You might also like

- Maximizing Your Wealth: A Comprehensive Guide to Understanding Gross and Net SalaryFrom EverandMaximizing Your Wealth: A Comprehensive Guide to Understanding Gross and Net SalaryNo ratings yet

- Rahul Agrawal's Salary Income AnalysisDocument32 pagesRahul Agrawal's Salary Income AnalysiskiranshingoteNo ratings yet

- TAX SALARY CHAPTERDocument32 pagesTAX SALARY CHAPTERkiranshingoteNo ratings yet

- Meaning of Salary': Condition For Charging Income U/H "Salaries"Document21 pagesMeaning of Salary': Condition For Charging Income U/H "Salaries"kiranshingoteNo ratings yet

- 40 40 Income From Salary BTDocument55 pages40 40 Income From Salary BTkiranshingoteNo ratings yet

- Salary IncomeDocument47 pagesSalary Incomearchana_anuragiNo ratings yet

- Income From Salary' & Its Computation: TaxationDocument35 pagesIncome From Salary' & Its Computation: TaxationChintan ShahNo ratings yet

- Income From SalaryDocument54 pagesIncome From SalaryMohsin ShaikhNo ratings yet

- Income From SalariesDocument30 pagesIncome From SalariesDeepak Gupta50% (2)

- Income From SalariesDocument19 pagesIncome From SalariesVineeta WadhwaniNo ratings yet

- Tax Rules for Salary IncomeDocument16 pagesTax Rules for Salary IncomeNoob GamerNo ratings yet

- Income From Salary GuideDocument11 pagesIncome From Salary Guiderakshitha9reddy-1No ratings yet

- Income From SalariesDocument70 pagesIncome From SalariesPratik AgrawalNo ratings yet

- Income Under The Head Salaries: (Section 15 - 17)Document55 pagesIncome Under The Head Salaries: (Section 15 - 17)leela naga janaki rajitha attiliNo ratings yet

- Learn Income Tax in Easy StepsDocument79 pagesLearn Income Tax in Easy Stepsbushra_anwarNo ratings yet

- Income From SalariesDocument28 pagesIncome From SalariesAshok Kumar Meheta100% (2)

- Income From SalariesDocument48 pagesIncome From Salarieskeerthana_hassan67% (6)

- Income From SalaryDocument29 pagesIncome From SalaryIsmail SayyadNo ratings yet

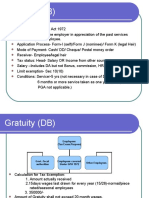

- GratuityDocument7 pagesGratuitySandeep TakNo ratings yet

- Income From SalaryDocument54 pagesIncome From SalaryJyoti Kalotra70% (10)

- O Sec 56 (2) I.E. IOS Clause V, Vi, VII (A & B), Ix, X, XiDocument7 pagesO Sec 56 (2) I.E. IOS Clause V, Vi, VII (A & B), Ix, X, XiRadhika SarawagiNo ratings yet

- Unit V HR OperationsDocument43 pagesUnit V HR OperationssnehalNo ratings yet

- Income Under The Head "Salaries"Document7 pagesIncome Under The Head "Salaries"Rahul AgarwalNo ratings yet

- Module 2 - Income From SalariesDocument22 pagesModule 2 - Income From SalariesAishwarya NNo ratings yet

- Provisions of Salary Taxation and Deductions under Section 15, 16, 17Document46 pagesProvisions of Salary Taxation and Deductions under Section 15, 16, 17Dhiraj YAdavNo ratings yet

- P2Document18 pagesP2YusufNo ratings yet

- tax Unit 4 (Tax on Individual)Document116 pagestax Unit 4 (Tax on Individual)Shivam PalNo ratings yet

- Salary Income LawDocument25 pagesSalary Income Lawvishal singhNo ratings yet

- Dr. Shannu Narayan PGP - Fintax Batch Session 3Document18 pagesDr. Shannu Narayan PGP - Fintax Batch Session 3ayman abdul salamNo ratings yet

- Project On:-Income From SalaryDocument32 pagesProject On:-Income From SalaryNida UldayNo ratings yet

- Notes On SalariesDocument18 pagesNotes On SalariesParul KansariaNo ratings yet

- Lesson 4 Income Under The Head Salaries - I: StructureDocument14 pagesLesson 4 Income Under The Head Salaries - I: StructuredrcpjoshiNo ratings yet

- Unit 2 SalaryDocument131 pagesUnit 2 SalaryRekha BansalNo ratings yet

- Taxable Salary IncomeDocument253 pagesTaxable Salary IncomedjbbuzzzNo ratings yet

- Chapter 4: Income From Salaries (Section 15 To 17) : Advance Direct Tax and Service Tax (Sub Code: 441)Document34 pagesChapter 4: Income From Salaries (Section 15 To 17) : Advance Direct Tax and Service Tax (Sub Code: 441)Puneeth DhondaleNo ratings yet

- Incomes On RetirementDocument11 pagesIncomes On RetirementShabnam HabeebNo ratings yet

- Salary Includes: U/s 17Document14 pagesSalary Includes: U/s 17Ansh NayyarNo ratings yet

- Salary SimplifiedDocument16 pagesSalary SimplifiedaruunstalinNo ratings yet

- Income From SalaryDocument21 pagesIncome From SalaryAditya Avasare60% (10)

- GratuityDocument6 pagesGratuityJagan MohanNo ratings yet

- Benefits of RetirementDocument2 pagesBenefits of Retirementvirajv1No ratings yet

- Final Indirect Tax ProjectDocument39 pagesFinal Indirect Tax Projectssg1015No ratings yet

- Allowances and Minmum Wage ActDocument22 pagesAllowances and Minmum Wage ActjinujithNo ratings yet

- Income From SalariesDocument30 pagesIncome From SalariesSanket MhetreNo ratings yet

- GRATUITY BY Pooja MiglaniDocument9 pagesGRATUITY BY Pooja MiglaniBrahamdeep KaurNo ratings yet

- Tax ProjectDocument34 pagesTax Projectjinalshah21097946No ratings yet

- Income From SalaryDocument30 pagesIncome From SalaryNicholas OwensNo ratings yet

- Income Tax Planning for Salary and House Property IncomeDocument51 pagesIncome Tax Planning for Salary and House Property IncomeRavi SinghNo ratings yet

- Salary Presentation 1Document56 pagesSalary Presentation 1NIRAVNo ratings yet

- Income Tax 05Document17 pagesIncome Tax 05AMJAD ULLA RNo ratings yet

- Know Your Retirement BookletDocument21 pagesKnow Your Retirement BookletPushparajan GunasekaranNo ratings yet

- Income from Salary GuideDocument15 pagesIncome from Salary GuideSakibul Haque NavinNo ratings yet

- Law of Taxation - Income Under The Head Salary (Autosaved)Document78 pagesLaw of Taxation - Income Under The Head Salary (Autosaved)Naman GoyalNo ratings yet

- Salary TheoryDocument53 pagesSalary TheorymohammedimranukNo ratings yet

- Income From SalaryDocument22 pagesIncome From SalaryJatin DrallNo ratings yet

- Income From SalariesDocument24 pagesIncome From SalariesvnbanjanNo ratings yet

- Salary Income-Pg DTDocument11 pagesSalary Income-Pg DTOnkar BandichhodeNo ratings yet

- Caultimates.com: Income Under Salary HeadDocument142 pagesCaultimates.com: Income Under Salary HeadOnlineNo ratings yet

- Financial Planning For Salaried Employee and Strategies For Tax SavingsDocument10 pagesFinancial Planning For Salaried Employee and Strategies For Tax Savingscity cyberNo ratings yet

- Business Strategies of Wal MartDocument22 pagesBusiness Strategies of Wal MartkiranshingoteNo ratings yet

- A Model of Business Ethics: Exploring Expectations, Perceptions, Evaluations and OutcomesDocument20 pagesA Model of Business Ethics: Exploring Expectations, Perceptions, Evaluations and OutcomesvirtualatallNo ratings yet

- CODE OF ETHICS AND AUDITOR INDEPENDENCEDocument17 pagesCODE OF ETHICS AND AUDITOR INDEPENDENCEkiranshingoteNo ratings yet

- Business Ethics - Ch5 (Samandova&Huseynali) PDFDocument16 pagesBusiness Ethics - Ch5 (Samandova&Huseynali) PDFkiranshingoteNo ratings yet

- 31 31 EthicsDocument18 pages31 31 EthicskiranshingoteNo ratings yet

- 41 Business EthicsDocument16 pages41 Business EthicsPrashant RaiNo ratings yet

- 17 Business Ethics ImpDocument21 pages17 Business Ethics ImpkiranshingoteNo ratings yet

- Work Ethics and MotivationDocument16 pagesWork Ethics and Motivationsimply_coool100% (3)

- Business EthicsDocument322 pagesBusiness EthicssameerzakNo ratings yet

- Principles of Business EthicsDocument26 pagesPrinciples of Business EthicskiranshingoteNo ratings yet

- 15 15 InfyDocument21 pages15 15 InfykiranshingoteNo ratings yet

- 16 16 PPT On Business EthicsDocument28 pages16 16 PPT On Business EthicskiranshingoteNo ratings yet

- Environmental Report12 Fe PDFDocument17 pagesEnvironmental Report12 Fe PDFkiranshingoteNo ratings yet

- Designpatterns 12 PDFDocument40 pagesDesignpatterns 12 PDFkiranshingoteNo ratings yet

- Woosley Introduction To Environmental Management SystemsDocument50 pagesWoosley Introduction To Environmental Management Systemschandro57No ratings yet

- Using Design Patterns With GRASP: G R A S PDocument34 pagesUsing Design Patterns With GRASP: G R A S PkiranshingoteNo ratings yet

- Designpatterns 03 PDFDocument35 pagesDesignpatterns 03 PDFkiranshingoteNo ratings yet

- Woosley Introduction To Environmental Management SystemsDocument50 pagesWoosley Introduction To Environmental Management Systemschandro57No ratings yet

- Designpatterns 08 PDFDocument32 pagesDesignpatterns 08 PDFkiranshingoteNo ratings yet

- Designpatterns 10 PDFDocument23 pagesDesignpatterns 10 PDFkiranshingoteNo ratings yet

- Designpatterns 11 PDFDocument32 pagesDesignpatterns 11 PDFkiranshingoteNo ratings yet

- Strategy Pa Ern and State Pa Ern: CSCI 3132 Summer 2011 1Document16 pagesStrategy Pa Ern and State Pa Ern: CSCI 3132 Summer 2011 1kiranshingoteNo ratings yet

- Designpatterns 02 RDD Strategy PDFDocument36 pagesDesignpatterns 02 RDD Strategy PDFkiranshingoteNo ratings yet

- The Command Pattern for Software DesignDocument29 pagesThe Command Pattern for Software DesignkiranshingoteNo ratings yet

- Designpatterns 07 PDFDocument33 pagesDesignpatterns 07 PDFkiranshingoteNo ratings yet

- The Observer Pattern: CSCI 3132 Summer 2011Document33 pagesThe Observer Pattern: CSCI 3132 Summer 2011kiranshingoteNo ratings yet

- Designpatterns 06 PDFDocument19 pagesDesignpatterns 06 PDFkiranshingoteNo ratings yet

- Designpatterns 01 Adapter Facade PDFDocument23 pagesDesignpatterns 01 Adapter Facade PDFkiranshingoteNo ratings yet

- Designpatterns 03 PDFDocument35 pagesDesignpatterns 03 PDFkiranshingoteNo ratings yet

- Strategy Pa Ern and State Pa Ern: CSCI 3132 Summer 2011 1Document16 pagesStrategy Pa Ern and State Pa Ern: CSCI 3132 Summer 2011 1kiranshingoteNo ratings yet

- Payslip 20230417170111Document2 pagesPayslip 20230417170111Iragavan IndraNo ratings yet

- Accounting Principles Canadian Volume II 7th Edition Weygandt Test Bank Full Chapter PDFDocument50 pagesAccounting Principles Canadian Volume II 7th Edition Weygandt Test Bank Full Chapter PDFEdwardBishopacsy100% (14)

- Magic Dominique Julius Julius TotalDocument4 pagesMagic Dominique Julius Julius TotalPaupauNo ratings yet

- Bethnal Green BMV Brochure MIPDocument7 pagesBethnal Green BMV Brochure MIPMark I'AnsonNo ratings yet

- CA Final DT Super 30 QuestionsDocument65 pagesCA Final DT Super 30 Questionsambica mahabhashyamNo ratings yet

- Tax Problem SolutionDocument5 pagesTax Problem SolutionSyed Ashraful Alam RubelNo ratings yet

- Guidelines and Instructions For BIR Form No. 1701Q Quarterly Income Tax Return For Individuals, Estates and TrustsDocument1 pageGuidelines and Instructions For BIR Form No. 1701Q Quarterly Income Tax Return For Individuals, Estates and TrustsAlyssa Hallasgo-Lopez AtabeloNo ratings yet

- Igcse Accounting Sole Trader Revision Questions FDocument56 pagesIgcse Accounting Sole Trader Revision Questions FAung Zaw Htwe100% (1)

- BTC 2021 Form CSDocument40 pagesBTC 2021 Form CSisty5nnt100% (1)

- Advances To Officers, Investment Property, Cash Surrender ValueDocument2 pagesAdvances To Officers, Investment Property, Cash Surrender ValueMary Joyce YuNo ratings yet

- Federal Income Tax Accounting Case StudyDocument1 pageFederal Income Tax Accounting Case Studykinmon2No ratings yet

- NEA Rankings and Estimates-2015!03!11aDocument130 pagesNEA Rankings and Estimates-2015!03!11aNC Policy WatchNo ratings yet

- WSBP LK TW I 2018Document85 pagesWSBP LK TW I 2018Nela NavidaNo ratings yet

- Caso Componiendo La Rentabilidad FinalDocument41 pagesCaso Componiendo La Rentabilidad FinalKevin Dani SanchezNo ratings yet

- 1010EZ FillableDocument5 pages1010EZ FillableFilozófus ÖnjelöltNo ratings yet

- PWC Adjusted Trial BalanceDocument2 pagesPWC Adjusted Trial BalanceHải NhưNo ratings yet

- CPCS 2021-011 Participation in Conventions, SeminarsDocument3 pagesCPCS 2021-011 Participation in Conventions, SeminarsEdson Jude DonosoNo ratings yet

- Bulgari Group Q1 2011 Results: May 10th 2011Document10 pagesBulgari Group Q1 2011 Results: May 10th 2011sl7789No ratings yet

- Cash and Accrual Basis - ExercisesDocument2 pagesCash and Accrual Basis - ExercisesTrisha Mae AlburoNo ratings yet

- Central Plain University income tax calculationDocument3 pagesCentral Plain University income tax calculationLFGS Finals0% (1)

- Cosmotic Surgical Center Business PlanDocument37 pagesCosmotic Surgical Center Business PlanRamchandra Cv100% (1)

- Prepare The Trial Balance:: Particulars Amount Particulars AmountDocument2 pagesPrepare The Trial Balance:: Particulars Amount Particulars Amountkush khandelwalNo ratings yet

- Ing N.V. Metro Manila Branch Vs Cir DigestDocument2 pagesIng N.V. Metro Manila Branch Vs Cir Digestbrian jay hernandezNo ratings yet

- Akuntansi Keuangan Menengah - Kieso - Solution Bab 5Document78 pagesAkuntansi Keuangan Menengah - Kieso - Solution Bab 5VimbyarnoPurboSuseno93% (30)

- Good Faith Bad Faith.Document4 pagesGood Faith Bad Faith.twenty19 law100% (1)

- Employee Benefits As 15Document58 pagesEmployee Benefits As 15Aayushi AroraNo ratings yet

- MBA Decision: Wilton University vs Mount Perry CollegeDocument1 pageMBA Decision: Wilton University vs Mount Perry CollegeShashwat DeshmukhNo ratings yet

- Canada's oil and gas regulatory regimeDocument16 pagesCanada's oil and gas regulatory regimekalite123No ratings yet

- 8 Session 20 Pillar 02 Finance Management Part 1Document13 pages8 Session 20 Pillar 02 Finance Management Part 1Azfah AliNo ratings yet

- Metro Schools Mike Looney ContractDocument7 pagesMetro Schools Mike Looney ContractAnonymous GF8PPILW5No ratings yet