You might also like

- Get a Second Opinion before You Sign: What to do when the Bank says 'No' ? How to survive and thrive with Private Lending.From EverandGet a Second Opinion before You Sign: What to do when the Bank says 'No' ? How to survive and thrive with Private Lending.No ratings yet

- Where Credit is Due: Bringing Equity to Credit and Housing After the Market MeltdownFrom EverandWhere Credit is Due: Bringing Equity to Credit and Housing After the Market MeltdownNo ratings yet

- Defeat Foreclosure: Save Your House,Your Credit and Your Rights.From EverandDefeat Foreclosure: Save Your House,Your Credit and Your Rights.No ratings yet

- Loan Modifications, Foreclosures and Saving Your Home: With an Affordable Loan Modification AgreementFrom EverandLoan Modifications, Foreclosures and Saving Your Home: With an Affordable Loan Modification AgreementNo ratings yet

- American Foreclosure: Everything U Need to Know About Preventing and BuyingFrom EverandAmerican Foreclosure: Everything U Need to Know About Preventing and BuyingNo ratings yet

- Construction Liens for the Pacific Northwest Alaska Idaho Oregon Washington Federal Public Works: A PrimerFrom EverandConstruction Liens for the Pacific Northwest Alaska Idaho Oregon Washington Federal Public Works: A PrimerNo ratings yet

- Real Estate Transactions and Foreclosure Control—A Home Mortgage Reference Handbook: The Causes and Remedies of Foreclosure PainsFrom EverandReal Estate Transactions and Foreclosure Control—A Home Mortgage Reference Handbook: The Causes and Remedies of Foreclosure PainsNo ratings yet

- Be the Bank: "When the Bank Says No or Moves Too Slow" You Are the Bank!From EverandBe the Bank: "When the Bank Says No or Moves Too Slow" You Are the Bank!No ratings yet

- Saving Main Street and Its Retailers: Protecting Your Town, Jobs and Small Businesses from GlobalizationFrom EverandSaving Main Street and Its Retailers: Protecting Your Town, Jobs and Small Businesses from GlobalizationNo ratings yet

- Real Estate Escapes: True tales of getting out of contracts, leases, prosecutions and legal liabilityFrom EverandReal Estate Escapes: True tales of getting out of contracts, leases, prosecutions and legal liabilityNo ratings yet

- Beating Banks At Their Own Game: Don't fear Big Brother; fear Big BanksFrom EverandBeating Banks At Their Own Game: Don't fear Big Brother; fear Big BanksNo ratings yet

- The Foreclosure Workbook: The Complete Guide to Understanding Foreclosure and Saving Your HomeFrom EverandThe Foreclosure Workbook: The Complete Guide to Understanding Foreclosure and Saving Your HomeNo ratings yet

- Constitution of the State of Minnesota — 1876 VersionFrom EverandConstitution of the State of Minnesota — 1876 VersionNo ratings yet

- Our Virtuous Republic: The Forgotten Clause in the American Social ContractFrom EverandOur Virtuous Republic: The Forgotten Clause in the American Social ContractNo ratings yet

- Naked Guide to Bonds: What You Need to Know -- Stripped Down to the Bare EssentialsFrom EverandNaked Guide to Bonds: What You Need to Know -- Stripped Down to the Bare EssentialsNo ratings yet

- Voluntary Liens ReportDocument6 pagesVoluntary Liens ReportMortgage Compliance Investigators100% (1)

- Failure to Comply: We Fought a Wall Street Giant and Won: We Fought a Wall Street Giant and WonFrom EverandFailure to Comply: We Fought a Wall Street Giant and Won: We Fought a Wall Street Giant and WonNo ratings yet

- From The Memory Of The Collector - Or "Calling The Priest To The Sinner"From EverandFrom The Memory Of The Collector - Or "Calling The Priest To The Sinner"No ratings yet

- Quantum of Justice - The Fraud of Foreclosure and the Illegal Securitization of Notes by Wall Street: The Fraud of Foreclosure and the Illegal Securitization of Notes by Wall StreetFrom EverandQuantum of Justice - The Fraud of Foreclosure and the Illegal Securitization of Notes by Wall Street: The Fraud of Foreclosure and the Illegal Securitization of Notes by Wall StreetNo ratings yet

- Free & Clear, Standing & Quiet Title: 11 Possible Ways to Get Rid of Your MortgageFrom EverandFree & Clear, Standing & Quiet Title: 11 Possible Ways to Get Rid of Your MortgageRating: 2 out of 5 stars2/5 (3)

- The Ultimate Guide to Avoiding Eviction for Tenants: Leases, Rent, Registration, Verification & RightsFrom EverandThe Ultimate Guide to Avoiding Eviction for Tenants: Leases, Rent, Registration, Verification & RightsNo ratings yet

- Responsibility Assignment Matrix A Complete Guide - 2020 EditionFrom EverandResponsibility Assignment Matrix A Complete Guide - 2020 EditionNo ratings yet

- An Instructional Guide Short Sales And Foreclosed Properties For The Experienced The Novice And The Merely LazyFrom EverandAn Instructional Guide Short Sales And Foreclosed Properties For The Experienced The Novice And The Merely LazyNo ratings yet

- Treasury Operations In Turkey and Contemporary Sovereign Treasury ManagementFrom EverandTreasury Operations In Turkey and Contemporary Sovereign Treasury ManagementNo ratings yet

- 10-10-08 A) AP - Bank of America Issues Nationwide Moratorium On Foreclosures, B) CNBC - Foreclosure PrimerDocument12 pages10-10-08 A) AP - Bank of America Issues Nationwide Moratorium On Foreclosures, B) CNBC - Foreclosure PrimerHuman Rights Alert - NGO (RA)No ratings yet

- The Mortgage Loan Process: The Good, Bad, and Ugly but the Real - A Humorous, Sarcastic Walk-Through of a Dry, Boring Topic for BeginnersFrom EverandThe Mortgage Loan Process: The Good, Bad, and Ugly but the Real - A Humorous, Sarcastic Walk-Through of a Dry, Boring Topic for BeginnersNo ratings yet

- A Guide to Ethical Practices in the United States Tax IndustryFrom EverandA Guide to Ethical Practices in the United States Tax IndustryNo ratings yet

- Teil 12 Foreclosure FraudDocument44 pagesTeil 12 Foreclosure FraudNathan Beam100% (1)

- Bailee Letter TermsDocument3 pagesBailee Letter TermsHelpin HandNo ratings yet

- The Story Behind the Mortgage and Housing Meltdown: The Legacy of GreedFrom EverandThe Story Behind the Mortgage and Housing Meltdown: The Legacy of GreedNo ratings yet

- Lawfully Yours: The Realm of Business, Government and LawFrom EverandLawfully Yours: The Realm of Business, Government and LawNo ratings yet

- Lender Processing Services' DOCX Document Fabrication Price SheetDocument3 pagesLender Processing Services' DOCX Document Fabrication Price SheetForeclosure Fraud100% (2)

- The Complete Guide to Preventing Foreclosure on Your Home: Legal Secrets to Beat Foreclosure and Protect Your Home NOWFrom EverandThe Complete Guide to Preventing Foreclosure on Your Home: Legal Secrets to Beat Foreclosure and Protect Your Home NOWRating: 4.5 out of 5 stars4.5/5 (4)

- How to Use a Short Sale to Stop Home Foreclosure and Protect Your FinancesFrom EverandHow to Use a Short Sale to Stop Home Foreclosure and Protect Your FinancesNo ratings yet

- Mortgage Compliance Investigators - Mortgage Fraud InvestigationDocument16 pagesMortgage Compliance Investigators - Mortgage Fraud InvestigationBilly Bowles100% (3)

- Mortgage Compliance Investigators - Chain of Title AnalysisDocument31 pagesMortgage Compliance Investigators - Chain of Title AnalysisBilly BowlesNo ratings yet

- What Will A Trustee's Deed Tell?Document3 pagesWhat Will A Trustee's Deed Tell?Billy BowlesNo ratings yet

- Alvie's "Pig in A Poke"Document9 pagesAlvie's "Pig in A Poke"Billy BowlesNo ratings yet

- Attorneys' "Unbundled Service Pre - Litigation Package"Document3 pagesAttorneys' "Unbundled Service Pre - Litigation Package"Damion EmholtzNo ratings yet

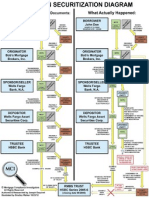

- RMBS Loan Securitization Flow ChartDocument1 pageRMBS Loan Securitization Flow ChartBilly BowlesNo ratings yet

- Explanation of Securitization By: Joe Esquivel (MCI)Document3 pagesExplanation of Securitization By: Joe Esquivel (MCI)Billy Bowles0% (1)

- Mortgage Compliance Investigators - Level 3 Securitization AuditDocument35 pagesMortgage Compliance Investigators - Level 3 Securitization AuditBilly BowlesNo ratings yet

- FANNIE MAE/FREDDIE MAC Loan Securitization Flow ChartDocument1 pageFANNIE MAE/FREDDIE MAC Loan Securitization Flow ChartBilly Bowles100% (1)

- Newsweek - July 3, 2020 USA PDFDocument52 pagesNewsweek - July 3, 2020 USA PDFRaimundo LimaNo ratings yet

- Excel Professional Services: Donor's Tax GuideDocument11 pagesExcel Professional Services: Donor's Tax GuideMae Angiela TansecoNo ratings yet

- RFBT03-08 - Law On Pledge, Mortgage and Antichresis - For DiscussionDocument9 pagesRFBT03-08 - Law On Pledge, Mortgage and Antichresis - For DiscussionJamNo ratings yet

- Chapter 3 Multiple Choice Questions / Page 1Document7 pagesChapter 3 Multiple Choice Questions / Page 1Navleen Kaur100% (1)

- Land Titles and Deeds Land Registration PDFDocument29 pagesLand Titles and Deeds Land Registration PDFRossette Anasario100% (1)

- Dharavi Redevelopment Project Offers Millennial OpportunityDocument13 pagesDharavi Redevelopment Project Offers Millennial OpportunitySaurav Singh100% (1)

- Land Patent FAQ, Part 2 - How To File A Land PatentDocument11 pagesLand Patent FAQ, Part 2 - How To File A Land PatentkatiaNo ratings yet

- How Is Saleable Area CalculatedDocument13 pagesHow Is Saleable Area Calculatedmave_tgNo ratings yet

- An Enquiry Into The Effect of GST On Real Estate Sector of IndiaDocument5 pagesAn Enquiry Into The Effect of GST On Real Estate Sector of IndiaEditor IJTSRDNo ratings yet

- Complete Guide and Checklist of Purchasing A Subsale Residential Property in Malaysia PDFDocument19 pagesComplete Guide and Checklist of Purchasing A Subsale Residential Property in Malaysia PDFVance ThuangNo ratings yet

- Accounting For PpeDocument37 pagesAccounting For PpeJohn Francis Idanan40% (5)

- 6.5. Rule 29 Valuation ReportDocument23 pages6.5. Rule 29 Valuation ReportOmkar BhosaleNo ratings yet

- 06 Activity 1panlaquiDocument1 page06 Activity 1panlaquiEmirish PNo ratings yet

- Southern Motors, Inc. v. Moscosco (G.R. No. L-14475, May 30, 1961)Document2 pagesSouthern Motors, Inc. v. Moscosco (G.R. No. L-14475, May 30, 1961)Lorie Jean UdarbeNo ratings yet

- Real Estate Industry Analysis and Target MarketsDocument16 pagesReal Estate Industry Analysis and Target MarketsDIVYANSHU SHEKHARNo ratings yet

- Mananquil Vs Moico-ReadDocument4 pagesMananquil Vs Moico-ReadPatrick James TanNo ratings yet

- Assignment in LEGAL COMMDocument3 pagesAssignment in LEGAL COMMSai PastranaNo ratings yet

- Big Draw of Tiong BahruDocument2 pagesBig Draw of Tiong BahruCheryl NgNo ratings yet

- MGCCT ProspectusDocument700 pagesMGCCT ProspectusMarc EdwardsNo ratings yet

- On Windows - Google Input ToolsDocument11 pagesOn Windows - Google Input ToolsKevin MorrisNo ratings yet

- Buena Mano Q2-2013 Visayas and Mindanao CatalogDocument25 pagesBuena Mano Q2-2013 Visayas and Mindanao CatalogJay CastilloNo ratings yet

- RDO No. 43A - East Pasig Zonal ValuesDocument161 pagesRDO No. 43A - East Pasig Zonal ValuesMiguel Pillas79% (14)

- City of Yes - Housing Opportunity - EAS - 24DCP033YDocument4 pagesCity of Yes - Housing Opportunity - EAS - 24DCP033YPaul GrazianoNo ratings yet

- Contact Info of Dealers 2024Document3 pagesContact Info of Dealers 2024nationalnetworkdelhiNo ratings yet

- Saln 1994 FormDocument3 pagesSaln 1994 FormJulius RarioNo ratings yet

- Notice of Transfer or Assignment of LoanDocument2 pagesNotice of Transfer or Assignment of LoanemrazNo ratings yet

- Modified Variation Order Management Model For Civil Engineering Construction ProjectsDocument119 pagesModified Variation Order Management Model For Civil Engineering Construction ProjectsAhed NabilNo ratings yet

- Approved List of ValuersDocument7 pagesApproved List of ValuersTim Tom100% (1)

- Quiet Title Actions by Stephen M. Parham Bloom Sugarman, LLP Telephone: 404-577-7710Document5 pagesQuiet Title Actions by Stephen M. Parham Bloom Sugarman, LLP Telephone: 404-577-7710robNo ratings yet

- Property de Leon Notes PDFDocument3 pagesProperty de Leon Notes PDFClarisseOsteria50% (4)