AnwarNo ratings yet

- Efficient Market HypothesisDocument3 pagesEfficient Market HypothesisShameem AnwarNo ratings yet

- A Study of Service Quality in The Hospitality Industry JMDocument12 pagesA Study of Service Quality in The Hospitality Industry JMShameem AnwarNo ratings yet

- A Study On Receivables ManagementDocument3 pagesA Study On Receivables ManagementShameem AnwarNo ratings yet

- Effect of Exchange Rate in Foreign Trade Part IVDocument23 pagesEffect of Exchange Rate in Foreign Trade Part IVShameem AnwarNo ratings yet

- Cultural IntegrationDocument3 pagesCultural IntegrationShameem AnwarNo ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Structure: Default and RepossessionDocument14 pagesStructure: Default and RepossessionAnkit KumarNo ratings yet

- Chapter 3Document47 pagesChapter 3Groove'N'Move GNMNo ratings yet

- Fs Unit-1 Important QuestionsDocument13 pagesFs Unit-1 Important QuestionsKarthick KumarNo ratings yet

- Sale of Goods Act 1930 Bare ActDocument18 pagesSale of Goods Act 1930 Bare ActPrateek KhandelwalNo ratings yet

- Final Assessment LAW416 Final Assessment LAW416Document12 pagesFinal Assessment LAW416 Final Assessment LAW416Haiman HashimNo ratings yet

- HPS TheoryDocument2 pagesHPS TheorySiva SankariNo ratings yet

- Dba1607 Legal Aspects of Business PDFDocument404 pagesDba1607 Legal Aspects of Business PDFsantha3e100% (12)

- Buying and Selling Vocab-1Document3 pagesBuying and Selling Vocab-1Nazwa AzliaNo ratings yet

- Bcom 1-6 SyllabusDocument60 pagesBcom 1-6 Syllabusapi-282343438No ratings yet

- Material For PracticeDocument8 pagesMaterial For PracticeJayaKhemani100% (1)

- Financial Services M.com NotesDocument31 pagesFinancial Services M.com NotesFarhan Damudi75% (8)

- Hire Purchase PDFDocument12 pagesHire Purchase PDFliamNo ratings yet

- Hire PurchaseDocument19 pagesHire PurchaseFaris Hanis100% (1)

- English Commercial Law Module Handbook-Updated 20120612 181831Document46 pagesEnglish Commercial Law Module Handbook-Updated 20120612 181831Roda May DiñoNo ratings yet

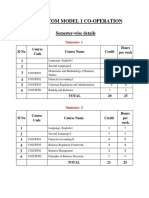

- B Com Model 1 Co OperationDocument37 pagesB Com Model 1 Co OperationHvffNo ratings yet

- REPUBLIC ACT No 6552Document6 pagesREPUBLIC ACT No 6552GraceNo ratings yet

- Financial Accounting (1st Year)Document18 pagesFinancial Accounting (1st Year)RohitNo ratings yet

- Assigment Business LawDocument12 pagesAssigment Business Lawapisj5100% (1)

- Verification of Assets and LiabilitiesDocument62 pagesVerification of Assets and Liabilitiesanon_672065362No ratings yet

- A Critical Appraisal of Al-Ijarah Thumma Al-Bay' (AITAB) Operation: Issues and ProspectsDocument16 pagesA Critical Appraisal of Al-Ijarah Thumma Al-Bay' (AITAB) Operation: Issues and ProspectsNur ShahiraNo ratings yet

- General Banking Activities of Social Islami Bank Limited With Special Reference To Accounts SectionDocument27 pagesGeneral Banking Activities of Social Islami Bank Limited With Special Reference To Accounts Sectioncatseye2050No ratings yet

- English Commercial Law Module Handbook-Updated 20120612 181831Document45 pagesEnglish Commercial Law Module Handbook-Updated 20120612 181831Godslove Minta100% (1)

- SY BCom NewDocument42 pagesSY BCom NewAamir KhanNo ratings yet

- Aqsat FAQs enDocument3 pagesAqsat FAQs enRockroll AsimNo ratings yet

- Module-3 IFSS-NoteDocument29 pagesModule-3 IFSS-NoteAbhisekNo ratings yet

- E Catalogue 86681ff1Document21 pagesE Catalogue 86681ff1Tariq SalimNo ratings yet

- Sales of Goods Act-1930Document22 pagesSales of Goods Act-1930Karan Veer Singh67% (3)

- Sale of Goods Act 1930Document47 pagesSale of Goods Act 1930suhasiniNo ratings yet

- Ownership Transfer FormDocument2 pagesOwnership Transfer FormSambit DasNo ratings yet

- Hire Purchase AgreementDocument16 pagesHire Purchase AgreementKweku JnrNo ratings yet