You might also like

- India Info Line ICICI DirectDocument6 pagesIndia Info Line ICICI DirectSharad DhariwalNo ratings yet

- PTC India Rating Downgrade and Price Target CutDocument8 pagesPTC India Rating Downgrade and Price Target Cutdrsivaprasad7No ratings yet

- Eclerx Services (Eclser) : Chugging Along..Document6 pagesEclerx Services (Eclser) : Chugging Along..shahavNo ratings yet

- Kamat Hotels (KAMHOT) : Results InlineDocument4 pagesKamat Hotels (KAMHOT) : Results InlinedidwaniasNo ratings yet

- Atul Auto (ATUAUT) : Market Rewards PerformanceDocument5 pagesAtul Auto (ATUAUT) : Market Rewards PerformanceGaurav JainNo ratings yet

- AgilityDocument5 pagesAgilityvijayscaNo ratings yet

- Apollo Tyres ProjectDocument10 pagesApollo Tyres ProjectChetanNo ratings yet

- Financial Analysis of Indigo Airlines From Lender's PerspectiveDocument12 pagesFinancial Analysis of Indigo Airlines From Lender's PerspectiveAnil Kumar Reddy100% (1)

- Dena Bank (DENBAN) : Core Performance Drives ProfitabilityDocument7 pagesDena Bank (DENBAN) : Core Performance Drives ProfitabilitySachin GuptaNo ratings yet

- LIC Housing Finance (LICHF) : Retail Doing Well, Developer Witnesses StressDocument6 pagesLIC Housing Finance (LICHF) : Retail Doing Well, Developer Witnesses Stressdrsivaprasad7No ratings yet

- Maruti Suzuki India LTD (MARUTI) : Uptrend To Continue On Price & MarginsDocument9 pagesMaruti Suzuki India LTD (MARUTI) : Uptrend To Continue On Price & MarginsAmritanshu SinhaNo ratings yet

- Unity Infraprojects Q4FY13 Execution SluggishDocument8 pagesUnity Infraprojects Q4FY13 Execution SluggishShyam RathiNo ratings yet

- Container Corp of India: Valuations Appear To Have Bottomed Out Upgrade To BuyDocument4 pagesContainer Corp of India: Valuations Appear To Have Bottomed Out Upgrade To BuyDoshi VaibhavNo ratings yet

- India Equity Analytics Today: Buy Stock of KPIT TechDocument24 pagesIndia Equity Analytics Today: Buy Stock of KPIT TechNarnolia Securities LimitedNo ratings yet

- Mahindra & Mahindra 2Document6 pagesMahindra & Mahindra 2Ankit SinghalNo ratings yet

- Case Study - Star River Electronic LTDDocument12 pagesCase Study - Star River Electronic LTDNell Mizuno100% (2)

- KPITTECH 03082020160338 KPITInvestorUpdateSEuploadDocument28 pagesKPITTECH 03082020160338 KPITInvestorUpdateSEuploadSreenivasulu Reddy SanamNo ratings yet

- Submitted To Chitkara Business School in Partial Fulfilment of The Requirements For The Award of Degree of Master of Business AdministrationDocument8 pagesSubmitted To Chitkara Business School in Partial Fulfilment of The Requirements For The Award of Degree of Master of Business AdministrationVishu GuptaNo ratings yet

- IDirect IDFC EventUpdate Apr2014Document8 pagesIDirect IDFC EventUpdate Apr2014parry0843No ratings yet

- Comfort Delgro - NomuraDocument28 pagesComfort Delgro - NomuraTerence Seah Pei ChuanNo ratings yet

- Cox & Kings (CNKLIM) : Peak Season of HBR Drives ToplineDocument6 pagesCox & Kings (CNKLIM) : Peak Season of HBR Drives ToplineDarshan MaldeNo ratings yet

- Tech Mahindra: Performance HighlightsDocument11 pagesTech Mahindra: Performance HighlightsAngel BrokingNo ratings yet

- Ashoka BuildconDocument6 pagesAshoka BuildconSaurabh YadavNo ratings yet

- Financial Statement Analysis and Valuation of Ratanpur Steel Re-Rolling Mills Ltd. & GPH Ispat Ltd.Document33 pagesFinancial Statement Analysis and Valuation of Ratanpur Steel Re-Rolling Mills Ltd. & GPH Ispat Ltd.Imtiyaz Khan100% (3)

- IT Sector Update: Demand Improvement Key for UpsideDocument20 pagesIT Sector Update: Demand Improvement Key for UpsidePritam WarudkarNo ratings yet

- DLF IdbiDocument5 pagesDLF IdbivivarshneyNo ratings yet

- Pernod Ricard (India) : Premiumization MantraDocument6 pagesPernod Ricard (India) : Premiumization MantraMayank DixitNo ratings yet

- Reliance Industries Fundamental PDFDocument6 pagesReliance Industries Fundamental PDFsantosh kumariNo ratings yet

- Thermax Limited (THERMA) : Healthy ExecutionDocument6 pagesThermax Limited (THERMA) : Healthy Executionnikhilr05No ratings yet

- Blue Dart Express LTD.: CompanyDocument5 pagesBlue Dart Express LTD.: CompanygirishrajsNo ratings yet

- Fundamental Analysis For AIRASIA BERHAD: 1 - History of Consistently Increasing Earnings, Sales & Cash FlowDocument13 pagesFundamental Analysis For AIRASIA BERHAD: 1 - History of Consistently Increasing Earnings, Sales & Cash FlowPraman ChelseaNo ratings yet

- AnandRathi Relaxo 05oct2012Document13 pagesAnandRathi Relaxo 05oct2012equityanalystinvestorNo ratings yet

- DB Corp: Key Management TakeawaysDocument6 pagesDB Corp: Key Management TakeawaysAngel BrokingNo ratings yet

- Aditya Birla Nuvo: Consolidating Growth BusinessesDocument6 pagesAditya Birla Nuvo: Consolidating Growth BusinessesSouravMalikNo ratings yet

- L&T 4Q Fy 2013Document15 pagesL&T 4Q Fy 2013Angel BrokingNo ratings yet

- Ings BHD RR 3Q FY2012Document6 pagesIngs BHD RR 3Q FY2012Lionel TanNo ratings yet

- NMDC Result UpdatedDocument7 pagesNMDC Result UpdatedAngel BrokingNo ratings yet

- Alok Ind - ICICI DirectDocument9 pagesAlok Ind - ICICI DirectSwamiNo ratings yet

- Bluedart Express (Bludar) : Holding Its Operational Levers Justifies ValuationDocument11 pagesBluedart Express (Bludar) : Holding Its Operational Levers Justifies ValuationDinesh ChoudharyNo ratings yet

- HDFBANK UpdateDocument8 pagesHDFBANK UpdateShyam RathiNo ratings yet

- Suggested Answer - Syl2012 - Jun2014 - Paper - 20 Final Examination: Suggested Answers To QuestionsDocument16 pagesSuggested Answer - Syl2012 - Jun2014 - Paper - 20 Final Examination: Suggested Answers To QuestionsMdAnjum1991No ratings yet

- Simplex Infra, 19th February, 2013Document10 pagesSimplex Infra, 19th February, 2013Angel BrokingNo ratings yet

- Q3 FY12 Results Review - Press Meet: 14 February, 2012Document27 pagesQ3 FY12 Results Review - Press Meet: 14 February, 2012Rishabh GuptaNo ratings yet

- Lucky Cement Final Project Report On: Financial Statement AnalysisDocument25 pagesLucky Cement Final Project Report On: Financial Statement AnalysisPrecious BarbieNo ratings yet

- Financial Reporting and Analysis PDFDocument2 pagesFinancial Reporting and Analysis PDFTushar VatsNo ratings yet

- Financial Statement Analysis ReportDocument47 pagesFinancial Statement Analysis Reportgaurang90% (80)

- Financial Analysis of Next Plc Reveals Profitability and Liquidity StrengthsDocument11 pagesFinancial Analysis of Next Plc Reveals Profitability and Liquidity StrengthsHamza AminNo ratings yet

- Subject: Financial Management.: Project Submitted By: Project Submitted ToDocument17 pagesSubject: Financial Management.: Project Submitted By: Project Submitted ToSwaraj Singh YadavNo ratings yet

- Sant Goben Ratio (FINAL)Document64 pagesSant Goben Ratio (FINAL)Mihir ShahNo ratings yet

- InfoEdge (INFEDG) Maintains Buy Rating & Target Price of ₹950 After Mixed Q2 ResultsDocument8 pagesInfoEdge (INFEDG) Maintains Buy Rating & Target Price of ₹950 After Mixed Q2 ResultsJNNo ratings yet

- Future Retail (PANRET) : Higher-Than-Expected Interest Cost Dents PATDocument8 pagesFuture Retail (PANRET) : Higher-Than-Expected Interest Cost Dents PATdrsivaprasad7No ratings yet

- UAE Real Estate Sector Update October 2008Document40 pagesUAE Real Estate Sector Update October 2008Mustafa ChaudhryNo ratings yet

- Dishman 2QFY2013RUDocument10 pagesDishman 2QFY2013RUAngel BrokingNo ratings yet

- Corporate Finance Report AnalysisDocument64 pagesCorporate Finance Report AnalysisabhdonNo ratings yet

- Performance Highlights: Company Update - AutomobileDocument13 pagesPerformance Highlights: Company Update - AutomobileZacharia VincentNo ratings yet

- Ivrcl LTD (Ivrinf) : Improvement Only If Asset Monetisation MaterialisesDocument7 pagesIvrcl LTD (Ivrinf) : Improvement Only If Asset Monetisation Materialisesdrsivaprasad7No ratings yet

- Press Meet Q4 FY12Document30 pagesPress Meet Q4 FY12Chintan KotadiaNo ratings yet

- Jyoti Structures (JYOSTR) : When Interest Burden Outweighs AllDocument10 pagesJyoti Structures (JYOSTR) : When Interest Burden Outweighs Allnit111100% (1)

- List of the Most Important Financial Ratios: Formulas and Calculation Examples Defined for Different Types of Key Financial RatiosFrom EverandList of the Most Important Financial Ratios: Formulas and Calculation Examples Defined for Different Types of Key Financial RatiosNo ratings yet

- Indigo PaperDocument75 pagesIndigo Papernxoxoxrx xxxNo ratings yet

- Functional Specialization of Members of Stock ExchangeDocument14 pagesFunctional Specialization of Members of Stock ExchangeTaresh Baru100% (1)

- Wells Fargo Clear Access BankingDocument5 pagesWells Fargo Clear Access BankingМоника ПетровичNo ratings yet

- IlliquidDocument3 pagesIlliquidyến lêNo ratings yet

- Individual - Joint Account - HAO - FormDocument6 pagesIndividual - Joint Account - HAO - FormRABIU OLAMILEKAN ABAYOMINo ratings yet

- HomeCredit Loan Payment ScheduleDocument2 pagesHomeCredit Loan Payment ScheduleKylyn JynNo ratings yet

- Concept Map 2Document8 pagesConcept Map 2mike raninNo ratings yet

- Finweek - September 10, 2015Document48 pagesFinweek - September 10, 2015mariusNo ratings yet

- Week 3 Tutorial SolutionsDocument31 pagesWeek 3 Tutorial SolutionsalexandraNo ratings yet

- What Is Globalization? - Definition, Effects & Examples: VideoDocument4 pagesWhat Is Globalization? - Definition, Effects & Examples: VideoPew Collado PlaresNo ratings yet

- Siddhartha Institute MBA II Semester II Internal ExamDocument2 pagesSiddhartha Institute MBA II Semester II Internal ExamRaja Shekhar ChinnaNo ratings yet

- STD X CH 3 Money and Credit Notes (21-22)Document6 pagesSTD X CH 3 Money and Credit Notes (21-22)Dhwani ShahNo ratings yet

- Vethathiri - WisdomDocument40 pagesVethathiri - WisdomProf. Madhavan100% (2)

- Daimler Q3 2011 Interim ReportDocument38 pagesDaimler Q3 2011 Interim ReportSaiful_Azri_1450No ratings yet

- Iscal EARDocument311 pagesIscal EARDjalma MoreiraNo ratings yet

- Business Purchase and MergerDocument47 pagesBusiness Purchase and Mergerdc1901078No ratings yet

- NSE Yield Curve and Implied Yields ReportDocument2 pagesNSE Yield Curve and Implied Yields ReportCarl RossNo ratings yet

- Black Book On Direct Tax EffectDocument49 pagesBlack Book On Direct Tax Effectshiakhrustam621No ratings yet

- BLKL 5 Banking Industry and StructureDocument21 pagesBLKL 5 Banking Industry and Structurelinda kartikaNo ratings yet

- Sap Fico TutorialDocument29 pagesSap Fico Tutorialkmurali321No ratings yet

- The Noble Group: Brienne Bowen, Emily Phipps, Adam Foley, Jeff Schroeder, Michael MalloyDocument12 pagesThe Noble Group: Brienne Bowen, Emily Phipps, Adam Foley, Jeff Schroeder, Michael MalloyKshitishNo ratings yet

- CCMS ActivityDocument3 pagesCCMS ActivityRochelle LagmayNo ratings yet

- BIAN Landscape4.0Document1 pageBIAN Landscape4.0Arie Wibowo SutiarsoNo ratings yet

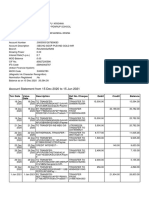

- Account statement for Mr. SAVARAPU KRISHNA from Dec 2020 to Jun 2021Document9 pagesAccount statement for Mr. SAVARAPU KRISHNA from Dec 2020 to Jun 2021SRINIVASARAO JONNALANo ratings yet

- The Financial StabilityDocument10 pagesThe Financial Stabilityhaque163No ratings yet

- Residential Status and Income Tax ImplicationsDocument6 pagesResidential Status and Income Tax ImplicationsmamtakariraNo ratings yet

- Myanmar Stamp ActDocument271 pagesMyanmar Stamp ActKaung Khant WanaNo ratings yet

- Review - Udayana - Baiq Sonia Toin - GBDocument9 pagesReview - Udayana - Baiq Sonia Toin - GBBaiq sonia ToinNo ratings yet

- Meezan Bank - Report 2Document87 pagesMeezan Bank - Report 2SaadatNo ratings yet

- Safe Shop Plan - 2022 JuneDocument40 pagesSafe Shop Plan - 2022 Juneshinu pokemon masterNo ratings yet