You might also like

- Course 3 1xEV-DO Rev A Coverage PlanningDocument29 pagesCourse 3 1xEV-DO Rev A Coverage PlanningDoTrongLinhNo ratings yet

- Network Planning PDFDocument7 pagesNetwork Planning PDFPercy De SilvaNo ratings yet

- Cambium InvestorPresentationQ3 - 2019Document29 pagesCambium InvestorPresentationQ3 - 2019Nipun SahniNo ratings yet

- The Business Model Canvas: Key Partners Key Activities Value Propositions Customer Relationships Customer SegmentsDocument7 pagesThe Business Model Canvas: Key Partners Key Activities Value Propositions Customer Relationships Customer SegmentsRayon KandanganNo ratings yet

- India's PPP Program India S PPP Program: Progress, Key Takeaways & Emerging ChallengesDocument15 pagesIndia's PPP Program India S PPP Program: Progress, Key Takeaways & Emerging Challengess2002121No ratings yet

- State Energy Code Budget Guidance ARRA 2010Document1 pageState Energy Code Budget Guidance ARRA 2010bcap-oceanNo ratings yet

- ph1 App F Risk RegisterDocument3 pagesph1 App F Risk RegisterHugo HernandezNo ratings yet

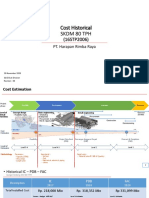

- Data Project SKDM - IC Vs PDB - R.08Document12 pagesData Project SKDM - IC Vs PDB - R.08Reza SanjayaNo ratings yet

- SRM FinalDocument16 pagesSRM FinalZubairLiaqatNo ratings yet

- I-ACT 2017 Yolanda Muliana (OK) Rev 6Document27 pagesI-ACT 2017 Yolanda Muliana (OK) Rev 6Yolanda MulianaNo ratings yet

- Strategic Internet Network Consultant ProposalDocument82 pagesStrategic Internet Network Consultant ProposalReinhard LalNo ratings yet

- Pres Miller NissanDocument26 pagesPres Miller NissanRiselda Myshku KajaNo ratings yet

- In-Building Wireless Infrastructure Solutions: D-RAN Rate Card and eRAN Concept StudyDocument30 pagesIn-Building Wireless Infrastructure Solutions: D-RAN Rate Card and eRAN Concept StudyDaniel RoureNo ratings yet

- Context Aware Security For Mobile Enterprise Appnote enDocument5 pagesContext Aware Security For Mobile Enterprise Appnote enprakistaoNo ratings yet

- The Future of Broadcasting For MSO HATHWAY - 20160601Document42 pagesThe Future of Broadcasting For MSO HATHWAY - 20160601kentmultanNo ratings yet

- How To Fill-In This Template:: All Other Fields Are Protected To Avoid Accidential Changes To The CalculationDocument11 pagesHow To Fill-In This Template:: All Other Fields Are Protected To Avoid Accidential Changes To The CalculationPravin Balasaheb GunjalNo ratings yet

- Little Cottonwood Canyon Eis: Project Overview and Draft Alternatives SummaryDocument3 pagesLittle Cottonwood Canyon Eis: Project Overview and Draft Alternatives SummaryLee DavidsonNo ratings yet

- Metric MissionDocument156 pagesMetric MissionV.I.G.MenonNo ratings yet

- ADVANCE ENTERPRISE KA PrixDocument1 pageADVANCE ENTERPRISE KA PrixMelchi BanzaNo ratings yet

- Presentation To Honourable Central Electricity Regulatory Commission On Views/Suggestions On Cercs' Discussion Paper On Terms and Condition of TariffDocument47 pagesPresentation To Honourable Central Electricity Regulatory Commission On Views/Suggestions On Cercs' Discussion Paper On Terms and Condition of TariffRavinder SharmaNo ratings yet

- Silicon Valley PortfolioDocument2 pagesSilicon Valley PortfolioAzif K MohammedNo ratings yet

- 2018 TYA Final WebDocument32 pages2018 TYA Final WebWilber SilesNo ratings yet

- CMMI High Maturity Best Practices HMBP 2010: Process Performance Models:Not Necessarily Complex by Himanshu Pandey and Nishu LohiaDocument25 pagesCMMI High Maturity Best Practices HMBP 2010: Process Performance Models:Not Necessarily Complex by Himanshu Pandey and Nishu LohiaQAINo ratings yet

- Chap-5 Network Design in The Supply ChainDocument44 pagesChap-5 Network Design in The Supply ChainMd. Sirajul IslamNo ratings yet

- Bs A Ordering Guide For EuropeDocument50 pagesBs A Ordering Guide For Europe李微風No ratings yet

- Kajian#4 - TTH4A3 - Perencanaan Jaringan Seluler - 3G-CaseDocument97 pagesKajian#4 - TTH4A3 - Perencanaan Jaringan Seluler - 3G-CaseRaksiNo ratings yet

- UMTS Coverage PlanningDocument55 pagesUMTS Coverage PlanningtadeleNo ratings yet

- Impact of Poor ForecastingDocument10 pagesImpact of Poor ForecastingMaira HassanNo ratings yet

- Bauxite ProjectDocument20 pagesBauxite Projectzainul fitri100% (1)

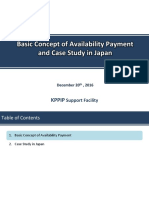

- Jica Basic Concept of AP and Case Study in JapanDocument28 pagesJica Basic Concept of AP and Case Study in JapanhenrikoNo ratings yet

- Optimisation of Telecommunication Costs: (Pri + Voip)Document22 pagesOptimisation of Telecommunication Costs: (Pri + Voip)TapankhamarNo ratings yet

- Metro FY22 Budget - Outreach Presentation - FinalDocument18 pagesMetro FY22 Budget - Outreach Presentation - FinalMetro Los AngelesNo ratings yet

- LA Metro Proposed FY 20-21 BudgetDocument24 pagesLA Metro Proposed FY 20-21 BudgetMetro Los AngelesNo ratings yet

- ASUG82475 - Removing Barriers To Customer-Centric Service With SAP Service CloudDocument17 pagesASUG82475 - Removing Barriers To Customer-Centric Service With SAP Service CloudSyed Sohail AhmedNo ratings yet

- Case Book - Harvard 2011Document139 pagesCase Book - Harvard 2011John Snowman100% (1)

- Mindset - The New Psychology of SuccessDocument18 pagesMindset - The New Psychology of SuccessAjaya KumarNo ratings yet

- Benchmarking and Optimising Maintenance For TurnaroundsDocument5 pagesBenchmarking and Optimising Maintenance For TurnaroundsGuru Raja Ragavendran NagarajanNo ratings yet

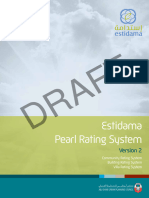

- Estidama - Pearl Rating System - Version-2.0Document185 pagesEstidama - Pearl Rating System - Version-2.0HabiNo ratings yet

- 2019.09.03 - EST & SCHED - r.2 - VARIANCE ReportDocument1 page2019.09.03 - EST & SCHED - r.2 - VARIANCE ReportSri100% (1)

- TruEarth Case AnalysisDocument53 pagesTruEarth Case Analysisneeraj_ghs679No ratings yet

- Workiva Q4-'22-Investor-PresentationDocument24 pagesWorkiva Q4-'22-Investor-PresentationkrrajanNo ratings yet

- Individual Performance Commitment and Review Form (Ipcrf)Document11 pagesIndividual Performance Commitment and Review Form (Ipcrf)Acire Nonac100% (3)

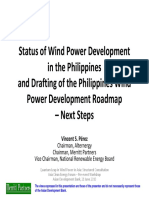

- (B) Vince Perez ADB Wind Power Roadmap 20 June 2010Document15 pages(B) Vince Perez ADB Wind Power Roadmap 20 June 2010ImjusttryingtohelpNo ratings yet

- Power Development Program (Power Supply Plan)Document49 pagesPower Development Program (Power Supply Plan)Emman Joshua BustoNo ratings yet

- PLDT Inc Tel: Last Close Fair Value Market CapDocument4 pagesPLDT Inc Tel: Last Close Fair Value Market Capskynyrd75No ratings yet

- My IPCR July - Dec 2020Document9 pagesMy IPCR July - Dec 2020Jopheth RelucioNo ratings yet

- Mckinsey Usps Future Bus Model2Document39 pagesMckinsey Usps Future Bus Model2Leo SaitoNo ratings yet

- Business Theory: FinanceDocument93 pagesBusiness Theory: FinanceNazarethNo ratings yet

- Black Diamond Council Fire Study Presentation - PUBLISHED 12.18.2020Document26 pagesBlack Diamond Council Fire Study Presentation - PUBLISHED 12.18.2020Ray StillNo ratings yet

- Economic and Political Weekly Economic and Political WeeklyDocument5 pagesEconomic and Political Weekly Economic and Political WeeklyGunjan ChandavatNo ratings yet

- ABT Improvement Project V0.1Document7 pagesABT Improvement Project V0.1Usman JavedNo ratings yet

- Gsc11 - gtsc4 - 14 Next Phase of NGN Global StandardizationDocument12 pagesGsc11 - gtsc4 - 14 Next Phase of NGN Global StandardizationAndreas Novemi UkiNo ratings yet

- Error Proofing TechniquesDocument140 pagesError Proofing TechniquesBoby SaputraNo ratings yet

- MKTG Sample Plan PresDocument102 pagesMKTG Sample Plan PresCarl O'ConnellNo ratings yet

- Liquid Mud Plant VesselDocument29 pagesLiquid Mud Plant VesselMich100% (1)

- Micro Financing SolutionDocument2 pagesMicro Financing SolutionUmang Mahesh DadhichNo ratings yet

- Original C-BV-RE-0783 - 060409Document8 pagesOriginal C-BV-RE-0783 - 060409Parasuram PadmanabhanNo ratings yet

- Technical, Commercial and Regulatory Challenges of QoS: An Internet Service Model PerspectiveFrom EverandTechnical, Commercial and Regulatory Challenges of QoS: An Internet Service Model PerspectiveNo ratings yet