Professional Documents

Culture Documents

Internship Report

Uploaded by

Disha GanatraCopyright

Available Formats

Share this document

Did you find this document useful?

Is this content inappropriate?

Report this DocumentCopyright:

Available Formats

Internship Report

Uploaded by

Disha GanatraCopyright:

Available Formats

INTERNSHIP PROJECT

REPORT

DISHA GANATRA

113712

MSc. FINANCE

COMPANY DETAILS

JAKHOTIA POLYFIBRE PVT. LTD.

3-6-323, BASHEERBAGH,

HYDERABAD, 500 029 (A.P.)

040 23441962

2

TABLE OF CONTENTS

PAGE No.

Acknowledgement 2

Executive Summary 3

Objectives 4

PART A

+ Industry Overview 5-9

+ Company Profile 10-26

Organization's Aim, Vision, Mission & Goal 10

Statutory Approvals 11

Organistational Structure 11

Human Resource Management Practices 12

Corporate Daily Policy 12

Environment Concern 12

Technical Parameters 13

Research & Development 13

Quality Assurance 14

Customization 15

Client Satisfaction 16

Raw Material Requirement 16

Their Manufacturing Facilities 16

Factory Location 17

Summary Of Steps Or Processes That Takes Place In The Factory 18-22

Summary Of The Manufacturing Process 22-24

Inventory Management 25-26

PART B

Internship Work Report and Topics Covered There In

+ Auditing 27-28

+ Cost Sheet 29-32

+ Financial Statement Analysis 33-39

+ SWOT Analysis 40

+ Weekly Log Report 41-42

Conclusion 43

Annexure 44

Bibliography 45

3

ACKNOWLEDGEMENT

I owe a great many thanks and gratitude to a great many people who helped and supported me

during my Internship.

The success of my internship depends largely on the encouragement and guidelines of many

others. I take this opportunity to express my gratitude and to extend my sincere thanks to all the

people who have been instrumental in the successful completion of my Internship and this report.

I express my thanks to the Principal of my college, St. Francis College for Women, Sister

Alphonsa Vattoly and our Course Co-ordinator Dr. Deepa James for giving me this opportunity

and for extending their support.

I would like to express my gratefulness to Prof. Dr. Vanishree T, who acted as a mentor

throughout my project for providing me valuable information and guidance.

My deep sense of gratitude to Mr. Anup Jakhotia (Director), Jakhotia Ployfibre Pvt. Ltd. for

giving me this opportunity of Internship, which has been a great learning experience. I would

also like to thank Mr. K. Sasidhar (C.E.O.), who has been very helpful in guiding and helping me

in getting the required information related to my internship.

I am especially thankful to Mr. Haridas Mundada, whose expertise and knowledge has helped me

learn and understand many concepts and there applicability in the Practical World.

And I would also like to take this opportunity to thank and show my appreciation to my dear

friend Ms. Needhi Bhutada, with whom I have done my internship, it would not have been the

same experience without her.

Lastly and most importantly, I also extend my heartfelt thanks to the Almighty God, my family

and well wishers. I would not have been able to do anything without them and their wishes.

4

EXECUTIVE SUMMARY

At Jakhotia Polyfibre Pvt. Ltd. I spent good time in learning and was rewarded for my best

efforts, learnt to deal with different situations, had experience of organizations working

environment.

Confidence, consistency, hard work, teamwork, seeking success out of dark, innovation,

creativity, organizational survival are the key learnings out of my job And I would like to say

that it will be one of my best skill that would remain with me and help me in the coming life

which offer many challenges.

The areas covered during my internship were wide like

I was taken to visit the factory, where I observed the process carried on in the factory and also

the manufacturing process.

I was given practical work like recording of vouchers in Tally. Later, I got to know the various

policies and practices of the company like their Human Resource Management practices, their

Aims, their vision and mission statements, etc.

After getting to know the company, I even got to know about the auditing aspect and practices.

As there was an Internal audit going on in the company, I assisted the Auditor in the Auditing

Process. I had the opportunity to learn a lot of things about Auditing and Taxation.

We also ventured into the topic of Cost Sheet. As its a Manufacturing Company cost sheet is

given a lot of importance. So the Manager gave a brief about the cost sheet and various cost

elements comprising in the Companys cost sheet.

Later on I was provided with the Financial Statements i.e. the Balance Sheet and Profit & Loss

Statement. With the help of these I used various Financial Statement Analysis Tools like

Comparative Statement Analysis, Common size Statement Analysis, Ratio Analysis, etc. to

analyse the financial statements.

I would like to highlight this, that my experience with the company was very memorable and full

of learning, where I found a lot of positive changes in my attitude, learning and behavior.

5

OBJECTIVES

To develop skills in the application of theory to practical work situations.

To develop self-confidence, assertiveness, and basic work habits.

To improve my communication skills, especially when dealing with people I do not

know.

To improve my ability to talk with others on a professional level.

To improve my research skills to be more effective and efficient in obtaining information.

To understand the workplace, operating procedures, the company and its products, how

the firm competes, and other organizational concepts.

To know what it is like to work in a professional environment.

To gain experience and insight in the work field during the internship.

6

PART A

INDUSTRY OVERVIEW

PLASTIC INDUSTRY PROFILE

Plastics have revolutionized our lives, creeping into every nook and corner of our homes and

offices. However, Indias per capita consumption of plastics is still 6 kg compared to 25 kg in

developed countries. Consumer plastics mainly comprise polymers such as polypropylene, high

and low density polyethylene, and vinyl chloride. Broadly plastics can be classified into two

types namely Thermosetting and Thermoplastic. The type of plastics includes HDPE, LDPE,

PVC, PP, PS, PETE and vinyl plastics, to name a few.

The plastics industry is highly fragmented. There are about 22,000 plastic processing units, of

which three-fourth are in the small-scale sector, which also accounts for a quarter of the total

polymer consumption. About 30 per cent of the total polymer consumption accounts for recycled

plastic. Plastics have a high volume-to-weight ratio, which makes their collection and transport a

major cost factor.

The Indian plastics industry has been growing at a phenomenal rate of 15 per cent over the years.

Thus its potential is being utilized properly. The boost in the plastics industry is due to the rapid

growth of segments like electronics, packaging, healthcare, consumer durables and

telecommunication sectors. Annually around six million tones of plastic is produced in the

country, with the plastic packaging sector growing fastest.

Reliance Industries Ltd., Gas Authority of India and petrochemicals are major producers of

polymers in India. RIL, Asias largest manufacturer of polypropylene with a combined capacity

of over one million tones, holds 70 per cent market share.

India will be the third largest plastics consumer after the US and China by 2010 at over 12

million. Plastic goods consumption is expected to double in the next three years. Experts have

predicted that Indias market for finished plastic goods will reach $300 billion by 2012, while

exports are expected to reach a level of $200 billion in the same period. India ranks highest in

recycling of plastics with 60 per cent of plastic recycled compared with a world average of 20

per cent. Experts have estimated that the basic demand for plastic would be boosted over the next

years by the housing, automobile and retail sectors.

Trends in Bulk Packaging:

PP Woven Sacks, Jute, Paper bags/ box are most widely used packaging systems for Bulk

Commodities. Cement, fertilizer and most of the chemicals are already packed woven sacks

while Food grains and sugar use both woven sacks and jute bags. Plastics are the material of

choice because of inherent advantages of functional performance and cost benefits. Relative

merits with respect to functional requirement for bulk packaging using these three prime

packaging materials are summarized in Table-1

7

Functional Requirement for Bulk Packaging (Table-1)

Parameter Jute Paper PP Woven Sacks

Seepage Relatively High Low Low

Moisture Prevention Nil Nil Excellent

Contamination /

Infestation

Very High Nil Low to Moderate

Organoleptic deterioration Very High Moderate Minimum

Aesthetics Poor Good Good

Availability Seasonal Limited Abundant and Easy

Cost High High Low

Seam Strength Strong Strong Low

Operational Convenience Good but Abrasive Good Good

Stack Stability Good Good Good

Drop Test Performance Fair Poor Very Good

Microbial attack Very High High Nil

Air borne pollution Very High None None

Biodegradability Yes Yes No

Energy Recovery Low Low High

Reusability Good Nil Good

8

Opportunities in Bulk Packaging - Polypropylene Woven Sacks the Ideal Choice:

Packaging fulfils the diverse role from protecting products, preventing spoilage, contamination,

extending shelf life, ensuring safe storage thereby helping to make them readily available to

consumers.

India is one of the largest producers of commodities like foodgrains, sugar, fruits, vegetables and

tea. Due to varied crop pattern, localized production of commodities, safe and hygienic storage,

transportation and distribution and protection against wastage, hence packaging is of utmost

importance. Huge losses have been observed in agriculture produce in India. Wastage varies from

5 to 35% depending on nature of crops.

Majority of wastage takes place in each of the above steps viz. storage, transportation and at retail

market due to improper packaging. Bulk Packaging provides a solution for commodities weighing

10 to 50 Kg during handling, storage and transportation.

The present paper describes trends in Bulk Packaging for various commodities, suitability of

Polypropylene (PP) Woven Sacks for packaging of foodgrains, sugar, tea, similarly for packaging

and transport of vegetables and other horticulture produce PP leno bag is an effective packaging

system. With changing packaging need, optimization of packaging role of Flexible Intermediate

Bulk Container (FIBC) and its future has been highlighted as trend. PP Woven sacks are

worldwide material of choice for bulk packaging of edible commodities for domestic use and

exports.

Polypropylene : Industry

+ Polypropylene (PP) is the third largest segment in the polymer group

+ PP can be manufactured by three different processes - solution polymerisation, slurry phase

polymerisation and gas phase process.

+ Polypropylene is widely produced by the gas phase process of propylene

+ PP is available as homopolymer or co-polymers of propylene and ethylene

+ PP fast substituting other polymers due to properties

o High strength to weight ratio

o Lightest of all the thermoplastic polymers

o High melting point

o Good processibility and gas barrier

o Low permeability to water and unaffected by bacteria

o Good directional stability

+ Market monopolised by IPCL till 1997-98

9

Production of PP Woven Sacks:

Polypropylene (PP) is used as the basic raw material and is fed to the hopper of extruder and

melted to pass through a T- die in film form which is then slit into tapes, which are then oriented

by stretching and wound in cheese winders. Tapes are then fed into circular / flat looms and

woven into tubular or flat fabric respectively. These fabrics can then be laminated based on

functional need of the packaging. Finally fabrics are cut into pieces as per bag specification with

stitching in bottom and top as per requirement followed by printing.

Pp Woven Bags (for Cement Packing)

PP BAGS FOR CEMENT PP/HDPE oriented sacks are becoming popular through out the world.

This is because they are chemically inert & are water repellent & lighter in weight. They are free

and possess sufficient strength and can easily be handled. These bags are expected to substitute

jute and craft paper bags in several areas. These bags are used in packaging of fertilizers, cement,

pesticides, chemical, oil seed, food grains, dry materials etc. PP bags enjoy a good market in

India and will continue to do so in the coming years. Plastic woven sacks are rapidly replacing

jute bags because they have often various advantages over the conventional jut fabrics as

packaging materials. They are also stronger and can withstand much higher impact loads. It has

high demand everywhere. So, new entrepreneurs can venture into this field.

Profile PP woven sacks laminated with PP liner have wider applications. PP woven sacks are

much stronger & can withstand much higher impact loads because of PP strips elongation at

break is about 15 to 25% as compared to 30% of Jute. These sacks are much cleaner & resist

fungal attack. PP Woven Sacks can be unlaminated, Laminated and along with PE liners. The

size range for bags made from tubular fabric is from minimum 24 inches (60 cm.) upto 61 inches

(155 cm). Woven Sacks are the best and the most cost effective packaging solution for Industries

like Cement, fertilizer, sugar, chemicals, food grains etc. off late Woven fabric, which is the first

stage of Woven sacks, is a preferred medium for bale wrapping and rain protection in the form of

Tarpaulin.

Salient Features:

+ Flexible and high strength

+ Double side print

+ Water & dust proof design

+ Heat/Wave Cut & hemmed top

+ Flat or anti-slip weaving

Applications:

PP woven bags and PP woven sacks with liners are specially designed for the packaging of

pulverous & force flowing materials, which include the following:

+ Food Products: Flour, Corn, Grain, Sugar, Salt, Animal Feed

+ Chemicals & Fertilizers: Carbon, Caustic Soda, Potash, Phosphates

10

+ Petro chemicals: Polymers, Granules, PVC Compound, Master Batches

+ Minerals: Cement, Calcium Carbonate, Lime, Sand

Advantages:

Woven bags and sacks of HDPE/PP offer several advantages over other industrial packaging

material. Some of the advantages are:

+ Moisture Proof: HDPE/PP Bags are inherently moisture repellent

+ Light Weight: HDPE/PP Bags being light weight, offers easy and cheap transportation.

+ Printing: Bright 2/3/4 Colour printing offer aggressive marketing prospects

+ Stack ability: No problems in stacking. Can be gusseted to further improve stacking

+ Strength: High Tensile strength and long life.

+ Economical: Highly economical compared to other alternative packing material

+ Seepage: No Seepages specially in paper lined bags

Plastic woven sacks are rapidly replacing jute bags because they have often various advantages

over the conventional jute fabrics as packaging materials. They have excellent chemical

resistance; they are light in weight and more suitable for packing of various chemicals in the

form of granules and powder. They are also: stronger and can withstand much higher impact

loads. Their elongation at break is 15 to 25 per cent compared to 3 per cent for jute; they are

much cleaner, both in use and production and can be used to handle food products as they are

resistant to fungal attack. Because of such superior properties of plastic woven bags, it has high

demand everywhere. Cement industry is increasing day by day.

11

COMPANY PROFILE

ABOUT THE COMPANY

Jakhotia Plastics Private Limited is one of the leading Polypropylene (PP) bag manufacturers in

India. They are manufacturing polypropylene bags since 1994; owing to their experience they

can offer customers the best quality products. There offer comprises of various types of bags and

sacks. They make polypropylene woven bags and sacks according to customer's specifications,

concerning dimensions and weights. PP Woven bags are the traditional bags in packaging

industry due to their wide variety of usage, flexibility and strength. Woven polypropylene bags

are specializing in packing and transporting bulk commodities. Due to strength, flexibility,

durability and lower cost, woven polypropylene bags are most popular products in industrial

package, which are widely used in packing cement, grain, feeds, fertilizer, seeds, powders, sugar,

salt, powder, chemical in granulated form. PP Woven bags are made according to customer's

preferred specifications as to mesh, denier, GSM, color, and sizes that vary from 25 to 80 cm.

widths or depending on the desired capacity.

Jakhotia Plastics are manufacturer of Polypropylene Circular Woven Sacks, mostly catering to

the needs of Cement Industry. And their products are basically used for packaging of Cement.

ORGANIZATION'S AIM, VISION, MISSION & GOAL

AIM / MISSION

We aim to provide the best packaging solutions with customer satisfaction, quality

assurance and a congenial working environment.

We strive to offer the finest quality services, timely delivery and competitive prices to all

our client.

We assure our clients the best products within a stipulated time frame

GOAL

To provide our customers with complete packaging solutions which can help them enhance their

business opportunities.

VISION STATEMENT

To supply packaging material all over India.

MISSION STATEMENT

To capture 80% of market share in India for cement packaging material.

CORE COMPETENCY OF THE COMPANY

Production of finest Quality Woven Sacks.

12

STATUTORY APPROVALS

+ Income Tax Registration: PAN No: AAACJ 5070 A

+ TIN No.: 28580199316

+ ECC No.: AAACJ 5070 AXM 002

+ CIN No.: U25209 AP 1992 PTC 014875

ORGANISTATIONAL STRUCTURE

MANAGING DIRECTOR

(OM PRAKASH JAKHOTIA)

DIRECTOR

(ANUP JAKHOTIA)

JAKOTIA)

DIRECTOR

(ARUN JAKHOTIA)

JAKOTIA)

MANUFACTURING

MANAGER

(REDDY)

ASSISTANT

MANAGER

ASSISTANT

MANAGER

ASSISTANT

MANAGER

ACCOUNTS

MANAGER

(DUTTA)

COMMERICAL

MANAGER

(SASIDHAR)

PURCHASE

MANAGER

(GRK RAJU)

ASSISTANT

MANAGER

13

HUMAN RESOURCE MANAGEMENT PRACTICES

The company does not follow any pre-defined rules or procedure for HRM.

For the purpose of finding out the details about the HRM practices carried out in the company,

we prepared a questionnaire and with the help of the manager learnt about the companys HRM

practices.

Refer ANNEXURE to find the questionnaire and the details relating to the HRM practices of the

Company.

CORPORATE DAILY POLICY

Jakhotia Plastic Pvt. Ltd.'s Management firmly believes that safety of its employees and all the

stakeholders associated with their project sites and manufacturing facilities is of utmost

importance. Safety is an essential and integral part of all their work activities which includes

planning, design, procurement, fabrication, construction, installation and commissioning of

facilities, products, manufacturing processes and services. They believe that incidents or

accidents and risk to health are preventable through the active involvement of all the stake

holders, thereby creating a safe and accident free work place. With regard to safety objectives,

the company will:-

+ Comply with the requirements of all relevant statutory, regulatory and other provisions.

+ Create and promote safety awareness to protect all stake holders from fore seeable work

hazards and risks through campaigns and training programmes among employees, business

associates and clients.

+ Provide appropriate level of training and supports to management and employees to ensure

that they are able to fulfill safety responsibilities.

+ Work with major suppliers, business associates and customers to facilitate their safety

performance improvement and also make it obligatory for them to follow the project site

safety rules, procedures, systems and safe practices.

Ensure that appropriate resources are available to fully implement the Safety Policy and

continuously review the policy's relevance with respect to legal and business development.

ENVIRONMENT CONCERN

With a conscious mind, they undertake Eco-friendly manufacturing processes and make sure that

less effluent and smoke are released. They take the following three concerns seriously that are

defined by some of the well-known regulatory bodies.

Reduction in hazardous environmental release

Recycling of waste products

14

Use of environmentally preferable products

For this, they source some of the latest and high performing machines for their unit. Moreover,

the material for fabrication is quality tested and is bio-degradable, which ensures no hazards to

the environment. The range of PP products manufactured by them are recyclable and do not emit

obnoxious fumes, when burned.

TECHNICAL PARAMETERS

Weight As per Required size

Width 30" to 155"

Denier 350 to 1200

Size 12 TO 90

GSM 40 GSM TO 120 GSM

Length As per Requirement

Colors Any Color

Imprint All

Packing As per Party Requirement

Bag opening As per Party Requirement

PE lining Yes

Laminated/Coated Yes

Perforated Yes

Mesh 8 x 8 TO 12 x 12

UV Stabilization As per customer requirement

The company endeavors to serve the industry with optimum quality latest products available in

the market at the most competitive prices. It is the quality of the products and the attitude of our

company towards its customers that has helped it in scaling great heights.

RESEARCH & DEVELOPMENT

At Jakhotia Plastics Pvt Ltd., they continuously strive to meet the challenging requirements of

the customers. Thus they keep a special focus on Research & Development to equip the

customers with latest products at the most competitive prices.

15

The following has helped in developing new products & colour masterbatches for the customers

in the shortest time at the most competitive prices:

+ To properly understand the needs of the customer.

+ Close interaction with the suppliers to know what is new in the market.

+ Maintaining a database of all trials at their end & customers end.

+ Colour swatches of all masterbatches in form of granules, film & molded chips.

+ Electronic database of standard pigments & end product.

+ Latest equipments such as Injection molding machines, two roll mills, hydraulic press,

spectrophotometer, imported MFI machines, imported filter pressure machines and many

more.

+ Small capacity production machines especially dedicated for R&D work.

QUALITY ASSURANCE

For Jakhotia Group of companies "Quality" is not an act but it is a habit. Quality Assurance is in

hands of most expert & experienced people in which top management itself is included.

They strictly follow "Quality Assurance System" at different level of Manufacturing Process...

+ Raw material Testing--Certified by major manufactures like Reliance, IPCL, Haldia, GAIL,

IOC, etc.

+ Tape Yarn--Width of yarn--Denier of yarn--Strength and elongation

+ Fabric--Size of Fabric, Mesh, Strength and elongation, Weight of Fabric in GSM

+ Cutting--Weaving Defects, Size of Cutting

+ Stitching--Seam Strength/Strength of Bag, Weight of Bag, Mass of Sack, Cleaning and

printing matter

+ Packaging--Counting and Proper Bailing

The Groups well-trained and experienced staff and associates ensures that all the products are

made from the finest material and adopts stringent quality control measures through out the

production process. Quality control is applied at each and every stage of manufacture and

storage, leading to the delivery of top quality material. An important part of our quality control is

minimal wastage of the raw material. Due to minimum wastage of less than 5% (from tape to

bag) gives an opportunity to keep the price under control.

Jakhotia Group has a complete in-house manufacturing & testing facility that enables it to

16

produce totally flawless and tough products.

What helps them to give an Edge over the competition?

Their experience of 18 years has enabled them to register their capabilities among their

competitors owing to the following factors:

+ Ethical business practices

+ Quality range of PP products

+ Specialize in offering printing services

+ Sound manufacturing facilities

+ Dexterous team of professionals

+ Custom designing

+ Excellent customer service

+ Wide marketing and distribution network

+ Timely delivery

+ Complete client satisfaction

CUSTOMIZATION

Serving clients in the best possible way is the only factor that boosts the growth of an

organization and promotes cordial relationships with them. This can be attained by providing the

customer with a product or a service of his/her choice and requirement. They accomplish the

arduous task of fulfilling the client individual needs by offering them the customization facility.

The facility assures that the clients receive range of PP products as per their specifications and

preferences.

The customization of PP Woven Bags / Sacks is done on following parameters:

Weave

Material

Draw string or zipper

PE lining

Printing & Logo on both sides

Lamination (Option for un-laminated

also available)

Length

Capacity

Weight

Gauge

Stitch and sew

Seal

Gusset

Handle

Bottom

Grade

They also offer customization of woven fabrics on the following parameters:

Single or double fold

Laminated / un-laminated

Weave & mesh

Print

Colors

Length

Weight

Gauge

17

CLIENT SATISFACTION

They are a company that strives to match the expectations of our clients in all possible ways that

help us in the betterment of our concern. Consequently, we provide them with quality PP bags.

These products are prepared using the high-grade material to assure that our clients receive only

the best and excellent range of products. Owing to the transparency in our business proceedings,

we have been able to garner maximum client satisfaction and cater to the needs of retailers, local

authorities, wholesalers, schools and big & small industries. With this, we also make a point to

supply our products in the set time frame and provide them with hassle-free transactions.

In addition to this, we attain maximum client satisfaction by offering our clients our range of

products as per the specifications and also offer facility of customized packaging to them.

- Jakhotia Group of Companies - Major clients are ORIENT CEMENT and B.K. BIRLA

GROUP

- Jakhotia Polyfibre Pvt. Ltd. - Major clients are VASAVADATTA CEMENT and

ULTRATECH CEMENT

RAW MATERIAL REQUIREMENT

The raw materials required are:

1. The polypropylene granules that are made into the tape yarn and then woven into the sacks

2. Colors or dyes for giving the polypropylene sacks the required colors.

The main factors guiding the source of raw material are:

o Quality

o Availability

o Cost

Quality plays a vital role in deciding the choice of raw material supplier.

The cost of the raw material is almost same but it is still a major guiding force behind choice of

the raw material.

Availability forms a major guiding force behind the buying decision as cost and quality being

almost same.

- Jakhotia Group of Companies major Supplies of Raw Materials are from the

RELIANCE INDUSTRY

THEIR MANUFACTURING FACILITIES

Their commitment towards efficiency is visible in the production process they follow and in the

final product supplied. Stretched across a wide plot area, their manufacturing unit assists them in

manufacturing their range of polypropylene bags and PP/HDPE Woven Fabrics as per the

specifications of the clients. In order to attain hassle free production, they have installed the unit

18

with all the latest machines and tools such as:

Extruders (PP / HDPE Stretching Lines)

Cutting and stitching machines

Circular weaving machines

Woven bag sewing machines

Hydraulic bailing presses for HDPE/PP bags

These machines help them in achieving a notable production capacity and fulfill the bulk

requirements of their clients within the stipulated time frame. In order to keep the machines in

proper working condition, these are maintained and upgraded timely.

Their Printing Facilities

Apart from the above motioned machines, they also have special printing machines that enable

them to print these bags, fabrics etc. These prints contain the logos of the clients company or

establishment and make use of the bags for packaging their products. They make use of

advanced printing facilities like six-color printing, offset printing, hot stamping, gravure and

other options such as tissue inserts, hang tags and bag labels.

Their Team

The core strength of the organization is the team of assiduous professionals, who help them in

the production of flawless range of polypropylene bags. the team holds immense expertise in

manufacturing of a range of products as per the industry requirements and continuously

upgrading it to stay at par with international standard. The professionals are well aware of their

responsibility and are instrumental in executing their respective tasks with perfection.

FACTORY LOCATION

1. JAKHOTIA PLASTICS PVT LTD Jeedimatla, A.P.

2. JAKHOTIA PLASTICS PVT LTD Goa

3. JAKHOTIA POLYMERS PVT LTD Hyderabad, A.P.

4. JAKHOTIA POLYFIBRE PVT LTD Sedam, Karnataka

5. JAKHOTIA POLYSACKS PVT LTD Rangampally, A.P.

6. RAGHURAM SYNTHETICS PVT LTD Suglampally, A.P.

Other Company specific information is present in ANNEXURE.

19

+ SUMMARY OF STEPS OR PROCESSES THAT TAKES PLACE IN THE FACTORY

STEP 1: Vendor Quotation

Procuring the Vendor Quotation and asking for Proforma invoice. If satisfied issue a Purchase

orders. According to it the raw materials are procured and ordered.

STEP 2: Purchase Order

Purchase Order Types

Purchasing provides the following purchase order types: Standard Purchase Order, Planned

Purchase Order, Blanket Purchase Agreement, and Contract Purchase Agreement. You can use

the Document Name field in the Document Types window to change the names of these

documents. For example, if you enter Regular Purchase Order in the Document Name field for

the Standard Purchase Order type, your choices in the Type field in the Purchase Orders window

will be Regular Purchase Order, Planned Purchase Order, Blanket Purchase Agreement, and

Contract Purchase Agreement.

Standard Purchase Orders

You generally create standard purchase orders for one-time purchase of various items.

You create standard purchase orders when you know the details of the goods or services

you require, estimated costs, quantities, delivery schedules, and accounting distributions.

If you use encumbrance accounting, the purchase order may be encumbered since the

required information is known.

Blanket Purchase Agreements

You create blanket purchase agreements when you know the detail of the goods or

services you plan to buy from a specific supplier in a period, but you do not yet know the

detail of your delivery schedules. You can use blanket purchase agreements to specify

negotiated prices for your items before actually purchasing them.

Blanket Releases

You can issue a blanket release against a blanket purchase agreement to place the actual

order (as long as the release is within the blanket agreement affectivity dates). If you use

encumbrance accounting, you can encumber each release.

Contract Purchase Agreements

You create contract purchase agreements with your suppliers to agree on specific terms

and conditions without indicating the goods and services that you will be purchasing.

You can later issue standard purchase orders referencing your contracts, and you can

encumber these purchase orders if you use encumbrance accounting.

20

Planned Purchase Orders

A planned purchase order is a long-term agreement committing to buy items or services

from a single source. You must specify tentative delivery schedules and all details for

goods or services that you want to buy, including charge account, quantities, and

estimated cost.

Scheduled Releases

You can issue scheduled releases against a planned purchase order to place the actual

orders. If you use encumbrance accounting, you can use the planned purchase order to

reserve funds for long term agreements. You can also change the accounting distributions

on each release and the system will reverse the encumbrance for the planned purchase

order and create a new encumbrance for the release.

Purchase Order Types Summary

Standard

Purchase

Order

Planned

Purchase

Order

Blanket

Purchase

Agreement

Contract

Purchase

Agreement

Terms and

Conditions

Known

Yes Yes Yes Yes

Goods or Services

Known

Yes Yes Yes No

Pricing Known Yes Yes Maybe No

Quantity Known Yes Yes No No

Account

Distributions

Known

Yes Yes No No

Delivery Schedule

Known

Yes Maybe No No

Can Be

Encumbered

Yes Yes No No

Can Encumber

Releases

N/A Yes Yes N/A

21

JAKOTIA PRIVATE LIMITED FOLLOWS BLANKET PURCHASE ORDER. THIS IS

THE SCHEDULE TO BE PREPAID BEFORE 31

ST

MAY.

STEP 3: Issuing of a Purchase Invoice

It will have all the specific details like Quantity, Description, Time, etc.

STEP 4: Dispatching the Material

The materials are then dispatched to the respective Plants and Machines. Gate entry of

transaction is made and the Bill is stamped.

Match the Purchase order and the Invoice.

STEP 5: Quality Check department

All the materials are sent to the Quality Check Department to check for any short falls. Whether

to accept or reject. If its accepted the process is continued, if its rejected the materials are sent

back.

STEP 6: Stores Department

After accepting to quality check it goes to stores, stores ledger makes an entry. Material receipt

note is raised. Finance people enter the invoice in respective ledger.

STEP 7: Production Department

A note is issued (Issue note) to the respective department and then material goes to production

department. Then production begins immediately.

After the materials are received the Manufacturing Process begins.

Product Mix Offered

The product will be polypropylene sacks but the colors and printing will be according to the

requirement of the clients. The dimensions of the sacks can also be changed within the operating

range of the looms. The operating range is the minimum and maximum widths between which

the loom can operate.

The width of the sacks will depend on the operating range of the loom while the length can be

changed at will since the sacks can be cut and stitched according to requirements. The products

offered will be the sacks of various sizes, fabric can also be made by slitting One side of the

woven fabric which is in the form of a tube. This fabric is used for Packing purposes in the

Cement Industry.

MACHINERY INFORMATION

Some of the machines that are installed at our unit are as follows:

22

+ Extruders

+ Circular weaving machine

+ Stitching machine

+ Flexographic printing machine

+ Lamination plant (Tandem and Turn bar) Up to 2600 mm of tubular fabrics

+ Bale press machine

+ Automatic cutting & stitching machine

+ Gusseting machine

TECHNOLOGY AND PROCESSES

The Polypropylene Tape Making Process

The polypropylene tapes are manufactured by slitting films of PP or HDPE which are produced

by blown extrusion technique. In this process, the granules of plastic are fed to the extruder

through the hopper. Molten plastics are extruded through circular die and the tube is inflated by

blowing with air to a desired diameter, and pulling it away with a pair of nip rolls.

The extruded PP film is then coded and the bubble is collapsed. The film thus formed is then slit

to desired width. These tapes are stretched in orientation water bath which is at its boiling point.

Alternatively orientation can be carried out by using hot plate. The HDPE/PP tape, after

orientation, is stabilized and then wound on bobbins.

The Principle stages involved in tape manufacture are:

Extrusion of Film

Quenching of Film

Slitting of Film Into Tapes

Orientation of Tapes

Annealing of Tapes

Winding

The Polypropylene Fabric Weaving Process

From bobbins carrying polypropylene yarn, fabric is made using warping and yarn winding

machine. The fabric is then woven on looms and finally cut to size and stitched to sacks of

required dimensions.

Whenever required, the sacks are screen-printed using specially prepared ink. In some cases,

laminated sacks are required and as such before stitching and printing the fabric has to be

laminated by extrusion coating of LDPE. Lamination should be done from outside.

Weaving is done either by using Flat Looms or Circular Looms, the latter offers the following

advantages:

Higher output of fabric

23

Better retention of mechanical properties

Sack output is higher due to only one side stitching

Savings of 20-25% due to superior quality of tapes

Floor space savings is higher due to less number of operations.

The woven fabric is later coated with polymer by the Extrusion coating process.

Printing & Cutting

The woven fabric is feed to the printing and cutting machine which prints and cuts as per set

specifications.

Stitching

The woven fabric after printing and cutting operation is stitched manually.

Baling

In order to minimize the storage space occupied by finished sacks, five hundred sacks are packed

to form a bale and pressed in hydraulic baling press and strapped. The sacks are marked with

information as required by the buyer and each bale containing PP Sacks are marked with

standard mark.

Technology/Process Options

The technology is relatively uniform amongst suppliers of machinery. The granules are fed into

the extruder with the color granules and extruded into tape yarn which is then woven into the

fabric with circular looms which produces the fabric in the form of a tube.

SUMMARY OF THE MANUFACTURING PROCESS

PP Woven Sacks are generally manufactured and printed as per the Customers demands/needs.

The end users adopt different kinds of Color Combinations and Designs in the Printing of these

Sacks to convey the massage(s), characteristic(s), quantity & quality related details and handling

instructions etc. For some kind of specific applications like filling of Hydroscopic Materials e.g.

Chemicals, Fertilizers, Food Products etc. these Woven Sacks are laminated also.

The Process of manufacturing PP Woven Sacks involves following three steps:

1. Extrusion

2. Weaving

3. Finishing & Stitching

Extrusion

The process of manufacturing PP woven bags involves mixing raw materials starting with PP or

HDPE pellets and other additives, extruding the raw materials into a yarn PP resin is heated with

feeler of CaCo3 and pigment, melted and extruded as a flat film. It is then slit into tape yarn by

the slitting unit and stretched and annealed. Next, a take-up winder winds the heat oriented tape

yarn onto a bobbin.

The Raw Material (PP & Filler) in the Granules form is fed to a Raffia Tape Manufacturing Plant

24

to obtain the Raffia Tapes of PP. The Raw Material Mix is prepared in a Tray adjacent to the

Feed Hopper. The prepared Mix is sucked in to the Hopper by Vacuum. The Raw Material Mix

is fetched to the Extruder of the Plant; where the same is melt by applying controlled External

Heat on the Barrel. The Molten Mass is forced out through a Die Head into a Cooling Tank, in

the form of Sheet/Film. The cooled & solidified Sheet/Film is passed through the Knifes to

obtain Raffia Tapes of higher Denier (a Unit by which the fineness of a Yarn is measured). High

Density Polyethylene (HDPE) or Polypropylene (PP) granules are first converted in to 2.5 mm

wide tapes by Extrusion process. The Raffia Tapes received from the Plant are stretched and

annealed. These are then wound on Cheese Pipes with the help of the Sets of Winders.

Weaving

Weaving the yarn into a fabric in a process similar to the weaving of textiles. These flat tapes are

then woven into circular fabric by Circular weaving machine. Thus woven circular fabric is then

cut in to required dimension. Thread from the bobbin in the circular looms creel stand is woven

into tubular cloth The Weaving of Raffia Tapes into Cloths is carried out in Circular Looms,

which produce Circular Cloth of desired Width. The process of Weaving is Automatic and

Continuous in nature. Numbers of Circular Looms are installed so as to match the Effective

Output of the Raffia Tape manufacturing Plant. The Cloth produced by each Loom is

continuously wound on Rotating Pipes.

Finishing & Stitching

The Rolls of Woven Cloth are carried out to the Finishing & Stitching Section of the Unit. The

Cloth is cut into desired size and the printed. After printing the cut pieces are sent for stitching.

Prior to the stitching of the Cloth, a valve is made in one corner of the cut piece, as per the

Customers specification. The Woven Sacks passed through the Quality Control Test are bundled

in 500 or 1000 Nos. and pressed on a Bailing Press. The pressed Woven Sacks are wrapped,

bundled, packed and dispatched.

The Quality Control checks are carried out at each and every step to avoid rejections. The

parameters pertaining to the Weight, Denier, Bursting Strength etc. are strictly adhered to.

25

STEPS IN MANUFACTURING PROCESS

Woven sacks manufacturing process is a web of several steps from tape making to weaving of

tape into fabric, printing and stitching. The various stages in woven sacks manufacturing process

at Jakhotia includes:

Line Diagram of Manufacturing Process

Process Stages

Products output

C

CHDPE /PP GRANULES

C TAPE LINES

Tape (Flat Yarn)

C WINDERS

Yarn wound on Cheese

Pipes

CCIRCULAR LOOMS

C,

Woven Fabrics

C

C FABRICS CUTTING MACHINE

,

C

Woven Fabrics pieces

C

STITCHING MACHINE

Unprinted Bags/sacks

C PRINTING MACHINE

Printed Bags

BALE PACKING

C Finished bags/Fabrics

bales

FINISHED GOODS

C,C

Ready for dispatch

26

INVENTORY MANAGEMENT

Effective inventory management is all about knowing what is on hand, where it is in use,

and how much finished product results.

Inventory management is the process of efficiently overseeing the constant flow of units into and

out of an existing inventory. This process usually involves controlling the transfer in of units in

order to prevent the inventory from becoming too high, or dwindling to levels that could put the

operation of the company into jeopardy. Competent inventory management also seeks to control

the costs associated with the inventory, both from the perspective of the total value of the goods

included and the tax burden generated by the cumulative value of the inventory.

Just In Time Inventory Management

JIT, or just in time, inventory is a inventory management strategy that is aimed at monitoring

the inventory process in such a manner as to minimize the costs associated with inventory

control and maintenance. To a great degree, a just-in-time inventory process relies on the

efficient monitoring of the usage of materials in the production of goods and ordering

replacement goods that arrive shortly before they are needed. This simple strategy helps to

prevent incurring the costs associated with carrying large inventories of raw materials at any

given point in time.

Another application of a just in time inventory focuses not on raw materials but on finished

goods. Again, the idea is to develop a solid understanding of what is needed to produce goods

and schedule them for shipment to customers within the shortest time frame possible. As with

raw materials, shipping finished goods shortly after producing them leads to minimizing storage

costs and any taxes that may be applicable. This dual application of a just in time

inventory strategy can significantly cut the operational expenses of a business in regards to the

amount of inventory that must be stored at any one time and the amount of taxes that must be

paid on larger inventories.

A just in time inventory management process involves understanding how much of a given item

is needed to maintain production while more of the same item is ordered. This involves two key

factors. First, it is necessary to know how long it will take for the item to be shipped from the

supplier and arrive at the manufacturing facility. Second, the anticipated life or usage of the item

must be determined. By knowing these two pieces of information, it is possible to establish

procedures that allow the item to be reordered just in time to arrive and replace a worn item,

without having the replacement set in storage for an extended period of time.

27

The main Benefits of Just In Time Manufacturing System are as follows:

1. Funds that were tied up in inventories can be used elsewhere.

2. Areas previously used, to store inventories can be used for other more productive uses.

3. Throughput time is reduced, resulting in greater potential output and quicker response to

customers.

4. Defect rates are reduced, resulting in less waste and greater customer satisfaction.

The main Disadvantages of Just in Time Manufacturing System are as follows:

1. Implementing thorough JIT procedures can involve a major overhaul of your business

systems - it may be difficult and expensive to introduce.

2. JIT manufacturing also opens businesses to a number of risks, notably those associated

with your supply chain. With no stocks to fall back on, a minor disruption in supplies to

your business from just one supplier could force production to cease at very short notice.

28

PART B

INTERNSHIP WORK REPORT

AUDITING

Details of Auditing Practices of The Company

+ Internal Audit Quarterly

+ External Audit - Yearly

+ Tax Audit Yearly

The quarterly Audit was going on while we were there in the company. Helped and assisted the

Auditor in the Auditing Process.

AUDIT PROGRAMME:

Initial Engagement

Here we check the Opening Balance of current year with that of the Closing Balance of

Previous Year. And whether there is any discrepancy.

Vouching for period between 1/4/2010 to 31/3/2011

Purchases

Sales

Cash Receipts

Cash Payments

Vouching is done with the help of various original documents and vouchers that are

acquired from the Organization that are matched with the recorded entries in the financial

statements using Tally. Details like the Date, Quantity, Price, Amount, various Taxes and

their percentages, etc. are checked.

Verification of

Excise Duty

Service Tax

VAT Last date of payment for every month should be before the 20

th

of next month.

TDS Last date of payment of every month should be before the 7

th

of next month. For

the month of March 3 months grant is allowed.

Verification of various Taxes and Duties are checked. The percentages, amount,

payment, etc. are checked.

Cross check with Cash Deposited with Bank and Cash Withdrawal from Bank with the Bank

Statement.

Verification of BRS Opening and Closing.

29

Addition and Deletion of Fixed Assets and Depreciation there on.

Addition and Deletion of Assets should be supported by various Documents.

Depreciation whether calculated on according to The Companies Act, 1967 or according

to The Income Tax (Regulation) Act, 1961.

Any difference in the amount of tax due to the above reason should be notified and the

difference amount should be recorded in the liabilities side of balance sheet under the

head Deferred Tax Liability

Cash payment exceeding Rs. 20,000/-

If there are any cash payments exceeding Rs. 20,000; it should be notified with the reasons

and the amount there on.

Provision for expenses

Provisions for expenses should be documented and noted along with the details of the

particular expenses and the amount there in.

Summary of Audit approach

The audit approach was based on an assessment of the audit risk relevant to the individual

elements of the financial statements. The assessment or the verification has been done on the

basis of books of account prepared by the concern, however the auditor is not liable for the facts

which are concealed and kept out of books which couldn't be identified on the ordinary course

Summary of audit strategy

+ Generating an understanding of the business through discussions with management and a

review of the management accounts;

+ Reviewing the design and implementation of the internal financial control systems to the

extent that they have a bearing on the highest risk areas of the financial statements;

+ Assessing the audit risk and, based on that assessment and the assessment of the design of the

internal control system, developing and implementing appropriate audit procedures;

+ Reviewing the adequacy of material disclosures in the financial statements; and

+ Verifying all material balance sheet accounts and performing analytical review of income

and expenditure streams.

30

COST SHEET

Cost sheet is a statement, which shows various components of total cost of a product.

For determination of total cost of production a statement showing the various elements of cost is

prepared. This statement is called as a statement of cost or cost sheet

Cost sheet is a statement which provides assembly of the detailed cost of a cost center or a cost

unit. It is a statement showing the details of

a) Total cost of job

b) Cost of an operation or order.

It brings out the composition of total cost in a logical order under proper classifications & sub-

divisions. Separate columns are provided to show total cost, cost per-unit etc. A cost sheet is

prepared under output or unit costing method.

It is usually adopted when there is only one product is produced and all costs are incurred for that

product only. In case of different products there are different cost sheets for different products.

Cost sheet may be prepared for a week, monthly, quarterly or yearly indicating various

components of cost as prime cost, works cost, cost of production, cost of goods sold, total cost

and also profitability on a production.

The preparation of cost sheet depends on the cost data provided by cost accounting. Due to

differences in the nature of cost data there are three different cost sheet Performa may be used.

(a) Cost sheet with break up cost: These types of cost sheet contain two columns as total cost

and cost per unit of output.

(b) Cost Sheet with treatment of Stock: This type of cost sheet is maintained in case of

manufacturing concern. Generally there are three types of stock as (1) Stock of Raw material, (2)

Stock of work in progress and (3) Stock of finished goods.

(c) Estimated cost sheet or price quotation: Price quotation means quoting the minimum price

for obtaining a specific order. The quotation is sent in the form or estimated cost sheet having

one column. In estimated cost sheet all elements of cost and overhead expenses are calculated in

the following manner.

Estimated direct material

Estimated labor cost

Estimated overheads

PURPOSE OF COST SHEET

+ It gives the breakup of total cost under different elements.

+ It shows total cost as well as cost per unit.

31

+ It helps in comparison with previous years.

+ It facilities preparation of tenders or quotations.

+ It enables the management to fix up selling price.

+ It controls cost.

Cost Sheet helps in:

1. Stage wise cost identification

Costs such as prime cost, factory cost, cost of production, cost of goods sold, total cost of

sale etc.

2. Determine the cost per unit

This helps in determining cost per unit on which the future cost can be predicted.

DIVISIONS OF COST

Prime Cost

It comprises of all direct materials, direct labor and direct expenses. It is also known as flat cost.

Prime cost = Direct Materials + Direct Labor + Direct Expenses

Works / Factory Cost

It is also known as a factory cost or cost of manufacture. It is the cost of manufacturing an

article. It includes prime cost and factory expenses.

Works Cost = Prime Cost + Factory Overheads

Cost Of Production

It represents factory cost plus administrative expenses.

Cost of Production = Factory Cost + Administrative Expenses

Total Cost

It represents cost of production plus selling and distribution expenses.

Total Cost= Cost of Production + Selling & Distribution Expenses

Selling Price

It is the price which includes total cost plus margin of profit or minus loss, if any.

Selling Price = Total Cost + Profit (-Loss)

32

Non-Cost Items

Non-cost items are those items which do not form part of cost of a product. Such items should

not be considered while ascertaining the cost of a product. These are items included in the Profit

& Loss A/c. These will not come in the cost sheet

a) Income tax

b) Interest on capital

c) Interest on loan

d) Profit on Sale of fixed assets

e) All the assets

f) Donations

g) Capital Expenditure

h) Discount on shares & Debentures

i) Commission to Partners, Managers etc

j) Brokerage

k) Preliminary Expenses Written off

l) Wealth tax etc

m) Bonus to directors and employees if it is based on profit, expenses of raising capital,

penalties & fines.

Preparation Of Cost Sheet

The various components of cost explained above are presented in the form of a statement. Such a

statement of cost consists of prime cost, works cost, cost of production of goods, cost of goods

sold, total cost and sales and is termed as cost sheet.

- In Jakhotia Group of Companies the cost sheets are prepared to determine the Cost per

Process and the Cost per Product.

- The Finished product of a process is the Raw material of the next Process.

UTILITY OF COST SHEET

+ Determine the total cost

A total cost sheet (statement) helps in determining aggregate cost of manufacturing a product

or providing a service.

+ Determining product price

A cost sheet helps in identifying the total cost for a product or service which in turn helps in

properly pricing of products & services.

+ Cost reduction or cost control

Cost sheets helps in identifying the total cost stage wise & any unwanted cost can be

curtailed.

+ Prepare budgets

33

A cost statement helps in preparing budget for each department.

+ Profit planning

It helps to minimize cost & increase profits.

ESSENTIAL OF AN EFFECTIVE COSTING SYSTEM

The essential features that an effective costing system should possess are as follows:

+ Costing system should be tailor made, practical, simple and capable of meeting the

requirements of a business concern.

+ The method of costing should be suitable to the industry.

+ The data used by the system should be accurate, otherwise it may distort the output of

system.

+ Necessary co-operation and participation of executives from various departments of the

concern is essential for developing good cost accounting system.

+ The cost of installing and operating the system should justify the results.

+ The system of costing should not sacrifice the utility by introducing meticulous and

unnecessary details.

34

FINANCIAL STATEMENTS ANALYSIS

What Are Financial Statements?

Financial statements are documents showing the financial position of a company. The four main

statements are the balance sheet, income statement, cash flow statement, and statement of

retained earnings (or shareholders' equity).

What is Financial Statement Analysis?

Financial statement analysis takes specific line items from a financial statement and turns them

into easy-to-understand data or information.

Why Financial Analysis Is Needed?

Numbers on financial statements can be confusing. Analysis of the numbers gives you or outside

investors a better perspective of how your company is managing money and operations.

How Are Financial Statements Developed?

Financial statements are a key part of business finances and are used for many different reasons,

primarily as a form of analysis within the company. Outside of the company, lenders and

investors alike study financial statements in order to make key investment decisions, so

preparing financial statements is important even for small business owners and entrepreneurs.

Fortunately, the major financial statements are very common and there are well-established ways

to develop them for most businesses.

Interpreting Financial Statement Analysis

Financial statement ratios must be considered in the context of industry standards. Ratios should

be compared to benchmarks of similar businesses to determine a company's overall financial

health.

Need for Financial Statement Analysis

Companies conduct financial statement analysis to understand their financial health during the

statement period. By using these statements wisely, an individual can gauge the company's

present financial scenario, as well as make projections for the immediate future. The company

also makes extensive use of financial ratios and graphs. With this, one understands the relation

between the company's assets and its productivity. Financial statement analysis is extremely

beneficial for the company's management, its shareholders, its creditors and the government.

Parties Interested In Financial Statement Analysis

The analysis of financial figures contained in the company's profit and loss account and balance

sheet by employing appropriate technique is known a financial statement analysis. Financial

statement analysis is useful to different parties to obtain the required information about the

organization. Following are the parties interested in financial statement analysis.

1. Shareholders:

35

Shareholders are interested in financial statement analysis to know the profitability of the

organization. Profitability shows the growth potentiality of an organization and safety of

investment of shareholders.

2. Investors And Lenders:

Investors and lenders are interested to know the solvency position of an organization. They

analyze the financial statement position to know about the safety of their investment and ability

to pay interest and repayment of principle amount on due date.

3. Creditors:

Creditors are interested in analyzing the financial statements in order to know the short term

liquidity position of an organization. Creditors analyze the financial statement to know whether

the organization is able to pay the amount of short term liabilities on due date or not.

4. Management:

Management is interested to analyze the financial statement for measuring the effectiveness of its

policies and decisions. It analyze the financial statements to know short term and long term

solvency position, profitability, liquidity position and return on investment from the business.

5. Government:

Government is interested to analyze the financial position in determining the amount of tax

liability. It also helps for formulating effective plans and policies for economic growth.

Objectives Of Financial Statement Analysis

The major objectives of financial statement analysis are as follows

1. Assessment Of Past Performance:

Past performance is a good indicator of future performance. Investors or creditors are interested

in the trend of past sales, cost of good sold, operating expenses, net income, cash flows and

return on investment. These trends offer a means for judging management's past performance

and are possible indicators of future performance.

2. Assessment of current position:

Financial statement analysis shows the current position of the firm in terms of the types of assets

owned by a business firm and the different liabilities due against the enterprise.

3. Prediction of profitability and growth prospects:

Financial statement analysis helps in assessing and predicting the earning prospects and growth

rates in earning which are used by investors while comparing investment alternatives and other

users in judging earning potential of business enterprise.

36

4. Prediction of bankruptcy and failure:

Financial statement analysis is an important tool in assessing and predicting bankruptcy and

probability of business failure.

5. Assessment of the operational efficiency:

Financial statement analysis helps to assess the operational efficiency of the management of a

company. The actual performance of the firm which is revealed in the financial statements can be

compared with some standards set earlier and the deviation of any between standards and actual

performance can be used as the indicator of efficiency of the management.

Methods Or Techniques Of Financial Statement Analysis

Financial statement analysis can be performed by employing a number of methods or techniques.

The following are the important methods or techniques of financial statement analysis.

1. Ratio Analysis:

Ratio analysis is the analysis of the interrelationship between two financial figures.

2. Cash Flow Analysis:

Cash flow analysis is the analysis of the change in the cash position during a period.

3. Comparative Financial Statements:

Comparative financial statement is a analysis of financial statements of the company for two

years or of the two companies of similar types.

4. Common-size Financial Statements:

Common-size financial statement is a analysis of financial statements of the company, where

there is a base element taken from the financial statement and every other elements are taken as a

percentage of that base element.

5. Trend Analysis:

Trend analysis is the analysis of the trend of the financial ratios of the company over the years.

The methods to be selected for the analysis depend upon the circumstances and the users' need.

The user or the analyst should use appropriate methods to derive required information to fulfill

their needs.

Limitations Of Financial Statement Analysis

Although analysis of financial statement is essential to obtain relevant information for making

several decisions and formulating corporate plans and policies, it should be carefully performed

as it suffers from a number of the following limitations.

1. Mislead the user:

The accuracy of financial information largely depends on how accurately financial statements are

37

prepared. If their preparation is wrong, the information obtained from their analysis will also be

wrong which may mislead the user in making decisions.

2. Not useful for planning:

Since financial statements are prepared by using historical financial data, therefore, the

information derived from such statements may not be effective in corporate planning, if the

previous situation does not prevail.

3. Qualitative aspects:

Then financial statement analysis provides only quantitative information about the company's

financial affairs. However, it fails to provide qualitative information such as management-labor

relation, customers satisfaction, managements skills and so on which are also equally important

for decision making.

4. Comparison not possible:

The financial statements are based on historical data. Therefore comparative analysis of financial

statements of different years cannot be done as inflation distorts the view presented by the

statements of different years.

5. Wrong judgment:

The skills used in the analysis without adequate knowledge of the subject matter may lead to

negative direction . Similarly, biased attitude of the analyst may also lead to wrong judgment and

conclusion.

The limitations mentioned above about financial statement analysis make it clear that the

analysis is a means to an end and not an end to itself. The users and analysts must understand the

limitations before analyzing the financial statements of the company.

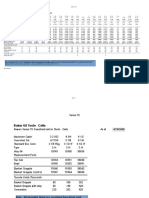

Financial Statement Analysis

With reference to ANNEXTURE

Various Analysis tools are used to Analyze the Statements provided by the company i.e. Balance

Sheet and Profit & Loss a/c of 2009-2010 and 2010-2011.

Comparative Statement

Common-size Statement

Ratio Analysis

Schedule of change in Working Capital

38

+ COMPARATIVE STATEMENT ANALYSIS (CFS)

The CFS helps a financial analyst in horizontal analysis of the firm and in establishing operating

and positional trend of the firm. The CFS may be prepared to show

1. The absolute amount of different items in monetary terms,

2. The amount of periodic changes in monetary terms,

3. The percentages of periodic changes to reveal the proportionate changes.

The CFS can be prepared for both the BS and the IS.

Comparative Income Statement (CIS):

A CIS shows the figure of different items of the Income Statement of the firm in absolute terms,

the absolutes changes from one period to another and if desired, the changes in percentage from.

The CIS is helpful in deriving meaningful conclusions regarding changes in sales volume,

different expense items, etc.

From CIS, a financial analyst can quickly ascertain whether sales are increasing or decreasing

and by how much amount or by how much percentage. Similarly, analysis can be made for other

items also.

Comparative Balance Sheet (CBS)

A CBS shows the different assets and liabilities of the firm on different dates to make

comparisons of absolute balances and also of changes if any, from one date to another. The CBS

may be helpful in analyzing and evaluating the financial position of the firm over a period of

number of years.

+ COMMON SIZE STATEMENT (CSS)

The CSS represents the relationship of different items of financial statements with some

Common item by expressing each item as a percentage of the Common item.

In Common Size Balance Sheet each item of the Balance Sheet is stated as percentage of the

total of the Balance Sheet.

Similarly in Common Size Income Statement, each item is stated as a percentage of the Net

Sales.

The Percentages of different items are computed by dividing the absolute amount of that item by

the Common Base (i.e., the Balance Sheet total or the Net Sales as the case may be) and then

multiplying by 100. The percentages so calculated can be easily compared with the

corresponding percentages in some other period.

39

Thus, the CSS is useful not only in intra-firm comparisons over a series of different year but also

in making inter-firm comparisons for the same year or for several years.

+ RATIO ANALYSIS (RA)

The RA has emerged as the principal technique of the AFS. A ratio is a relationship expressed in

mathematical terms between two individual or groups of figures connected with each other is

some logical manner.

The RA is based on the premise that a single accounting figure by itself may not communicate

any meaningful information but when expressed as relative to some other figure, it may

definitely give some significant information.

The relation between two or more accounting figure/groups is called a financial ratio.

A financial ratio helps to summarize a large mass of financial data into a concise form and to

make meaningful interpretations and conclusions about the performance and positions of a firm.

FINANCIAL STATEMENT ANALYSIS INTERPRETATION

INTERPRETATIONS

COMPARATIVE STATEMENT ANALYSIS

CIS:

On the basis of CIS, it can be said that PBT for the year 2010-2011 has increased by 23.67%

over the PBT for the year 2009-2010.

The Income during the same period has increased by 22.69% which was coupled with the

increase in the Expenses which also increased by same 22.69%. This means that Input/Output

ratio or the production efficiency level has been maintained during the period 20010-2011.

The same increase of 22.69% in Income and Expenditure has resulted in increase in the PBT by

23.67%.

CBS:

The CBS also reveals many facts about the composition of the assets and the financial structure

of the firm.

The Fixed Assets has decreased over the period by 12.60%, though this decrease has primarily

resulted by the amount of depreciation.

The increase in Current Assets is less than the Current Liabilities. The Current Assets have

increase by 137% and the Current Liabilities have increased by 177.26%. It means that the Net

40

Current Assets have increased by 46.40%. Therefore, the Net Working Capital in increased by

46.40%.

The firm has not raised any capital during the period and the increase in the Share Capital is

resulted due the receipt of the Share application money pending allotment.

The Secured Loans have decreased by 16.52%, whereas the Unsecured Loans have increased by

5.37%.

The increase in the Sources of Funds by 2.38% is matched with the increase in the Application of

Funds by 2.38%.

COMMON SIZE STATEMENT ANALYSIS

The Common Size BS and the Common Size IS reveal that proportion of fixed assets out of total

assets has reduced from 72.36% to 61.80% where as the amount of Current Assets have

increased from 82.12% to190.64%. This simply shows the increasing reliance of the firm on the

Current Assets.

Out of the total liabilities the total of proprietors funds has increased from 40.40% to 49.12%

where as the proportion of external liabilities has reduced from 59.60% to 50.88%. Since, no

new capital has been issued and the other liabilities have reduced, the proportion of capital in the

total financing of firm has gone up, this is due to the increase in the proportion of Reserves &

Surplus from 4.30% to 13.56%.

Further, the Total Expenditure as well as the PBT have remained pegged at 99.44% and 0.56%

respectively, of the Total Income. However, the Net Profit has reduced from 0.48% to 0.42% of

Total Income. This is due to the increase in the proportion of Provision for Tax from 0.09% to

0.16%.

41

SWOT ANALYSIS

STRENTHS:

Growing industrialization in India leading more demand of sophisticated packaging by

the end customer.

The demand is directly related to demand of end product so till time a new better material

does not come to replace the position is safe.

No big player entering in the market.

WEAKNESS:

Training required for handling of bags.

Jute and food grain are most competitive.

Low re-sale value

Stack ability height less than jute.

High Capacity of production to get profit.

One of the major problems concerning this industry is the quality of manpower, which is

generally of lower profile mainly illiterate labour force abounds these factories.

OPPORTUNITY:

Growing Cement requirement.

a) Northern Region: Cement Production has been increased by 11%, whereas

consumption by 3 %

b) Western Region: Cement Production has been reduced by 3%, whereas consumption

by 8 %

c) Eastern Region: Cement Production has been increased by 7%, whereas consumption

by 10 %

d) Central Region: Cement Production has been increased by 3%, whereas consumption

by 5 %

e) Southern Region: Cement Production has been increased by 7%, whereas consumption

has increased by 11%

Food grain can prove as a huge market.

Poor showing of jute industry.

THREATS:

Lesser availability of Raw Materials for production of polymer bags.

Expected fall in cement prices might affect polypropylene consumption.

International fluctuating of petroleum prices may affect industry.

Not biodegradable.

High dependency on labor.

42

WEEKLY LOG REPORT

WEEK ONE:

+ Introduction to the company.

+ Visit to one of the factory location of the company i.e. at Jeedimetla, Hyderabad.

+ Activities or Process that takes place in the factory.

+ Looked at the MANUFACTURING PROCESS that goes on in the factory.

WEEK TWO AND THREE:

+ Worked at the head office which is located in Basheerbagh, Hyderabad.

+ Recording of various transactions in vouchers using TALLY.

WEEK FOUR:

+ Getting to know the company in detail.

+ All the PRACTICES AND POLICIES of the company were observed.

+ Along with and with the help of the manager understood the works and detail functioning

of the company.

+ SWOT analysis of the company.

WEEK FIVE:

+ There was AUDITING going on in the firm. So we assisted the Auditor.

+ Learnt some of the concepts of auditing and taxation.

+ Vouching of Purchase, Sales, Cash Receipts and Payments

+ Verification of books of accounts.

WEEK SIX:

+ Understanding and analysis of COST SHEET with the help of the manager.

+ Looking at each and every step involved in production process and cost incurred in such

process.

+ Stage wise cost identification

Costs such as prime cost, factory cost, cost of production, cost of goods sold, total cost of

sale etc.

+ Determination of the cost per unit

This helps in determining cost per unit on which the future cost can be predicted.

WEEKSEVEN AND EIGHT:

43

+ Was provided with the various Financial Statements i.e. Balance Sheet Statement and

Profit & Loss Statement of the year 2009-2010 and 2010-2011.

+ FINANCIAL STATEMENT ANALYSIS - getting the proper understanding of each and

every tool.

+ Various Financial Statement Analysis Tools were used to analyze the Financial

Statements of the Company.

+ Application of tools like

Comparative Statement Analysis

Common-size Statement Analysis

Ratio Analysis

Schedule of changes in Working Capital

+ Interpretations and Explanation.

44