You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Business Enivironment and LawDocument321 pagesBusiness Enivironment and Lawajit4allNo ratings yet

- Etrade Bank Deposit Slip PDFDocument2 pagesEtrade Bank Deposit Slip PDFAdamNo ratings yet

- Acc 117 Group Project 1 (Group 3)Document17 pagesAcc 117 Group Project 1 (Group 3)NORAMYZA AKMA JAMALUDINNo ratings yet

- AccountingDocument88 pagesAccountingFranky100% (3)

- Total Quality ManagementDocument40 pagesTotal Quality Managementyashika swamiNo ratings yet

- Human Resource Management Ch12Document42 pagesHuman Resource Management Ch12atoydequitNo ratings yet

- III SEM - Business ManagementDocument25 pagesIII SEM - Business Managementyashika swamiNo ratings yet

- Devedet TheoryDocument14 pagesDevedet Theoryyashika swamiNo ratings yet

- What Is Total Quality ManagementDocument12 pagesWhat Is Total Quality Managementyashika swamiNo ratings yet

- EvaluationDocument15 pagesEvaluationyashika swamiNo ratings yet

- HRMDocument13 pagesHRMzaraNo ratings yet

- Capital Budge 2Document26 pagesCapital Budge 2yashika swamiNo ratings yet

- Management Control Systems PDFDocument17 pagesManagement Control Systems PDFyashika swamiNo ratings yet

- Total Quality ManagementDocument40 pagesTotal Quality Managementyashika swamiNo ratings yet

- Advertising ResearchDocument8 pagesAdvertising ResearchPiNo ratings yet

- Advertising ResearchDocument8 pagesAdvertising ResearchPiNo ratings yet

- Managerial SkillsDocument2 pagesManagerial Skillsyashika swamiNo ratings yet

- Quality of Work LifeDocument8 pagesQuality of Work Lifeyashika swamiNo ratings yet

- Management Control Systems PDFDocument17 pagesManagement Control Systems PDFyashika swamiNo ratings yet

- Quality of Work LifeDocument8 pagesQuality of Work Lifeyashika swamiNo ratings yet

- Child Labor From Sadaqat ALiDocument9 pagesChild Labor From Sadaqat ALiSadaqat AliNo ratings yet

- Child Labor From Sadaqat ALiDocument9 pagesChild Labor From Sadaqat ALiSadaqat AliNo ratings yet

- Corporate GoveranceDocument23 pagesCorporate Goveranceyashika swamiNo ratings yet

- Flexible Work Arrangements and Employee Retention in IT SectorDocument8 pagesFlexible Work Arrangements and Employee Retention in IT Sectoryashika swamiNo ratings yet

- QuestionnaireDocument4 pagesQuestionnaireyashika swamiNo ratings yet

- Quality of Work Life in The UniversitiesDocument15 pagesQuality of Work Life in The Universitiesyashika swamiNo ratings yet

- Reference: 11. Dessler, G. (1981) - Personnel Management. Reston Publishing Company: RestonDocument27 pagesReference: 11. Dessler, G. (1981) - Personnel Management. Reston Publishing Company: Restonyashika swamiNo ratings yet

- Offer Letter TemplateDocument6 pagesOffer Letter Templateyashika swamiNo ratings yet

- Quality of Work Life With Special Reference To Academic SectorDocument4 pagesQuality of Work Life With Special Reference To Academic Sectoryashika swamiNo ratings yet

- Vol. 4 Issue 1,2 Jan-June 13 PDFDocument1 pageVol. 4 Issue 1,2 Jan-June 13 PDFyashika swamiNo ratings yet

- Quality of Work Life With Special Reference To Academic SectorDocument4 pagesQuality of Work Life With Special Reference To Academic Sectoryashika swamiNo ratings yet

- Training and Development in Indian Banking SectorDocument7 pagesTraining and Development in Indian Banking Sectoryashika swamiNo ratings yet

- Questionnire For LeadDocument3 pagesQuestionnire For Leadyashika swamiNo ratings yet

- Tvl-Computer Systems Servicing-Grade 12: Let Us DiscoverDocument6 pagesTvl-Computer Systems Servicing-Grade 12: Let Us DiscoverDan Gela Mæ MaYoNo ratings yet

- Operations Management Slide 1st ChapDocument34 pagesOperations Management Slide 1st ChapMehedi HassanNo ratings yet

- Urban MobilityDocument2 pagesUrban MobilityHafiey EyzaNo ratings yet

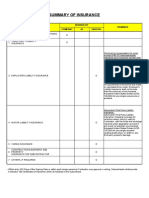

- Summary of Insurance: RDMP Balikpapan Project Description Insured by Remarks Company JO SubconDocument1 pageSummary of Insurance: RDMP Balikpapan Project Description Insured by Remarks Company JO SubconAsywida FahmiNo ratings yet

- Phone CallsDocument4 pagesPhone CallsDaiboun Sahel ImeneNo ratings yet

- ICAP Exemptions For Other QualificationsDocument2 pagesICAP Exemptions For Other QualificationsAtiq RehmanNo ratings yet

- Website Returns Form V2Document2 pagesWebsite Returns Form V2masturbate2308No ratings yet

- Customer App FormDocument2 pagesCustomer App FormELMON RENTASIDANo ratings yet

- Quarantine Facilities Available As Below (Rate Inclusive of Taxes and Three Meals)Document4 pagesQuarantine Facilities Available As Below (Rate Inclusive of Taxes and Three Meals)Revankar B R ShetNo ratings yet

- Request For Modification Permit-New - GuidelineDocument9 pagesRequest For Modification Permit-New - GuidelineGregorio PossagnoNo ratings yet

- 300-420 ENSLD Designing Cisco EnterpriseDocument3 pages300-420 ENSLD Designing Cisco Enterprisehector_ninoskaNo ratings yet

- Chapter - 1 An Introduction To Indian Banking SystemDocument27 pagesChapter - 1 An Introduction To Indian Banking Systemprasad pawleNo ratings yet

- SDX 6000 SeriesDocument6 pagesSDX 6000 SeriesHakob DadekhyanNo ratings yet

- Explanation of BenefitsDocument1 pageExplanation of Benefitssamy gomaaNo ratings yet

- CSEC Tourism QuestionDocument2 pagesCSEC Tourism QuestionJohn-Paul Mollineaux0% (1)

- Draft Consolidated ReportDocument41 pagesDraft Consolidated Reportoishi AcharyaNo ratings yet

- Issue 26Document128 pagesIssue 26SnehalPoteNo ratings yet

- Job-Specification - House Officer PDFDocument2 pagesJob-Specification - House Officer PDFIndika2323No ratings yet

- Telit ML865C1 Product BriefDocument2 pagesTelit ML865C1 Product BriefAbhishek TiwariNo ratings yet

- Dentists Email ListDocument8 pagesDentists Email Listlawra nickNo ratings yet

- Session 1 - Tourism - A Sunrise SectorDocument20 pagesSession 1 - Tourism - A Sunrise SectorNiyati Bhat JathalNo ratings yet

- Supply Chain ManagementDocument3 pagesSupply Chain Managementnst100% (1)

- Prepayment of Your Personal Loan Account:XXXXXXXXXXXX4785Document2 pagesPrepayment of Your Personal Loan Account:XXXXXXXXXXXX4785Daniel GnanaselvamNo ratings yet

- Chapter 1Document38 pagesChapter 1saraNo ratings yet

- Business Accounting and Taxation BrochureDocument4 pagesBusiness Accounting and Taxation BrochureRudrin DasNo ratings yet

- Motor Vehicles Department, Government of Maharashtra: Application Reference DetailsDocument3 pagesMotor Vehicles Department, Government of Maharashtra: Application Reference DetailsAshutosh BhosaleNo ratings yet

- Bank Statement Template 2 - TemplateLabDocument1 pageBank Statement Template 2 - TemplateLabViktoria DenisenkoNo ratings yet