You might also like

- Computerised Payroll Practice Set Using MYOB AccountRight: Australian EditionFrom EverandComputerised Payroll Practice Set Using MYOB AccountRight: Australian EditionNo ratings yet

- Chapter 3 Financial Model ExcelDocument11 pagesChapter 3 Financial Model Excelzzduble1No ratings yet

- Activity Based Budget Spreadsheet TemplateDocument15 pagesActivity Based Budget Spreadsheet TemplateAnass HamdouneNo ratings yet

- 1 - Blank Financial AppendixDocument57 pages1 - Blank Financial AppendixKingNo ratings yet

- Certificate of Creditable Tax Withheld at SourceDocument2 pagesCertificate of Creditable Tax Withheld at SourceMaricar Lelaine SecretarioNo ratings yet

- Analysis of Beta Corporation's 1991 Cash Flow StatementDocument14 pagesAnalysis of Beta Corporation's 1991 Cash Flow Statementshahin selkarNo ratings yet

- Accounting Excel Reports - Report Generalledger ExcelDocument36 pagesAccounting Excel Reports - Report Generalledger ExcelMark Ceddrick MioleNo ratings yet

- 2019 Tax Advisors Update 11.14.19 PDFDocument326 pages2019 Tax Advisors Update 11.14.19 PDFD100% (1)

- FD-Schedule C-Profit or Loss From Business (Sole Prop)Document2 pagesFD-Schedule C-Profit or Loss From Business (Sole Prop)Anthony Juice Gaston BeyNo ratings yet

- Projected Profit and Cash FlowDocument27 pagesProjected Profit and Cash FlowAprian ImmanuelNo ratings yet

- Byrd and Chens Canadian Tax Principles 2012 2013 Edition Canadian 1st Edition Byrd Solutions ManualDocument9 pagesByrd and Chens Canadian Tax Principles 2012 2013 Edition Canadian 1st Edition Byrd Solutions Manuallemon787100% (5)

- Chart of Accounts 1670433717Document22 pagesChart of Accounts 1670433717Ahmed ElwaseefNo ratings yet

- 2018-Income-Statement Copy-2Document9 pages2018-Income-Statement Copy-2api-464285260No ratings yet

- Chapter 4Document6 pagesChapter 4Ashanti T Swan0% (1)

- Pay As You Go (Payg) WithholdingDocument70 pagesPay As You Go (Payg) WithholdingliamNo ratings yet

- Balance SheetDocument4 pagesBalance SheetSiddharth KaliaNo ratings yet

- Tax Credits for Child Care and Education ExpensesDocument17 pagesTax Credits for Child Care and Education ExpensesKeti AnevskiNo ratings yet

- Profit and Loss Statement TemplateDocument8 pagesProfit and Loss Statement TemplateJerarudo BoknoyNo ratings yet

- Worked Example Financial StatementDocument2 pagesWorked Example Financial StatementNayaz EmamaulleeNo ratings yet

- Former Mayor Bill White's 2009 Tax ReturnDocument43 pagesFormer Mayor Bill White's 2009 Tax ReturnTexas WatchdogNo ratings yet

- Gene Locke Tax Return, 2006Document25 pagesGene Locke Tax Return, 2006Lee Ann O'NealNo ratings yet

- ACC 330 Final Project Two Tax Planning Template - 2020Document3 pagesACC 330 Final Project Two Tax Planning Template - 2020BREANNA JOHNSONNo ratings yet

- Income StatementDocument26 pagesIncome StatementRashad MallakNo ratings yet

- The Polks Tax CalculationDocument8 pagesThe Polks Tax CalculationhuytrinhxNo ratings yet

- Dashboard: Profit & Loss StatementDocument3 pagesDashboard: Profit & Loss StatementKhairie RahimNo ratings yet

- Introduction to Federal Taxation in CanadaDocument40 pagesIntroduction to Federal Taxation in CanadaDonna So100% (2)

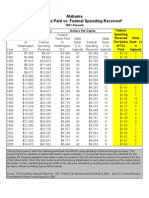

- Federal Taxes Paid Vs Federal Spending Received by States, 1981-2005Document51 pagesFederal Taxes Paid Vs Federal Spending Received by States, 1981-2005Javier Arvelo-Cruz-SantanaNo ratings yet

- Physical properties of HC gas streamDocument2 pagesPhysical properties of HC gas streammahi_kotaNo ratings yet

- Estimated Grade Calculator for Accounting CourseDocument7 pagesEstimated Grade Calculator for Accounting Course037boyNo ratings yet

- ITR AssignmentDocument8 pagesITR AssignmentEkta VermaNo ratings yet

- FR - MID - TERM - TEST - 2020 CPA Financial ReportingDocument13 pagesFR - MID - TERM - TEST - 2020 CPA Financial ReportingH M Yasir MuyidNo ratings yet

- PL Appropriation AcDocument6 pagesPL Appropriation AcShivangi Aggarwal100% (1)

- Indirect MethodDocument34 pagesIndirect MethodHacker SKNo ratings yet

- f1040x PDFDocument2 pagesf1040x PDFAlexNo ratings yet

- 12.2 - Cash Flows From Operating Activities: Treatment of Interest ReceivedDocument9 pages12.2 - Cash Flows From Operating Activities: Treatment of Interest ReceivedSrikiran RajNo ratings yet

- Amended U.S. Individual Income Tax ReturnDocument2 pagesAmended U.S. Individual Income Tax ReturnJohnNo ratings yet

- Amended 1040 Tax Form ExplainedDocument2 pagesAmended 1040 Tax Form Explainedgolcha_edu532No ratings yet

- Irs 990-Ez 2007Document3 pagesIrs 990-Ez 2007api-18678301No ratings yet

- Homework ES 2 Solution ACCT 553Document5 pagesHomework ES 2 Solution ACCT 553Mohammad IslamNo ratings yet

- Amended U.S. Individual Income Tax Return: Use Part III On The Back To Explain Any ChangesDocument2 pagesAmended U.S. Individual Income Tax Return: Use Part III On The Back To Explain Any ChangesEri TakataNo ratings yet

- Specimen Examen F3 AccaDocument21 pagesSpecimen Examen F3 AccaGNo ratings yet

- f3 Specimen j14 PDFDocument21 pagesf3 Specimen j14 PDFBestNo ratings yet

- F3 Specimen Exam 2014 PDFDocument21 pagesF3 Specimen Exam 2014 PDFgrrrklNo ratings yet

- Computation of Adjusted Profit For Self EmployedDocument8 pagesComputation of Adjusted Profit For Self EmployedCindyNo ratings yet

- Chapter 11 - Computation of Taxable Income and TaxDocument22 pagesChapter 11 - Computation of Taxable Income and TaxMichelle Tan100% (1)

- Partner's Instructions For Schedule K-1 (Form 1065)Document15 pagesPartner's Instructions For Schedule K-1 (Form 1065)Mario LaflammeNo ratings yet

- Untitled PDFDocument2 pagesUntitled PDFjenny abbottNo ratings yet

- Please Review The Updated Information Below.: For Begins After This CoversheetDocument6 pagesPlease Review The Updated Information Below.: For Begins After This CoversheetAshutosh Singh ParmarNo ratings yet

- Accounting 4Document8 pagesAccounting 4syopiNo ratings yet

- Tax Audit Issues and ApplicabilityDocument20 pagesTax Audit Issues and ApplicabilityJigar MehtaNo ratings yet

- Financial Statements SummaryDocument53 pagesFinancial Statements Summaryrachealll100% (1)

- 3 Partnership AccountsDocument93 pages3 Partnership AccountsCA K D Purkayastha100% (1)

- 2013 Form IL-1040: Personal InformationDocument2 pages2013 Form IL-1040: Personal Informationvimal_pro222-scribdNo ratings yet

- Amended Tax Return Form 1040X ExplainedDocument2 pagesAmended Tax Return Form 1040X ExplainedKel TranNo ratings yet

- CPA Regulation (Reg) Notes 2013Document7 pagesCPA Regulation (Reg) Notes 2013amichalek0820100% (3)

- FTG Irs Form 990-Ez 2008Document12 pagesFTG Irs Form 990-Ez 2008L. A. PatersonNo ratings yet

- Section24-Prior Year Salary OverpaymentsDocument8 pagesSection24-Prior Year Salary OverpaymentsP45 TesterNo ratings yet

- Interest Charge On DISC-Related Deferred Tax Liability: Sign HereDocument2 pagesInterest Charge On DISC-Related Deferred Tax Liability: Sign HereInternational Tax Magazine; David Greenberg PhD, MSA, EA, CPA; Tax Group International; 646-705-2910No ratings yet

- United Council Form 990 2010Document18 pagesUnited Council Form 990 2010Signe BrewsterNo ratings yet

- Instructions For Filling The Tax Calculator For Financial Year 2017-18Document2 pagesInstructions For Filling The Tax Calculator For Financial Year 2017-18SubramanyaNo ratings yet

- Premarket OpeningBell ICICI 15.12.16Document8 pagesPremarket OpeningBell ICICI 15.12.16Rajasekhar Reddy AnekalluNo ratings yet

- Premarket OpeningBell ICICI 21.12.16Document8 pagesPremarket OpeningBell ICICI 21.12.16Rajasekhar Reddy AnekalluNo ratings yet

- Premarket Technical&Derivative Ashika 16.12.16Document4 pagesPremarket Technical&Derivative Ashika 16.12.16Rajasekhar Reddy AnekalluNo ratings yet

- Premarket MorningGlance SPA 15.12.16Document3 pagesPremarket MorningGlance SPA 15.12.16Rajasekhar Reddy AnekalluNo ratings yet

- Premarket CurrencyDaily ICICI 21.12.16Document4 pagesPremarket CurrencyDaily ICICI 21.12.16Rajasekhar Reddy AnekalluNo ratings yet

- Premarket CurrencyDaily ICICI 20.12.16Document4 pagesPremarket CurrencyDaily ICICI 20.12.16Rajasekhar Reddy AnekalluNo ratings yet

- Premarket CurrencyDaily ICICI 15.12.16Document4 pagesPremarket CurrencyDaily ICICI 15.12.16Rajasekhar Reddy AnekalluNo ratings yet

- Premarket MarketOutlook Angel 15.12.16Document14 pagesPremarket MarketOutlook Angel 15.12.16Rajasekhar Reddy AnekalluNo ratings yet

- Premarket Technical&Derivative Angel 15.12.16Document5 pagesPremarket Technical&Derivative Angel 15.12.16Rajasekhar Reddy AnekalluNo ratings yet

- Morning Report: Equity Latest % CHG NSE Sect. Indices Latest % CHG Nifty GainersDocument6 pagesMorning Report: Equity Latest % CHG NSE Sect. Indices Latest % CHG Nifty GainersRajasekhar Reddy AnekalluNo ratings yet

- Premarket MarketOutlook Motilal 20.12.16Document5 pagesPremarket MarketOutlook Motilal 20.12.16Rajasekhar Reddy AnekalluNo ratings yet

- Premarket WakeUpCall Wallfort 21.12.16Document2 pagesPremarket WakeUpCall Wallfort 21.12.16Rajasekhar Reddy AnekalluNo ratings yet

- Premarket MorningReport Ashika 15.12.16Document6 pagesPremarket MorningReport Ashika 15.12.16Rajasekhar Reddy AnekalluNo ratings yet

- Premarket WakeUpCall Wallfort 20.12.16Document2 pagesPremarket WakeUpCall Wallfort 20.12.16Rajasekhar Reddy AnekalluNo ratings yet

- Premarket MorningReport Dynamic 20.12.16Document7 pagesPremarket MorningReport Dynamic 20.12.16Rajasekhar Reddy AnekalluNo ratings yet

- Premarket MorningGlance SPA 20.12.16Document3 pagesPremarket MorningGlance SPA 20.12.16Rajasekhar Reddy AnekalluNo ratings yet

- Premarket MarketOutlook Angel 20.12.16Document14 pagesPremarket MarketOutlook Angel 20.12.16Rajasekhar Reddy AnekalluNo ratings yet

- Technical Derivatives Report SummaryDocument5 pagesTechnical Derivatives Report SummaryRajasekhar Reddy AnekalluNo ratings yet

- Premarket MarketOutlook Motilal 19.12.16Document4 pagesPremarket MarketOutlook Motilal 19.12.16Rajasekhar Reddy AnekalluNo ratings yet

- Premarket MorningReport Dynamic 19.12.16Document7 pagesPremarket MorningReport Dynamic 19.12.16Rajasekhar Reddy AnekalluNo ratings yet

- Premarket MorningReport Ashika 21.12.16Document6 pagesPremarket MorningReport Ashika 21.12.16Rajasekhar Reddy AnekalluNo ratings yet

- Premarket MorningGlance SPA 21.12.16Document3 pagesPremarket MorningGlance SPA 21.12.16Rajasekhar Reddy AnekalluNo ratings yet

- Premarket MorningReport Dynamic 21.12.16Document7 pagesPremarket MorningReport Dynamic 21.12.16Rajasekhar Reddy AnekalluNo ratings yet

- Premarket MarketOutlook Angel 19.12.16Document14 pagesPremarket MarketOutlook Angel 19.12.16Rajasekhar Reddy AnekalluNo ratings yet

- Premarket MarketOutlook Angel 9.12.16Document11 pagesPremarket MarketOutlook Angel 9.12.16Rajasekhar Reddy AnekalluNo ratings yet

- Premarket CurrencyDaily ICICI 19.12.16Document4 pagesPremarket CurrencyDaily ICICI 19.12.16Rajasekhar Reddy AnekalluNo ratings yet

- US$ INR Currency Futures OutlookDocument4 pagesUS$ INR Currency Futures OutlookRajasekhar Reddy AnekalluNo ratings yet

- Techno Funda Pick Techno Funda Pick: R Hal Research AnalystsDocument10 pagesTechno Funda Pick Techno Funda Pick: R Hal Research AnalystsRajasekhar Reddy AnekalluNo ratings yet

- Premarket OpeningBell ICICI 09.12.16Document8 pagesPremarket OpeningBell ICICI 09.12.16Rajasekhar Reddy AnekalluNo ratings yet

- Monthly Call: Apollo TyresDocument4 pagesMonthly Call: Apollo TyresRajasekhar Reddy AnekalluNo ratings yet

- Godrej Meridien Gurgaon Sector 106 BrochureDocument59 pagesGodrej Meridien Gurgaon Sector 106 BrochureGodrej MeridienNo ratings yet

- Intern Report BBA PUDocument34 pagesIntern Report BBA PUBabita ChhetriNo ratings yet

- 2 0 1 1 C A S E S PropertyDocument36 pages2 0 1 1 C A S E S PropertyIcee GenioNo ratings yet

- Amortization On A Simple Interest MortgageDocument470 pagesAmortization On A Simple Interest Mortgagesaxophonist42No ratings yet

- Preface To The Third Edition: Life Contingencies by C.W. Jordan, Our Text Has Become The Only OneDocument59 pagesPreface To The Third Edition: Life Contingencies by C.W. Jordan, Our Text Has Become The Only OneAelin IsmailovaNo ratings yet

- August 9, 2013 Federal RICO Complaint To Add 2260 Defendant Ryder Ray Sexual Exploitation ChildDocument193 pagesAugust 9, 2013 Federal RICO Complaint To Add 2260 Defendant Ryder Ray Sexual Exploitation Childrealestatelawyer101No ratings yet

- Activity A - Introduction To Engineering EconomyDocument2 pagesActivity A - Introduction To Engineering EconomySofia MonteroNo ratings yet

- Ra 8291 - Gsis LawDocument15 pagesRa 8291 - Gsis LawjoyeduardoNo ratings yet

- Home Loans in India - A Complete GuideDocument84 pagesHome Loans in India - A Complete GuidePrathmesh AmbulkarNo ratings yet

- Phil Savings Bank vs. ManalacDocument13 pagesPhil Savings Bank vs. ManalacSherwin Anoba CabutijaNo ratings yet

- Mortel V KasscoDocument1 pageMortel V KasscoMichelle BernardoNo ratings yet

- Allahabad Bank Was Founded by Group of Europeans On April 24Document34 pagesAllahabad Bank Was Founded by Group of Europeans On April 24Mahendra KushwahaNo ratings yet

- LEAD BATCH 2 - ERG-TAX 1 Estate Tax - George James Comprehensive Problem-AnsDocument2 pagesLEAD BATCH 2 - ERG-TAX 1 Estate Tax - George James Comprehensive Problem-AnsJims Leñar CezarNo ratings yet

- Owais Zahid - Nov 22Document6 pagesOwais Zahid - Nov 22Owais ZahidNo ratings yet

- Singapore Property Weekly Issue 93 To 126 PDFDocument436 pagesSingapore Property Weekly Issue 93 To 126 PDFPrasanth NairNo ratings yet

- Loan Documentation IobDocument18 pagesLoan Documentation IobVenkatesanSelvarajan0% (1)

- The Savings and Loan Crisis and Its Relationship To BankingDocument22 pagesThe Savings and Loan Crisis and Its Relationship To Bankingmanepalli vamsiNo ratings yet

- PART - 5 - Precalculus Fifth Edition Mathematics For CalculusDocument182 pagesPART - 5 - Precalculus Fifth Edition Mathematics For CalculusJed Lavu0% (1)

- 2017 (GR No 202364, Arturo Calubad V Ricarcen Development Corporation) PDFDocument15 pages2017 (GR No 202364, Arturo Calubad V Ricarcen Development Corporation) PDFFrance SanchezNo ratings yet

- Investigate Three Occupations: Instruction Sheet: Posted On CanvasDocument5 pagesInvestigate Three Occupations: Instruction Sheet: Posted On Canvasapi-521677138No ratings yet

- Upholds validity of consignation of loan payment when creditor is unknownDocument8 pagesUpholds validity of consignation of loan payment when creditor is unknownJm CruzNo ratings yet

- 3 C's of CreditDocument45 pages3 C's of Creditsushant1903No ratings yet

- Chap 014Document67 pagesChap 014Nitesh Agrawal100% (2)

- Bachrach V Talisay SilayDocument1 pageBachrach V Talisay SilayalexNo ratings yet

- Mi Investment Outlook Ce enDocument17 pagesMi Investment Outlook Ce enCrypto JiznNo ratings yet

- ACC 240 CH - 17 - SM - 9eDocument17 pagesACC 240 CH - 17 - SM - 9eashandron4everNo ratings yet

- Chapter 5 Annual Cash Flow AnalysisDocument54 pagesChapter 5 Annual Cash Flow AnalysisShudipto PodderNo ratings yet

- Business Mathematics: For LearnersDocument13 pagesBusiness Mathematics: For LearnersJet Rollorata BacangNo ratings yet

- Financial crises caused by cross-border investment flows not misbehaviorDocument4 pagesFinancial crises caused by cross-border investment flows not misbehavioralpar7377No ratings yet

- Taxation of Federal ObligationsDocument26 pagesTaxation of Federal ObligationsTRISTARUSANo ratings yet