You might also like

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- All in A NameDocument1 pageAll in A NameSudeep RoyNo ratings yet

- HinglishDocument1 pageHinglishSudeep RoyNo ratings yet

- Akbar & BirbalDocument2 pagesAkbar & BirbalSudeep RoyNo ratings yet

- Maturity Level DetailsDocument5 pagesMaturity Level DetailsSudeep RoyNo ratings yet

- ReportDocument41 pagesReportSudeep RoyNo ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Food For Thought 2014 11 M&a LTM 2014Document32 pagesFood For Thought 2014 11 M&a LTM 2014lauraNo ratings yet

- Roshan ProjectDocument253 pagesRoshan ProjectAmit PrajapatiNo ratings yet

- Project Management, Tools, Process, Plans and Project Planning TipsDocument16 pagesProject Management, Tools, Process, Plans and Project Planning TipsChuma Khan100% (1)

- Business Economics: AssignmentDocument4 pagesBusiness Economics: AssignmentRaffay MaqboolNo ratings yet

- Currensee Correlation - OANDADocument1 pageCurrensee Correlation - OANDAwim006100% (1)

- Resources and Capabilities: Their Importance How To Analyse ThemDocument34 pagesResources and Capabilities: Their Importance How To Analyse Themvishal7debnat-402755No ratings yet

- University CatalogueDocument166 pagesUniversity CatalogueOloo Yussuf Ochieng'No ratings yet

- Chapter 05Document4 pagesChapter 05Md. Saidul IslamNo ratings yet

- Letter of AppoinmentDocument4 pagesLetter of Appoinmentmonu tyagi100% (1)

- Flipkart InitialDocument9 pagesFlipkart InitialVivek MeshramNo ratings yet

- The Securities Contracts (Regulation) Act, 1956: © The Institute of Chartered Accountants of IndiaDocument20 pagesThe Securities Contracts (Regulation) Act, 1956: © The Institute of Chartered Accountants of Indianabin shresthaNo ratings yet

- Listing Presentation Scripts: Sitting Down at The Table (Via Zoom)Document5 pagesListing Presentation Scripts: Sitting Down at The Table (Via Zoom)kang hyo minNo ratings yet

- SalesInvoiceImport 02 MARET 2023Document6 pagesSalesInvoiceImport 02 MARET 2023Fakta IdNo ratings yet

- Managerial Finance: Article InformationDocument22 pagesManagerial Finance: Article Informationlia s.No ratings yet

- CSR ModifiedDocument72 pagesCSR Modifiedadilnr1No ratings yet

- Star Trek PDFDocument31 pagesStar Trek PDF1701musicproject100% (1)

- Mathematics of Finance Exercise and SolutionDocument14 pagesMathematics of Finance Exercise and Solutionfarid rosliNo ratings yet

- Case Study 3Document4 pagesCase Study 3Anwar Iqbal50% (2)

- A Buyers Guide To Treasury Management SystemsDocument28 pagesA Buyers Guide To Treasury Management Systemspasintfi100% (1)

- Maximo Data Relationships PrimaryDocument29 pagesMaximo Data Relationships PrimaryEnio BassoNo ratings yet

- United States District Court District of NebraskaDocument4 pagesUnited States District Court District of Nebraskascion.scionNo ratings yet

- A Tale of Two Electronic Components DistributorsDocument2 pagesA Tale of Two Electronic Components DistributorsAqsa100% (1)

- U74999HR2017PTC066978 OTRE 143398915 Form-PAS-3-20012020 SignedDocument5 pagesU74999HR2017PTC066978 OTRE 143398915 Form-PAS-3-20012020 Signedakshay bhartiyaNo ratings yet

- 2.G.R. No. 116123Document10 pages2.G.R. No. 116123Lord AumarNo ratings yet

- Delta CEO Richard Anderson's 2012 Year-End MemoDocument2 pagesDelta CEO Richard Anderson's 2012 Year-End MemoSherylNo ratings yet

- Esco BROCHUREDocument18 pagesEsco BROCHUREJohn GonzalezNo ratings yet

- Demat Account Details of Unicon Investment SolutionDocument53 pagesDemat Account Details of Unicon Investment SolutionManjeet SinghNo ratings yet

- Pampanga PB ValisesDocument20 pagesPampanga PB Valisesallyssa monica duNo ratings yet

- Employee Service RegulationDocument173 pagesEmployee Service RegulationKrishan Kumar Sharma50% (2)

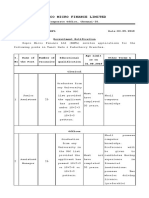

- Repco Micro Finance Limited: Corporate Office, Chennai-35Document4 pagesRepco Micro Finance Limited: Corporate Office, Chennai-35Abaraj IthanNo ratings yet