You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Date Account & Explanation F Debit CreditDocument7 pagesDate Account & Explanation F Debit CreditCindy Claire Pilapil88% (8)

- Case Studies of Cost and Works AccountingDocument17 pagesCase Studies of Cost and Works AccountingShalini Srivastav50% (2)

- Employability Skills Workshop 18, 19, 20 OCTOBER 2012: PGDM 11-13 BatchDocument5 pagesEmployability Skills Workshop 18, 19, 20 OCTOBER 2012: PGDM 11-13 BatchShalini SrivastavNo ratings yet

- Smita Mankad Bio Apr13Document2 pagesSmita Mankad Bio Apr13Shalini SrivastavNo ratings yet

- Accman: Integrating Knowledge and PracticeDocument6 pagesAccman: Integrating Knowledge and PracticeShalini SrivastavNo ratings yet

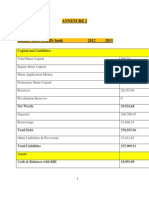

- Annexure 2Document13 pagesAnnexure 2Shalini SrivastavNo ratings yet

- Prasenjit Fact SheetDocument3 pagesPrasenjit Fact SheetShalini SrivastavNo ratings yet

- Accman Institute of Management: Student Fact SheetDocument3 pagesAccman Institute of Management: Student Fact SheetShalini SrivastavNo ratings yet

- Banking Law ProjectDocument25 pagesBanking Law ProjectRavi Singh SolankiNo ratings yet

- Statement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceDocument4 pagesStatement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceAyush kumarNo ratings yet

- Ch13 (Man)Document44 pagesCh13 (Man)kevin echiverriNo ratings yet

- 1) Introduction To Management Accounting-2Document34 pages1) Introduction To Management Accounting-2fpasanfiverNo ratings yet

- List of Automatic Crossover Trading Partner (Insurers) in Production Do Not Include Number Shown Below On Incoming ClaimsDocument23 pagesList of Automatic Crossover Trading Partner (Insurers) in Production Do Not Include Number Shown Below On Incoming Claimsspicypoova_899586184No ratings yet

- 2023 Audit Final ExamDocument17 pages2023 Audit Final ExamrakutenmeeshoNo ratings yet

- Chapter 13 - Financial Asset at Fair ValueDocument10 pagesChapter 13 - Financial Asset at Fair ValueMark LopezNo ratings yet

- Comparative Study of India Infoline With Other Broking FirmsDocument66 pagesComparative Study of India Infoline With Other Broking FirmsSami Zama50% (2)

- Module 2 Compound Interest 2Document38 pagesModule 2 Compound Interest 2Jennilyn RiveraNo ratings yet

- Common Business Transactions Using The Rules of Debit and CreditDocument9 pagesCommon Business Transactions Using The Rules of Debit and CreditSHIERY MAE FALCONITINNo ratings yet

- Sujarwo, 2019Document10 pagesSujarwo, 2019Putu Krisna Bayu PutraNo ratings yet

- Module 14 EquityDocument17 pagesModule 14 EquityZyril RamosNo ratings yet

- A Comparative Analysis of Financial Products in Banking Industry With Special Reference To ICICI Bank and State Bank of IndiaDocument98 pagesA Comparative Analysis of Financial Products in Banking Industry With Special Reference To ICICI Bank and State Bank of IndiaWhatsapp stutsNo ratings yet

- PidiliteDocument21 pagesPidiliteMandeep BatraNo ratings yet

- Unit 7 - MoneyDocument8 pagesUnit 7 - Moneyapi-428447569No ratings yet

- EM 531 - Lecture Notes 7Document45 pagesEM 531 - Lecture Notes 7Hasan ÖzdemNo ratings yet

- Australian Financial Advice Landscape: This Is An Abridged Version of The Full Report Published in December 2019Document52 pagesAustralian Financial Advice Landscape: This Is An Abridged Version of The Full Report Published in December 2019Stuff NewsroomNo ratings yet

- Acct Statement - XX1794 - 20122023Document49 pagesAcct Statement - XX1794 - 20122023rakshit7985231877No ratings yet

- Taller 1Document9 pagesTaller 1Adriana BlasNo ratings yet

- Crossing of Cheques BLDocument27 pagesCrossing of Cheques BLVikash kumarNo ratings yet

- Adat Farmers' Service Co-Operative Bank Ltd. - A Profile: TH THDocument4 pagesAdat Farmers' Service Co-Operative Bank Ltd. - A Profile: TH THJayasankar MallisseriNo ratings yet

- Abhinay Axis Project FinalDocument97 pagesAbhinay Axis Project FinalabhinaygoenkaNo ratings yet

- Chapter 1 - Accounting For PartnershipDocument13 pagesChapter 1 - Accounting For PartnershipKim EllaNo ratings yet

- K.P.R. Sugar Mill LimitedDocument7 pagesK.P.R. Sugar Mill LimitedKarthikeyan RK SwamyNo ratings yet

- Money and Banking: Module - 11Document14 pagesMoney and Banking: Module - 11Sarthak PithoriyaNo ratings yet

- Credit Risk Literature ReviewDocument6 pagesCredit Risk Literature Reviewnelnlpvkg100% (1)

- Laporan Transaksi: Kepada Yth, Dr. Rosmelia Esther Gloria SilabanDocument21 pagesLaporan Transaksi: Kepada Yth, Dr. Rosmelia Esther Gloria SilabanRosalindaNo ratings yet

- Financial Times 20151120Document62 pagesFinancial Times 20151120stefanoNo ratings yet

- Portfolio ManagementDocument20 pagesPortfolio ManagementREHANRAJNo ratings yet