You might also like

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (120)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- Victor Bulmer-Thomas The Political Economy of Central AmericaDocument441 pagesVictor Bulmer-Thomas The Political Economy of Central AmericagabrielescolanNo ratings yet

- Dizon V Commanding GeneralDocument3 pagesDizon V Commanding GeneralKirby Hipolito100% (1)

- Wodrow Wilson and The Birth NationDocument31 pagesWodrow Wilson and The Birth NationAraceli Jaramillo CovarrubiasNo ratings yet

- Gonzales vs. COMELEC - DigestDocument2 pagesGonzales vs. COMELEC - DigestStruggler 369No ratings yet

- Thesis Unesco Cultural PolicyDocument288 pagesThesis Unesco Cultural PolicyFernando UribeNo ratings yet

- Boundary Displacement - Area Studies and International Studies During and After The Cold War - Bruce Cumings - 29-01 (1997) PDFDocument26 pagesBoundary Displacement - Area Studies and International Studies During and After The Cold War - Bruce Cumings - 29-01 (1997) PDFRash YuuNo ratings yet

- #Technical CommentaryDocument15 pages#Technical CommentaryMonica GaudetNo ratings yet

- Technical #CommentaryDocument21 pagesTechnical #CommentaryMonica GaudetNo ratings yet

- U.S. May Have Already Fallen Over The CliffDocument1 pageU.S. May Have Already Fallen Over The CliffMonica GaudetNo ratings yet

- #U.S. May Have Already Fallen Over The #CliffDocument1 page#U.S. May Have Already Fallen Over The #CliffMonica GaudetNo ratings yet

- U.S. May Have Already Fallen Over The/#cliffDocument1 pageU.S. May Have Already Fallen Over The/#cliffMonica GaudetNo ratings yet

- The Chapman Report: Charts and Commentary by David ChapmanDocument22 pagesThe Chapman Report: Charts and Commentary by David ChapmanMonica GaudetNo ratings yet

- The Chapman Report: Charts and Commentary by David ChapmanDocument25 pagesThe Chapman Report: Charts and Commentary by David ChapmanMonica GaudetNo ratings yet

- Technical Commentary - December 3, 2012Document22 pagesTechnical Commentary - December 3, 2012Monica GaudetNo ratings yet

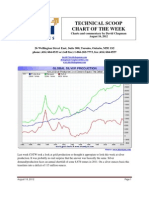

- Technical Scoop Chart of The Week: Charts and Commentary by David ChapmanDocument5 pagesTechnical Scoop Chart of The Week: Charts and Commentary by David ChapmanMonica GaudetNo ratings yet

- Bayer Combined Management Report 2012Document110 pagesBayer Combined Management Report 2012brindushaNo ratings yet

- Most Important MCQs About Constitutions of The World PDFDocument6 pagesMost Important MCQs About Constitutions of The World PDFArsalan SheikhNo ratings yet

- The External Financial Restricton. Esteban Pérez CaldenteyDocument16 pagesThe External Financial Restricton. Esteban Pérez CaldenteyAlejandro VieiraNo ratings yet

- Sign-Up Sheet For Case BriefsDocument3 pagesSign-Up Sheet For Case Briefsjaja001No ratings yet

- The Future in Question - Fernando CoronilDocument39 pagesThe Future in Question - Fernando CoronilCarmen Ilizarbe100% (1)

- 2015 2020 CTRM Market OutlookDocument17 pages2015 2020 CTRM Market OutlookCTRM CenterNo ratings yet

- PLACES Act Bill TextDocument3 pagesPLACES Act Bill TextTom UdallNo ratings yet

- US Presidents ListDocument2 pagesUS Presidents ListkenechidukorNo ratings yet

- Annotated BibliographyDocument10 pagesAnnotated Bibliographyserar802No ratings yet

- The Jere Beasley Report, Jan. 2009Document52 pagesThe Jere Beasley Report, Jan. 2009Beasley AllenNo ratings yet

- What Isn't For SaleDocument5 pagesWhat Isn't For SaleahcalabreseNo ratings yet

- ITC FoodsDocument11 pagesITC FoodsDixon MirandaNo ratings yet

- Book Review: Mine by Sally PartridgeDocument1 pageBook Review: Mine by Sally PartridgeAnna StroudNo ratings yet

- A History of The Globlal Economy, Joerg Baten NDocument14 pagesA History of The Globlal Economy, Joerg Baten NGael JiménezNo ratings yet

- The War of Brothers That Changed The WorldDocument8 pagesThe War of Brothers That Changed The WorldEsih WinangsihNo ratings yet

- Transnational Religious NetworksDocument12 pagesTransnational Religious NetworksChi TrầnNo ratings yet

- Minimum Stipend USANACDOM21Document12 pagesMinimum Stipend USANACDOM21Nikiya Anton BetteyNo ratings yet

- The Coming World Government - Oct2017 - Master FileDocument167 pagesThe Coming World Government - Oct2017 - Master FileGiuseppe BartolomeoNo ratings yet

- Works Cited FinalDocument13 pagesWorks Cited Finalapi-207681978No ratings yet

- We The People 11th Edition Ginsberg Test BankDocument25 pagesWe The People 11th Edition Ginsberg Test BankLaurenBateskqtre100% (16)

- Indian Consumer - Goldman Sachs ReportDocument22 pagesIndian Consumer - Goldman Sachs Reporthvsboua100% (1)

- FX MKT Insights Jun2010 Rosenberg PDFDocument27 pagesFX MKT Insights Jun2010 Rosenberg PDFsuksesNo ratings yet

- Vassar Chronicle, November 2013Document20 pagesVassar Chronicle, November 2013The Vassar ChronicleNo ratings yet

- 1987 DBQ - Compromise of 1850Document7 pages1987 DBQ - Compromise of 1850psppunk7182No ratings yet