You might also like

- Letter To Prof R VaidyanathanDocument2 pagesLetter To Prof R Vaidyanathanrvaidya2000No ratings yet

- Aranganin Pathaiyil ProfileDocument5 pagesAranganin Pathaiyil Profilervaidya2000No ratings yet

- NOV 2008 India PR ApprovingInvestmentDocument6 pagesNOV 2008 India PR ApprovingInvestmentrvaidya2000No ratings yet

- RESERVE BANK OF INDIA - : Investment in Credit Information CompaniesDocument1 pageRESERVE BANK OF INDIA - : Investment in Credit Information Companiesrvaidya2000No ratings yet

- How Did China Take Off US China Report 2012 "Uschinareport - Com-Wp-Con... Ds-2013!05!23290284.PDF" (1) .PDF - 1Document25 pagesHow Did China Take Off US China Report 2012 "Uschinareport - Com-Wp-Con... Ds-2013!05!23290284.PDF" (1) .PDF - 1rvaidya2000No ratings yet

- SGFX FinancialsDocument33 pagesSGFX FinancialsPGurusNo ratings yet

- National Herald NarrativeDocument2 pagesNational Herald Narrativervaidya2000No ratings yet

- Subramanian Testimony 31313Document25 pagesSubramanian Testimony 31313PGurusNo ratings yet

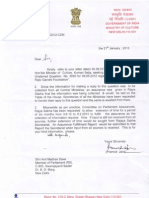

- Letter To PMDocument3 pagesLetter To PMrvaidya2000No ratings yet

- Vimarsha On Indian Economy - Myth and RealityDocument1 pageVimarsha On Indian Economy - Myth and Realityrvaidya2000No ratings yet

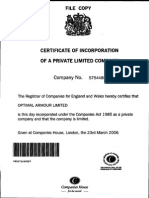

- Optimal Armour Corporate FilingsDocument198 pagesOptimal Armour Corporate FilingsPGurusNo ratings yet

- TVEs Growth Engines of China in 1980s - 1990s "WWW - Geoffrey-Hodgson - Inf... - Brakes-chinese-Dev - PDF"Document24 pagesTVEs Growth Engines of China in 1980s - 1990s "WWW - Geoffrey-Hodgson - Inf... - Brakes-chinese-Dev - PDF"rvaidya2000No ratings yet

- Ahmedabad Press Conference Nov 19 2015Document5 pagesAhmedabad Press Conference Nov 19 2015PGurus100% (1)

- Composite Resin Corporate FilingsDocument115 pagesComposite Resin Corporate FilingsPGurus100% (2)

- Letter and Invitaion Give To Mr. r.v19!06!2015Document2 pagesLetter and Invitaion Give To Mr. r.v19!06!2015rvaidya2000No ratings yet

- Brief Look at The History of Temples in IIT Madras Campus (Arun Ayyar, Harish Ganapathy, Hemanth C, 2014)Document17 pagesBrief Look at The History of Temples in IIT Madras Campus (Arun Ayyar, Harish Ganapathy, Hemanth C, 2014)Srini KalyanaramanNo ratings yet

- Sec 66ADocument5 pagesSec 66Arvaidya2000No ratings yet

- NGO's A Perspective 31-01-2015Document29 pagesNGO's A Perspective 31-01-2015rvaidya2000No ratings yet

- FDI in Retail - Facts & MythsDocument128 pagesFDI in Retail - Facts & Mythsrvaidya2000No ratings yet

- Why India Needs To Prepare For The Decline of The WestDocument4 pagesWhy India Needs To Prepare For The Decline of The Westrvaidya2000No ratings yet

- GrantsDocument1 pageGrantsrvaidya2000No ratings yet

- Representation To PMDocument31 pagesRepresentation To PMIrani SaroshNo ratings yet

- Timetable & AgendaDocument6 pagesTimetable & Agendarvaidya2000No ratings yet

- Shamelessness Is Paraded As ModernDocument2 pagesShamelessness Is Paraded As Modernrvaidya2000No ratings yet

- Humbug Over KashmirDocument4 pagesHumbug Over Kashmirrvaidya2000No ratings yet

- Secular Assault On The SacredDocument3 pagesSecular Assault On The Sacredrvaidya2000No ratings yet

- Why The Retail Revolution Is Meeting Its NemesisDocument3 pagesWhy The Retail Revolution Is Meeting Its Nemesisrvaidya2000No ratings yet

- Decline of The West Is Good For Us and Them - 11 Oct 2011Document4 pagesDecline of The West Is Good For Us and Them - 11 Oct 2011rvaidya2000No ratings yet

- Why The Indian Housewife Deserves Paeans of PraiseDocument3 pagesWhy The Indian Housewife Deserves Paeans of Praiservaidya2000No ratings yet

- Why Sub-Prime Is Not A Crisis in IndiaDocument4 pagesWhy Sub-Prime Is Not A Crisis in Indiarvaidya2000No ratings yet

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (890)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Case Study - JVG ScandalDocument2 pagesCase Study - JVG ScandalAdvay SinghNo ratings yet

- Introduction to Corporate FinanceDocument89 pagesIntroduction to Corporate FinanceBet NaroNo ratings yet

- Answer Scheme Tutorial Questions - Accounting Non-Profit OrganizationDocument7 pagesAnswer Scheme Tutorial Questions - Accounting Non-Profit OrganizationMoriatyNo ratings yet

- Guest Name: Cash MemoDocument1 pageGuest Name: Cash MemoAlpesh BhesaniyaNo ratings yet

- Journal, Ledger Trial BalanceDocument15 pagesJournal, Ledger Trial BalanceOmar Galal100% (1)

- GRA Strategic Plan Vers 2.0 06.12.11 PDFDocument36 pagesGRA Strategic Plan Vers 2.0 06.12.11 PDFRichard Addo100% (3)

- Marketing Trends 2024Document1 pageMarketing Trends 2024nblfuxinrqjjbtnjcs100% (1)

- Tata Steel LTDDocument15 pagesTata Steel LTDShardulNo ratings yet

- Essay - Education Should Be FreeDocument2 pagesEssay - Education Should Be FreeRuthie CamachoNo ratings yet

- Air India Brand Identity Case StudyDocument13 pagesAir India Brand Identity Case StudyAnkit JenaNo ratings yet

- Sabmiller AR 2011Document176 pagesSabmiller AR 2011gjhunjhunwala_1No ratings yet

- Statement of Employment Expenses For Working at Home Due To COVID-19Document2 pagesStatement of Employment Expenses For Working at Home Due To COVID-19Igor GoesNo ratings yet

- MKT-SEGDocument63 pagesMKT-SEGNicolas BozaNo ratings yet

- Barton InteriorsDocument36 pagesBarton InteriorsAhmed MasoudNo ratings yet

- 215 Units Rs. 6,529.38: Mrs Zubaida Hajyani - N/ADocument2 pages215 Units Rs. 6,529.38: Mrs Zubaida Hajyani - N/ASensationNo ratings yet

- Vavavoom Businss PlanDocument11 pagesVavavoom Businss PlanDrushti DoorputheeNo ratings yet

- 5328100312Document276 pages5328100312Nihit SandNo ratings yet

- Circular Business Model CanvasDocument25 pagesCircular Business Model CanvasLeanne Angel Mendones MayaNo ratings yet

- FIN338 Ch15 LPKDocument90 pagesFIN338 Ch15 LPKjahanzebNo ratings yet

- D. Enhancing Objectivity in Decision-Making. Answer DDocument11 pagesD. Enhancing Objectivity in Decision-Making. Answer DAldrin Frank Valdez100% (1)

- Commentary Tour GuidingDocument1 pageCommentary Tour GuidingMarisol Doroin MendozaNo ratings yet

- HDFC Mutual FundDocument24 pagesHDFC Mutual Fundsachin kumarNo ratings yet

- Organization and Organizational BehaviourDocument9 pagesOrganization and Organizational BehaviourNoor Mohammad ESSOPNo ratings yet

- Rahimafrooz TOC ReportDocument12 pagesRahimafrooz TOC ReportRezuan HasanNo ratings yet

- Harmonic Pattern Trading Strategy PDFDocument10 pagesHarmonic Pattern Trading Strategy PDFyul khaidir malik100% (1)

- ISO 55000 NEW STANDARDS FOR ASSET MANAGEMENT (PDFDrive)Document35 pagesISO 55000 NEW STANDARDS FOR ASSET MANAGEMENT (PDFDrive)Vignesh Bharathi0% (1)

- 2021 - 04 Russian Log Export Ban - VI International ConferenceDocument13 pages2021 - 04 Russian Log Export Ban - VI International ConferenceGlen OKellyNo ratings yet

- Agricultural Extension-The Trainning and Visit SystemDocument100 pagesAgricultural Extension-The Trainning and Visit SystemBenny Duong100% (10)

- Bond and Stock Problem SolutionsDocument3 pagesBond and Stock Problem SolutionsLucas AbudNo ratings yet

- IIC Calendar Activities for Academic YearDocument1 pageIIC Calendar Activities for Academic YearSrushti JainNo ratings yet