You might also like

- Critical Race TheoryDocument13 pagesCritical Race TheorySudip PatraNo ratings yet

- LEGAL TECHNIQUE AND LOGIC: Premises, Inference and ConclusionsDocument9 pagesLEGAL TECHNIQUE AND LOGIC: Premises, Inference and ConclusionsAizaFerrerEbinaNo ratings yet

- Assignment On Public FinanceDocument21 pagesAssignment On Public Financepadum chetry100% (1)

- Ricoeur David HallDocument209 pagesRicoeur David HallanimalismsNo ratings yet

- Gilles Deleuze's Logic of Sense - A Critical Introduction and GuideDocument233 pagesGilles Deleuze's Logic of Sense - A Critical Introduction and GuideSanggels Kim89% (9)

- Ethics Utilitarian and Kantian Ethics and WarDocument3 pagesEthics Utilitarian and Kantian Ethics and Warapi-3729409100% (3)

- Economics Answers 2Document14 pagesEconomics Answers 2Rakawy Bin RakNo ratings yet

- History of Economic ThoughtDocument49 pagesHistory of Economic ThoughtMateuNo ratings yet

- EU State Aid Law ExplainedDocument6 pagesEU State Aid Law ExplainedLuisa LopesNo ratings yet

- Classic Theories of Economic Development: Four Approaches: Linear Stages TheoryDocument4 pagesClassic Theories of Economic Development: Four Approaches: Linear Stages TheoryCillian ReevesNo ratings yet

- Regulations in IndiaDocument8 pagesRegulations in IndiaHimanshu GuptaNo ratings yet

- Geographical ImaginationsDocument228 pagesGeographical ImaginationsJuanCitoNo ratings yet

- Indian Takeover CodeDocument10 pagesIndian Takeover CodeMoiz ZakirNo ratings yet

- Introduction To The Marxist LensDocument34 pagesIntroduction To The Marxist Lensrawan allamNo ratings yet

- Applying Semiotics As A Technique On Different Advertisement To Endorse Their ProductsDocument11 pagesApplying Semiotics As A Technique On Different Advertisement To Endorse Their Productsapi-375702257100% (1)

- International Trade TheoriesDocument6 pagesInternational Trade TheoriesQueenie Gallardo AngelesNo ratings yet

- Cultural Studies ExplainedDocument9 pagesCultural Studies ExplainedArif widya100% (1)

- Derrida's Deconstruction of Kafka's "Before the LawDocument14 pagesDerrida's Deconstruction of Kafka's "Before the LawjuanevaristoNo ratings yet

- Teacher philosophies and educational theories quizDocument7 pagesTeacher philosophies and educational theories quizodelle100% (2)

- Law of Diminishing Marginal Returns PDFDocument3 pagesLaw of Diminishing Marginal Returns PDFRaj KomolNo ratings yet

- Neo-Classical Economics Cannot Provide Solutions To The Problems We Face Today. DiscussDocument10 pagesNeo-Classical Economics Cannot Provide Solutions To The Problems We Face Today. DiscussAdada Mohammed Abdul-Rahim BatureNo ratings yet

- Managerial Economics Practice Problem SetDocument7 pagesManagerial Economics Practice Problem SetAkshayNo ratings yet

- Refusal To Deal in The EUDocument32 pagesRefusal To Deal in The EUFrancis Njihia KaburuNo ratings yet

- F4eng 2010 AnsDocument12 pagesF4eng 2010 AnssigninnNo ratings yet

- From Crisis To Financial Stability Turkey Experience 3rd EdDocument98 pagesFrom Crisis To Financial Stability Turkey Experience 3rd Edsuhail.rizwanNo ratings yet

- Hw1 Andres-Corporate FinanceDocument8 pagesHw1 Andres-Corporate FinanceGordon Leung100% (2)

- Dissertation On Financial Crisis 2008Document115 pagesDissertation On Financial Crisis 2008Brian John SpencerNo ratings yet

- Mergers and Acquisitions of Financial Institutions: A Review of The Post-2000 LiteratureDocument24 pagesMergers and Acquisitions of Financial Institutions: A Review of The Post-2000 LiteratureImran AliNo ratings yet

- Lecture Notes - Welfare EconomicsDocument23 pagesLecture Notes - Welfare EconomicsJacksonNo ratings yet

- Separability and Competence-Competence in International ArbitrationDocument22 pagesSeparability and Competence-Competence in International ArbitrationRajatAgrawalNo ratings yet

- Economics of Industry PPT Lecture 1Document62 pagesEconomics of Industry PPT Lecture 1rog67558No ratings yet

- Labour Welfare Legislation in IndiaDocument27 pagesLabour Welfare Legislation in IndiaSweta SinhaNo ratings yet

- Circular Flow of EconomyDocument19 pagesCircular Flow of EconomyAbhijeet GuptaNo ratings yet

- Report On The Public Policy Exception in The New York Convention - 2015 PDFDocument19 pagesReport On The Public Policy Exception in The New York Convention - 2015 PDFJorge Vázquez ChávezNo ratings yet

- NTU Adam Smith EssayDocument19 pagesNTU Adam Smith EssayNg Hai Woon AlwinNo ratings yet

- Bank of Zambia Act Zambian Banking LawsDocument33 pagesBank of Zambia Act Zambian Banking LawsNoah AlutuliNo ratings yet

- Abuse of Dominant Position in Competition LawDocument23 pagesAbuse of Dominant Position in Competition LawKalyani AbhyankarNo ratings yet

- Circular Flow of IncomeDocument193 pagesCircular Flow of Incomeallah dittaNo ratings yet

- Corporate Social ResponsibilityDocument9 pagesCorporate Social ResponsibilityMartijn ReekNo ratings yet

- University of Saint Anthony's Guide to Economic GrowthDocument20 pagesUniversity of Saint Anthony's Guide to Economic GrowthAlly GelayNo ratings yet

- 1 Solomon Chapter 2 Banking, Insurance & MicrofinanceDocument121 pages1 Solomon Chapter 2 Banking, Insurance & MicrofinanceLAKEW SHIFERAWNo ratings yet

- Institutions and Long-Term Economic Growth - The Holy Grail of Political EconomyDocument16 pagesInstitutions and Long-Term Economic Growth - The Holy Grail of Political EconomyTommey82No ratings yet

- Adam Smith's Invisible Hand Theory ExplainedDocument2 pagesAdam Smith's Invisible Hand Theory Explainedmano123No ratings yet

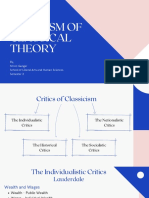

- Criticism of Classical TheoryDocument28 pagesCriticism of Classical TheoryShruti Gangar100% (1)

- Principles of Wto: 1. Trade Without DiscriminationDocument6 pagesPrinciples of Wto: 1. Trade Without DiscriminationNgocHuynhNo ratings yet

- How Self-Interest and Selfishness Impact EconomiesDocument2 pagesHow Self-Interest and Selfishness Impact EconomiesGino IgnacioNo ratings yet

- Demand and Supply - ExplanationDocument2 pagesDemand and Supply - Explanationfatwa3rohmanNo ratings yet

- Theories on Development in Third World CountriesDocument2 pagesTheories on Development in Third World CountriesAnireeth C Raj100% (1)

- International Economics I - Lecture NotesDocument2 pagesInternational Economics I - Lecture NotesMeer Hamza100% (1)

- Choosing Techniques and Capital Intensity in DevelopmentDocument12 pagesChoosing Techniques and Capital Intensity in DevelopmentShruthi ThakkarNo ratings yet

- The Product Life Cycle TheoryDocument6 pagesThe Product Life Cycle TheoryAyiik ToktookNo ratings yet

- Micro Economic PolicyDocument472 pagesMicro Economic PolicyMir Shoboocktagin Mahmud Dipu100% (6)

- International Trade Policy NOTES For Professor William J. Davey's CourseDocument35 pagesInternational Trade Policy NOTES For Professor William J. Davey's CourseLewis GNo ratings yet

- International Trade and Its Importance Adam Smith and The Theory of AA Narrative ReporttolosaDocument4 pagesInternational Trade and Its Importance Adam Smith and The Theory of AA Narrative ReporttolosaNicki Lyn Dela Cruz100% (1)

- Essay Paper On Stakeholder Theory Versus Shareholder ThoeryDocument5 pagesEssay Paper On Stakeholder Theory Versus Shareholder ThoeryThi ThaiNo ratings yet

- Lecture Notes On Eu Law Competition PDFDocument47 pagesLecture Notes On Eu Law Competition PDFNahmyNo ratings yet

- Bangladesh's Role in the WTODocument10 pagesBangladesh's Role in the WTOরাকিব অয়নNo ratings yet

- Econ 101 Intro to Basic ConceptsDocument4 pagesEcon 101 Intro to Basic ConceptsRudolph FelipeNo ratings yet

- Microeconomics FundamentalsDocument128 pagesMicroeconomics FundamentalsJEMALYN TURINGAN0% (1)

- National IncomeDocument4 pagesNational Incomesubbu2raj3372No ratings yet

- Insurance LawDocument24 pagesInsurance Lawfekadu bayisaNo ratings yet

- Innovation and Limits of AntitrustDocument50 pagesInnovation and Limits of AntitrustGlobalEconNo ratings yet

- Investor Protection Laws, Accounting and Auditing Around The WorldDocument40 pagesInvestor Protection Laws, Accounting and Auditing Around The Worlddion qeyenNo ratings yet

- Welfare EconomicsDocument6 pagesWelfare EconomicsVincent CariñoNo ratings yet

- Burden of Public DebtDocument4 pagesBurden of Public DebtAmrit KaurNo ratings yet

- Deontology and Utilitarianism Ethics TheoriesDocument7 pagesDeontology and Utilitarianism Ethics TheoriesMarianne GarciaNo ratings yet

- Ten Principles of EconomicsDocument3 pagesTen Principles of EconomicsArlette MovsesyanNo ratings yet

- TaxationDocument21 pagesTaxationmsjan019100% (1)

- Effects of Public ExpenditureDocument4 pagesEffects of Public ExpenditureRafiuddin BiplabNo ratings yet

- Joseph Stalin - Economic Problems of Socialism in The USSRDocument114 pagesJoseph Stalin - Economic Problems of Socialism in The USSRJay TharappelNo ratings yet

- Interview With George Habash - On The The Future of The Palestinian National Movement (1985)Document13 pagesInterview With George Habash - On The The Future of The Palestinian National Movement (1985)Jay TharappelNo ratings yet

- Interview With George Habash (1998) - TRANSCRIPTDocument17 pagesInterview With George Habash (1998) - TRANSCRIPTJay TharappelNo ratings yet

- Jay Tharappel - Indian Economic HistoryDocument39 pagesJay Tharappel - Indian Economic HistoryJay TharappelNo ratings yet

- Patnaik, U. The Agrarian Market Constraint in India After Fourteen Years of Economic Reforms and Trade LiberalisationDocument16 pagesPatnaik, U. The Agrarian Market Constraint in India After Fourteen Years of Economic Reforms and Trade LiberalisationJay TharappelNo ratings yet

- Export-Oriented Agriculture Policies Impact Food Security in Developing NationsDocument22 pagesExport-Oriented Agriculture Policies Impact Food Security in Developing NationsJay TharappelNo ratings yet

- Why The Novel MattersDocument1 pageWhy The Novel MattersMostaq AhmedNo ratings yet

- Negative and Positive Liberty: Alexis Carlos Cruz, Mpa Dpa StudentDocument15 pagesNegative and Positive Liberty: Alexis Carlos Cruz, Mpa Dpa StudentBatang MalolosNo ratings yet

- Introduce of Semantic MakalahDocument7 pagesIntroduce of Semantic MakalahAndi Muhammad EdwardNo ratings yet

- الاستقلال الفلسفي والتجديد عند طه عبد الرحمنDocument26 pagesالاستقلال الفلسفي والتجديد عند طه عبد الرحمنعبدالله عبدالقادرNo ratings yet

- Is Science Value-Free? Book ReviewDocument4 pagesIs Science Value-Free? Book ReviewMade DeddyNo ratings yet

- 2.2 Proportional EqualityDocument3 pages2.2 Proportional EqualityRhoddickMagrataNo ratings yet

- Assignment #1-Vocabulary Visual: Rick SmithDocument20 pagesAssignment #1-Vocabulary Visual: Rick SmithTechandTeachingNo ratings yet

- A Module in Introduction To Philosophy of The Human Person: Compiled By: Subject InstructorsDocument9 pagesA Module in Introduction To Philosophy of The Human Person: Compiled By: Subject InstructorsDanna GomezNo ratings yet

- Yasuo Deguchi, Jay L. Garfield, Graham Priest, Robert H. Sharf - What Can't Be Said - Paradox and Contradiction in East Asian Thought-Oxford University Press (2021)Document205 pagesYasuo Deguchi, Jay L. Garfield, Graham Priest, Robert H. Sharf - What Can't Be Said - Paradox and Contradiction in East Asian Thought-Oxford University Press (2021)AndersonNo ratings yet

- David Bloor Remember The Strong ProgramDocument14 pagesDavid Bloor Remember The Strong ProgramJhon LitleNo ratings yet

- Moravcsic-Appearance and Reality in Heraclitus' PhilosophyDocument18 pagesMoravcsic-Appearance and Reality in Heraclitus' PhilosophyМарина ВольфNo ratings yet

- Philosophy 2ND Quarter ExaminationDocument7 pagesPhilosophy 2ND Quarter Examinationalex100% (1)

- Hegel and the Christian God: Journal Article AnalysisDocument22 pagesHegel and the Christian God: Journal Article AnalysisAleiyandraNo ratings yet

- Othello As A School Text - Farouk Mitha PHD Thesis FINALDocument180 pagesOthello As A School Text - Farouk Mitha PHD Thesis FINALSarah ParkNo ratings yet

- Brock-The Ubiquitous Problem of Empty NamesDocument23 pagesBrock-The Ubiquitous Problem of Empty NamescgovicencioNo ratings yet

- Delacruz 12Document3 pagesDelacruz 12Anna DelacruzNo ratings yet

- Subalternity in The Pearl That Broke Its Shell: An Alternative Feminist AnalysisDocument14 pagesSubalternity in The Pearl That Broke Its Shell: An Alternative Feminist AnalysisIJ-ELTSNo ratings yet

- Disassembling Capital N PepperellDocument291 pagesDisassembling Capital N PepperellKathleen CliffordNo ratings yet

- Thomas Hill GreenDocument4 pagesThomas Hill GreenRohanNo ratings yet