You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- 21 Christmas Songs and Carols For Solo GuitarDocument26 pages21 Christmas Songs and Carols For Solo Guitaritalo_ramirez_591% (23)

- 21 Christmas Songs and Carols For Solo GuitarDocument26 pages21 Christmas Songs and Carols For Solo Guitaritalo_ramirez_591% (23)

- Craig D'Andrea - Falling For TwelvesDocument7 pagesCraig D'Andrea - Falling For Twelvesitalo_ramirez_5100% (2)

- Craig D'Andrea - Falling For TwelvesDocument7 pagesCraig D'Andrea - Falling For Twelvesitalo_ramirez_5100% (2)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Craig D'andrea - As We GoDocument6 pagesCraig D'andrea - As We Goitalo_ramirez_5100% (1)

- Craig D'andrea - As We GoDocument6 pagesCraig D'andrea - As We Goitalo_ramirez_5100% (1)

- Craig D'andrea - Bird Feeder PoliticsDocument8 pagesCraig D'andrea - Bird Feeder Politicsitalo_ramirez_5No ratings yet

- Cash and Cash Equivalents PDFDocument4 pagesCash and Cash Equivalents PDFJade Gomez100% (1)

- Craig D'Andrea - Three Mile Bike RideDocument7 pagesCraig D'Andrea - Three Mile Bike Rideitalo_ramirez_5No ratings yet

- Distance Vector Routing AlgorithmDocument11 pagesDistance Vector Routing Algorithmitalo_ramirez_50% (1)

- Craig D'andrea - Just Trust MeDocument6 pagesCraig D'andrea - Just Trust Meitalo_ramirez_5No ratings yet

- Credit Card FraudDocument13 pagesCredit Card Fraudharshita patni100% (1)

- Management Thesis On Performance of Public Sector Banks Pre and Post Financial CrisisDocument36 pagesManagement Thesis On Performance of Public Sector Banks Pre and Post Financial Crisisjithunair13No ratings yet

- Samsung CSRDocument1 pageSamsung CSRitalo_ramirez_5No ratings yet

- Chap 004Document30 pagesChap 004italo_ramirez_5No ratings yet

- International Business: by Charles W.L. HillDocument26 pagesInternational Business: by Charles W.L. Hillitalo_ramirez_5No ratings yet

- International Business: by Charles W.L. HillDocument36 pagesInternational Business: by Charles W.L. HillZoheb SanjidNo ratings yet

- International Business: by Charles W.L. HillDocument28 pagesInternational Business: by Charles W.L. Hillitalo_ramirez_5No ratings yet

- Guess Whos My FavoriteDocument7 pagesGuess Whos My Favoriteitalo_ramirez_5No ratings yet

- International Business: by Charles W.L. HillDocument35 pagesInternational Business: by Charles W.L. HillhabibshadNo ratings yet

- Craig D'Andrea - Canada SadDocument6 pagesCraig D'Andrea - Canada Saditalo_ramirez_5No ratings yet

- International Business: by Charles W.L. HillDocument29 pagesInternational Business: by Charles W.L. Hillitalo_ramirez_5No ratings yet

- Craig D'andrea - Band Friends (Take 59)Document7 pagesCraig D'andrea - Band Friends (Take 59)italo_ramirez_5No ratings yet

- International Business: by Charles W.L. HillDocument26 pagesInternational Business: by Charles W.L. Hillitalo_ramirez_5No ratings yet

- Guess Whos My FavoriteDocument7 pagesGuess Whos My Favoriteitalo_ramirez_5No ratings yet

- SEIC 2019 Handbook PDFDocument24 pagesSEIC 2019 Handbook PDFYing ShengNo ratings yet

- Metlife Summer Mkt.Document60 pagesMetlife Summer Mkt.anilk5265No ratings yet

- TermsDocument3 pagesTermsAmy GarrettNo ratings yet

- Accounting AssmntDocument11 pagesAccounting AssmntasadNo ratings yet

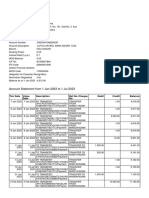

- Statement of Account - 08 - 25 - 16Document3 pagesStatement of Account - 08 - 25 - 16Radhe ShyamNo ratings yet

- Zakat Declaration Form CZ501Document1 pageZakat Declaration Form CZ501Zahid BashirNo ratings yet

- HowACreditCardIsProcessed PDFDocument5 pagesHowACreditCardIsProcessed PDFKornelius SitepuNo ratings yet

- Case DigestsDocument4 pagesCase DigestsJustine Jay Casas LopeNo ratings yet

- Colinares & Veloso vs. CA (Edited)Document3 pagesColinares & Veloso vs. CA (Edited)Ton RiveraNo ratings yet

- Customer Inquiry ReportDocument5 pagesCustomer Inquiry ReportRizky KurniawanNo ratings yet

- Manila Banking VS TeodoroDocument2 pagesManila Banking VS TeodoroSoltan Michael AlisanNo ratings yet

- Annotated Bib WEBSITEDocument3 pagesAnnotated Bib WEBSITEkylessmiles17No ratings yet

- Pantera IGS Fund PresentationDocument16 pagesPantera IGS Fund PresentationIrakli NinuaNo ratings yet

- Access Devices Regulation Act of 1998: Disclosure Requirements During Application and Solicitation ExceptionsDocument9 pagesAccess Devices Regulation Act of 1998: Disclosure Requirements During Application and Solicitation ExceptionsJustin CebrianNo ratings yet

- Bank Audit Analysis Documentation - Check ListDocument6 pagesBank Audit Analysis Documentation - Check Listrao_gmailNo ratings yet

- Menu DetailsDocument18 pagesMenu Detailssiddhmax21No ratings yet

- Derivatives Activation FormatDocument1 pageDerivatives Activation FormatbookbugNo ratings yet

- Iqtisad Al SunnahDocument53 pagesIqtisad Al SunnahKuzan AokijiNo ratings yet

- October 31, 2011 PostsDocument2,156 pagesOctober 31, 2011 PostsAlbert L. PeiaNo ratings yet

- Hacking: Don't Learn To Hack - Hack To LearnDocument26 pagesHacking: Don't Learn To Hack - Hack To Learndineshverma111No ratings yet

- JR 4 Axs BLBQVHH GL VDocument4 pagesJR 4 Axs BLBQVHH GL Vgaurav sehrawatNo ratings yet

- Scope of Retail Loans of Bank of Punjab LTDDocument8 pagesScope of Retail Loans of Bank of Punjab LTDVaibhav RastogiNo ratings yet

- Target: Iit/Engineering: A Word To ParentsDocument20 pagesTarget: Iit/Engineering: A Word To ParentsRathil MadihalliNo ratings yet

- New Product Development Process by Tamzidul AminDocument26 pagesNew Product Development Process by Tamzidul AminTamzidul Amin100% (1)

- United States v. Hoffler-Riddick, 4th Cir. (2007)Document10 pagesUnited States v. Hoffler-Riddick, 4th Cir. (2007)Scribd Government DocsNo ratings yet

- MGT602 Finalterm Subjective-By KamranDocument12 pagesMGT602 Finalterm Subjective-By KamranKifayat Ullah ToheediNo ratings yet

- Modul 10Document9 pagesModul 10Herdian KusumahNo ratings yet

- FIN 1finDocument41 pagesFIN 1finSudamMeryaNo ratings yet