You might also like

- Crown & Baptist Streets Village Group: ST Re EtDocument1 pageCrown & Baptist Streets Village Group: ST Re EtGeneric_PersonaNo ratings yet

- The Rise of The Individual in Modern ChinaDocument3 pagesThe Rise of The Individual in Modern ChinaGeneric_PersonaNo ratings yet

- Citizens United ReviewDocument5 pagesCitizens United ReviewGeneric_PersonaNo ratings yet

- Result of Portrayals of Latinos On TVDocument33 pagesResult of Portrayals of Latinos On TVGeneric_PersonaNo ratings yet

- Monument of Myth: The Basilica of Sacre CouerDocument20 pagesMonument of Myth: The Basilica of Sacre CouerGeneric_PersonaNo ratings yet

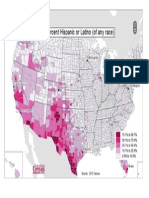

- US Map of Hispanic Population by CountyDocument1 pageUS Map of Hispanic Population by CountyGeneric_PersonaNo ratings yet

- Earnings of ImmigrantsDocument23 pagesEarnings of ImmigrantsGeneric_PersonaNo ratings yet

- Peach Leaf CurlDocument3 pagesPeach Leaf CurlGeneric_PersonaNo ratings yet

- Sydney As A Global CityDocument9 pagesSydney As A Global CityGeneric_PersonaNo ratings yet

- Measuring Helix Angle of GearsDocument6 pagesMeasuring Helix Angle of Gearsdarshan.hegdebNo ratings yet

- China and Sydney Australias Growing Business PartnershipDocument8 pagesChina and Sydney Australias Growing Business PartnershipGeneric_PersonaNo ratings yet

- English Language in Hong KongDocument13 pagesEnglish Language in Hong KongGeneric_PersonaNo ratings yet

- Sydney Australia's Green Sector OpportunityDocument8 pagesSydney Australia's Green Sector OpportunityGeneric_PersonaNo ratings yet

- Educated Preferences: Explaining Attitudes Toward Immigration in EuropeDocument44 pagesEducated Preferences: Explaining Attitudes Toward Immigration in EuropeGeneric_PersonaNo ratings yet

- US Policy and The International Dimensions of Failed Democratic Transitions in The Arab WorldDocument18 pagesUS Policy and The International Dimensions of Failed Democratic Transitions in The Arab WorldGeneric_PersonaNo ratings yet

- Agenda Setting, Public Opinion & Immigration ReformDocument21 pagesAgenda Setting, Public Opinion & Immigration ReformGeneric_PersonaNo ratings yet

- Grizzly Hevy Duty Wood Lathe ManualDocument60 pagesGrizzly Hevy Duty Wood Lathe ManualGeneric_PersonaNo ratings yet

- Promoting Economic Liberalization in EgyptDocument14 pagesPromoting Economic Liberalization in EgyptGeneric_PersonaNo ratings yet

- The Rise of The Individual in Modern ChinaDocument3 pagesThe Rise of The Individual in Modern ChinaGeneric_PersonaNo ratings yet

- The Diversity of Debt Crises in EuropeDocument18 pagesThe Diversity of Debt Crises in EuropeGeneric_PersonaNo ratings yet

- Protests in An Information SocietyDocument25 pagesProtests in An Information SocietyGeneric_PersonaNo ratings yet

- English Language in Hong KongDocument13 pagesEnglish Language in Hong KongGeneric_PersonaNo ratings yet

- Empowering Youth - Technology in Advocacy To Affect Social ChangeDocument18 pagesEmpowering Youth - Technology in Advocacy To Affect Social ChangeGeneric_PersonaNo ratings yet

- A Study On The Effects of Sexually Explicit Advertisement On MemoryDocument10 pagesA Study On The Effects of Sexually Explicit Advertisement On MemoryGeneric_PersonaNo ratings yet

- Hypothalamic Astrocytoma: Hyperphagia Syndrome & Accompanying IssuesDocument4 pagesHypothalamic Astrocytoma: Hyperphagia Syndrome & Accompanying IssuesGeneric_PersonaNo ratings yet

- Aggressive Behavior Following StrokeDocument5 pagesAggressive Behavior Following StrokeGeneric_PersonaNo ratings yet

- Prilleltensky.2008.Role of Power in Wellness-Oppression-Liberation - JCP PDFDocument21 pagesPrilleltensky.2008.Role of Power in Wellness-Oppression-Liberation - JCP PDFcastrolaNo ratings yet

- Internet, Mass Communication & Collective ActionDocument12 pagesInternet, Mass Communication & Collective ActionGeneric_PersonaNo ratings yet

- Title Insert (Derogatory Words) Research StudyDocument5 pagesTitle Insert (Derogatory Words) Research StudyGeneric_PersonaNo ratings yet

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Empanelment Application Form 2016Document4 pagesEmpanelment Application Form 2016venkatNo ratings yet

- Common Accounting Concepts and Principles: Going ConcernDocument3 pagesCommon Accounting Concepts and Principles: Going Concerncandlesticks20201No ratings yet

- Transpo Case Digests FinalsDocument21 pagesTranspo Case Digests Finalsaags_06No ratings yet

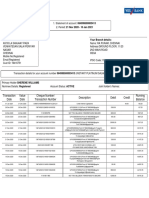

- Transaction Date Value Date Cheque Number/ Transaction Number Description Debit Credit Running BalanceDocument2 pagesTransaction Date Value Date Cheque Number/ Transaction Number Description Debit Credit Running Balancesylvereye07No ratings yet

- As 1816.1-2007 Metallic Materials - Brinell Hardness Test Test Method (ISO 6506-1-2005 MOD)Document3 pagesAs 1816.1-2007 Metallic Materials - Brinell Hardness Test Test Method (ISO 6506-1-2005 MOD)SAI Global - APACNo ratings yet

- Decongestion of PNP Lock-Up Cells DTD August 14, 2012 PDFDocument3 pagesDecongestion of PNP Lock-Up Cells DTD August 14, 2012 PDFjoriliejoyabNo ratings yet

- Overview of Data Tiering Options in SAP HANA and Sap Hana CloudDocument38 pagesOverview of Data Tiering Options in SAP HANA and Sap Hana Cloudarban bNo ratings yet

- Yamamoto Vs NishinoDocument3 pagesYamamoto Vs NishinoTricia SandovalNo ratings yet

- Applicti9n of Tcs - NQT - V1 - Bundle PackDocument17 pagesApplicti9n of Tcs - NQT - V1 - Bundle PackGopal Jee MishraNo ratings yet

- MTLBDocument121 pagesMTLBKIM KYRISH DELA CRUZNo ratings yet

- DOLE - DO 174 RenewalDocument5 pagesDOLE - DO 174 Renewalamadieu50% (2)

- Analysis of NPADocument31 pagesAnalysis of NPApremlal1989No ratings yet

- Spouses Firme Vs BukalDocument2 pagesSpouses Firme Vs Bukalpayumomichael2276No ratings yet

- Crisis After Suffering One of Its Sharpest RecessionsDocument5 pagesCrisis After Suffering One of Its Sharpest RecessionsПавло Коханський0% (2)

- Prophetic Graph Eng-0.17Document1 pageProphetic Graph Eng-0.17Judaz Munzer100% (1)

- Redress SchemeDocument164 pagesRedress SchemePhebeNo ratings yet

- Libcompiler Rt-ExtrasDocument2 pagesLibcompiler Rt-ExtrasNehal AhmedNo ratings yet

- Petron Corporation and Peter Milagro v. National Labor Relations Commission and Chito MantosDocument2 pagesPetron Corporation and Peter Milagro v. National Labor Relations Commission and Chito MantosRafaelNo ratings yet

- Memo Re Intensification of Anti-Kidnapping Stratergy and Effort Against Motorcycle Riding Suspects (MRS)Document2 pagesMemo Re Intensification of Anti-Kidnapping Stratergy and Effort Against Motorcycle Riding Suspects (MRS)Wilben DanezNo ratings yet

- Salonga Vs Cruz PanoDocument1 pageSalonga Vs Cruz PanoGeorge Demegillo Rocero100% (3)

- My Quiz For Negotiable InstrumentsDocument2 pagesMy Quiz For Negotiable InstrumentsJamie DiazNo ratings yet

- The Analysis of Foreign PolicyDocument24 pagesThe Analysis of Foreign PolicyMikael Dominik AbadNo ratings yet

- Affinity (Medieval) : OriginsDocument4 pagesAffinity (Medieval) : OriginsNatia SaginashviliNo ratings yet

- Bonsato Vs CA DigestDocument3 pagesBonsato Vs CA DigestFrances Ann Marie GumapacNo ratings yet

- 1854 - (Ennemoser) - The History of Magic Vol 1Document531 pages1854 - (Ennemoser) - The History of Magic Vol 1GreyHermitNo ratings yet

- Sanchez v. DemetriouDocument15 pagesSanchez v. DemetriouChristopher Martin GunsatNo ratings yet

- ASME B16-48 - Edtn - 2005Document50 pagesASME B16-48 - Edtn - 2005eceavcmNo ratings yet

- Break-Even Analysis Entails Calculating and Examining The Margin of Safety ForDocument4 pagesBreak-Even Analysis Entails Calculating and Examining The Margin of Safety ForMappe, Maribeth C.No ratings yet

- Goldman Sachs Risk Management: November 17 2010 Presented By: Ken Forsyth Jeremy Poon Jamie MacdonaldDocument109 pagesGoldman Sachs Risk Management: November 17 2010 Presented By: Ken Forsyth Jeremy Poon Jamie MacdonaldPol BernardinoNo ratings yet

- Sept. 2021 INSET Notice and Minutes of MeetingDocument8 pagesSept. 2021 INSET Notice and Minutes of MeetingSonny MatiasNo ratings yet