You might also like

- Value Chain Management Capability A Complete Guide - 2020 EditionFrom EverandValue Chain Management Capability A Complete Guide - 2020 EditionNo ratings yet

- Accounting Problem Solving QuestionsDocument24 pagesAccounting Problem Solving QuestionsForTheLoveOfFitnessNo ratings yet

- FCFEDocument7 pagesFCFEbang bebetNo ratings yet

- 4-Time Value of MoneyDocument35 pages4-Time Value of Moneysherif_awad100% (1)

- Discounted Cash Flow ApplicationsDocument27 pagesDiscounted Cash Flow ApplicationsAvinash DasNo ratings yet

- Ratio Analysis of RCF LTDDocument46 pagesRatio Analysis of RCF LTDAnil KoliNo ratings yet

- 09 KRM Om10 Tif ch07Document53 pages09 KRM Om10 Tif ch07Anonymous L7XrxpeI1zNo ratings yet

- Analysis of Financial StatementsDocument33 pagesAnalysis of Financial StatementsKushal Lapasia100% (1)

- EXERCISE - Calculating The Internal Rate of ReturnDocument5 pagesEXERCISE - Calculating The Internal Rate of ReturnNipun BajajNo ratings yet

- Pre-Money Valuation: Multiple ApproachDocument16 pagesPre-Money Valuation: Multiple ApproachDavid ChikhladzeNo ratings yet

- Auditing CA Final Investigation and Due DiligenceDocument26 pagesAuditing CA Final Investigation and Due Diligencevarunmonga90No ratings yet

- Risk and Return Fundamentals: Portfolio-A Collection, or Group, of AssetsDocument104 pagesRisk and Return Fundamentals: Portfolio-A Collection, or Group, of AssetsSagorNo ratings yet

- Aicpa Accounting GlossaryDocument24 pagesAicpa Accounting GlossaryRafael AlemanNo ratings yet

- L8 Raising CapitalDocument26 pagesL8 Raising CapitalKranthi ManthriNo ratings yet

- Introduction To Financial ManagemntDocument29 pagesIntroduction To Financial ManagemntibsNo ratings yet

- Assignment 1 Iqra Javaid - 46032 Submitted To Muhammad ZeeshanDocument6 pagesAssignment 1 Iqra Javaid - 46032 Submitted To Muhammad ZeeshanFAIQ KHALIDNo ratings yet

- Valuing Private Companies:: Factors and Approaches To ConsiderDocument35 pagesValuing Private Companies:: Factors and Approaches To ConsiderAvinash DasNo ratings yet

- Cost of Capital ExplainedDocument18 pagesCost of Capital ExplainedzewdieNo ratings yet

- Val PacketDocument157 pagesVal PacketKumar PrashantNo ratings yet

- Pestle Analysis - Alesh and GroupDocument18 pagesPestle Analysis - Alesh and GroupJay KapoorNo ratings yet

- Portfolio Selection Using Sharpe, Treynor & Jensen Performance IndexDocument15 pagesPortfolio Selection Using Sharpe, Treynor & Jensen Performance Indexktkalai selviNo ratings yet

- Chapter 06 - Risk & ReturnDocument42 pagesChapter 06 - Risk & Returnmnr81No ratings yet

- Sources of FinanceDocument32 pagesSources of FinanceDeepshikha Gupta100% (1)

- Entrepreneurship ExamDocument24 pagesEntrepreneurship ExamzyleahlsNo ratings yet

- Test 3 Project Finance Case Question Yogesh GandhiDocument14 pagesTest 3 Project Finance Case Question Yogesh GandhiYogi GandhiNo ratings yet

- Mini Case On Risk Return 1-SolutionDocument27 pagesMini Case On Risk Return 1-Solutionjagrutic_09No ratings yet

- Investor Behaviour and Factors Influencing DecisionsDocument44 pagesInvestor Behaviour and Factors Influencing DecisionsSajoy P.B.100% (1)

- Nestle Report AnalysisDocument3 pagesNestle Report AnalysisAkshatAgarwalNo ratings yet

- Cost of CapitalDocument55 pagesCost of CapitalSaritasaruNo ratings yet

- Financial Planning and Forecasting GuideDocument35 pagesFinancial Planning and Forecasting GuideSaidarshan RevandkarNo ratings yet

- Fundamentals of Corporate Finance Chap 001Document18 pagesFundamentals of Corporate Finance Chap 001tyremiNo ratings yet

- Capital Budgeting ReportDocument29 pagesCapital Budgeting ReportJermaine Carreon100% (1)

- Investment &financial Analysis AssignmentDocument5 pagesInvestment &financial Analysis AssignmentfionatuNo ratings yet

- Recall The Flows of Funds and Decisions Important To The Financial ManagerDocument27 pagesRecall The Flows of Funds and Decisions Important To The Financial ManagerAyaz MahmoodNo ratings yet

- Bank Ratio Analysis v.2Document30 pagesBank Ratio Analysis v.2moe.jee6173100% (1)

- Pricing Strategy and ManagementDocument15 pagesPricing Strategy and Managementadibhai06No ratings yet

- The Time Value of MoneyDocument66 pagesThe Time Value of MoneyrachealllNo ratings yet

- CH - 4 - Time Value of MoneyDocument49 pagesCH - 4 - Time Value of Moneyak sNo ratings yet

- Capital StructureDocument6 pagesCapital StructureHasan Zahoor100% (1)

- Actuaries 4Document69 pagesActuaries 4MuradNo ratings yet

- NPVDocument11 pagesNPVMaNi Rajpoot100% (1)

- Risk and ReturnDocument70 pagesRisk and Returnmiss_hazel85No ratings yet

- Beta Levered and UnleveredDocument3 pagesBeta Levered and UnleveredNouman MujahidNo ratings yet

- Sensitivity AnalysisDocument13 pagesSensitivity Analysisrastogi paragNo ratings yet

- Risk Analysis in Capital BudgetingDocument18 pagesRisk Analysis in Capital BudgetingKushagra RaghavNo ratings yet

- Capital Budgeting Cash FlowsDocument13 pagesCapital Budgeting Cash FlowsNagaeshwary Murugan100% (1)

- Ratio Analysis: R K MohantyDocument30 pagesRatio Analysis: R K Mohantybgowda_erp1438No ratings yet

- Chap 2 Financial Analysis & PlanningDocument108 pagesChap 2 Financial Analysis & PlanningmedrekNo ratings yet

- Investor Guide BookDocument169 pagesInvestor Guide BooktonyvinayakNo ratings yet

- Challenges in Forecasting Exchange Rates by Multinational Corporations Ms 12may2016Document22 pagesChallenges in Forecasting Exchange Rates by Multinational Corporations Ms 12may2016dr Milorad Stamenovic100% (3)

- Calculate Capital Budgeting Payback Period & ARRDocument83 pagesCalculate Capital Budgeting Payback Period & ARRAashutosh MishraNo ratings yet

- Capital Budgeting - SolutionsDocument16 pagesCapital Budgeting - SolutionsDoula IshamNo ratings yet

- Unit 2 Capital StructureDocument27 pagesUnit 2 Capital StructureNeha RastogiNo ratings yet

- Analysis of Financial Statements: Answers To Selected End-Of-Chapter QuestionsDocument9 pagesAnalysis of Financial Statements: Answers To Selected End-Of-Chapter Questionsfeitheart_rukaNo ratings yet

- Financial Ratio MBA Complete ChapterDocument19 pagesFinancial Ratio MBA Complete ChapterDhruv100% (1)

- Analyze financial ratios to evaluate FM222 courseDocument60 pagesAnalyze financial ratios to evaluate FM222 courseLai Alvarez100% (1)

- Chap 6 (Fix)Document13 pagesChap 6 (Fix)Le TanNo ratings yet

- FINANCIAL RATIO ANALYSISDocument25 pagesFINANCIAL RATIO ANALYSISWong Siu CheongNo ratings yet

- Determing The Factors of Industrial RelationsDocument2 pagesDeterming The Factors of Industrial RelationsZahid HassanNo ratings yet

- Ed Module 2Document4 pagesEd Module 2Zahid HassanNo ratings yet

- Flow ChartDocument1 pageFlow ChartZahid HassanNo ratings yet

- Should Euthalesia (Mercy Killing) Be LegalisedDocument3 pagesShould Euthalesia (Mercy Killing) Be LegalisedZahid HassanNo ratings yet

- Statistical Presentation Tools Descriptive StatisticsDocument3 pagesStatistical Presentation Tools Descriptive StatisticsZahid HassanNo ratings yet

- Module 2 LearningDocument27 pagesModule 2 LearningZahid HassanNo ratings yet

- Customer-Defined Service Standards: Presented by IsmailayazruknuddinDocument18 pagesCustomer-Defined Service Standards: Presented by IsmailayazruknuddinZahid HassanNo ratings yet

- POM Module 4Document1 pagePOM Module 4Zahid HassanNo ratings yet

- HistoryDocument6 pagesHistoryZahid HassanNo ratings yet

- GKDocument1 pageGKZahid HassanNo ratings yet

- Chess RulesDocument8 pagesChess RulesZahid HassanNo ratings yet

- Fund Sbi Mutual Fund Scheme Sbi Pharma Fund (G)Document31 pagesFund Sbi Mutual Fund Scheme Sbi Pharma Fund (G)Zahid HassanNo ratings yet

- Accounting For ManagementDocument5 pagesAccounting For ManagementZahid HassanNo ratings yet

- Careers and Career ManagementDocument18 pagesCareers and Career ManagementZahid HassanNo ratings yet

- BCMC Mod 07Document55 pagesBCMC Mod 07Zahid HassanNo ratings yet

- IhrmDocument1 pageIhrmZahid HassanNo ratings yet

- BCMC Mod 07Document55 pagesBCMC Mod 07Zahid HassanNo ratings yet

- Share Debenture HolderDocument45 pagesShare Debenture HoldergetstockalNo ratings yet

- Statistical Presentation Tools Descriptive StatisticsDocument3 pagesStatistical Presentation Tools Descriptive StatisticsZahid HassanNo ratings yet

- HistoryDocument6 pagesHistoryZahid HassanNo ratings yet

- Simplify: (I) 8888+888+88+8 (Ii) 11992-7823-456 2. (A+b)Document1 pageSimplify: (I) 8888+888+88+8 (Ii) 11992-7823-456 2. (A+b)Zahid HassanNo ratings yet

- Papc SyllabusDocument2 pagesPapc SyllabusZahid HassanNo ratings yet

- Presentation TopicsDocument1 pagePresentation TopicsZahid HassanNo ratings yet

- Venture CapitalDocument7 pagesVenture CapitalZahid Hassan0% (1)

- Anjuman Institute of Technology and Management Department of Manegement Studies Mba 1 Sem 1 Internal Assessment TestDocument1 pageAnjuman Institute of Technology and Management Department of Manegement Studies Mba 1 Sem 1 Internal Assessment TestZahid HassanNo ratings yet

- BCG MatrixDocument2 pagesBCG MatrixZahid HassanNo ratings yet

- Anjuman Institute of Technology and Management Department of Management StudiesDocument2 pagesAnjuman Institute of Technology and Management Department of Management StudiesZahid HassanNo ratings yet

- All PG DiplomaDocument20 pagesAll PG DiplomaZahid HassanNo ratings yet

- American Depositary Receipts and Global Depository Receipts: Presented BY Kirti GargDocument14 pagesAmerican Depositary Receipts and Global Depository Receipts: Presented BY Kirti Gargmemeenusaini100% (1)

- Withdrawal of Restriction On Short SalesDocument1 pageWithdrawal of Restriction On Short SalesKhushiNo ratings yet

- M&M 2006-2007Document160 pagesM&M 2006-2007Ramajit BhartiNo ratings yet

- Impairing The Microsoft - Nokia PairingDocument54 pagesImpairing The Microsoft - Nokia Pairingjk kumarNo ratings yet

- Materials Management ConceptDocument48 pagesMaterials Management Conceptajinkyabhavsar75% (4)

- Mathematics For Retail Buying - Six Month Planning and ComponentsDocument27 pagesMathematics For Retail Buying - Six Month Planning and ComponentsBhavyata ChavdaNo ratings yet

- Important Banking & Finance Abbreviations PDF by AffairsCloudDocument7 pagesImportant Banking & Finance Abbreviations PDF by AffairsCloudShekh DNo ratings yet

- Hedging Against Rising Coal Prices Using Coal FuturesDocument38 pagesHedging Against Rising Coal Prices Using Coal FuturesSunil ToshniwalNo ratings yet

- Chapter 4: Option Pricing Models: The Binomial ModelDocument9 pagesChapter 4: Option Pricing Models: The Binomial ModelDUY LE NHAT TRUONGNo ratings yet

- Tybms Black Book Topics Finance Revisedxlsx PDF FreeDocument2 pagesTybms Black Book Topics Finance Revisedxlsx PDF FreeShreyaNo ratings yet

- Foreign Exchange QuotesDocument4 pagesForeign Exchange QuotesVishant ChopraNo ratings yet

- Ebay Webdoc 649Document9 pagesEbay Webdoc 649Abdirisaq MohamudNo ratings yet

- 6sub Alll in One Walang PE Pati EappDocument136 pages6sub Alll in One Walang PE Pati EappJeff Dela RosaNo ratings yet

- Financial Market DefinitionDocument9 pagesFinancial Market DefinitionMARJORIE BAMBALANNo ratings yet

- Account Must Do List!! Nov - 2022 - 220911 - 200510Document259 pagesAccount Must Do List!! Nov - 2022 - 220911 - 200510KartikNo ratings yet

- Financial Management SyllabusDocument13 pagesFinancial Management Syllabusharshgupta.16018No ratings yet

- Ijser: Mathematical Modeling in FinanceDocument21 pagesIjser: Mathematical Modeling in FinancealexeyNo ratings yet

- RTP Dec 2020 QnsDocument13 pagesRTP Dec 2020 QnsbinuNo ratings yet

- AAII PortfolioBuildingEBook PDFDocument61 pagesAAII PortfolioBuildingEBook PDFelisaNo ratings yet

- Capital Structure and Cost of CapitalVal Exercises StudentsDocument2 pagesCapital Structure and Cost of CapitalVal Exercises StudentsApa-ap, CrisdelleNo ratings yet

- United Spirits: Performance HighlightsDocument11 pagesUnited Spirits: Performance HighlightsAngel BrokingNo ratings yet

- DoubleDragon Final Domestic ProspectusDocument528 pagesDoubleDragon Final Domestic ProspectusKeith GarridoNo ratings yet

- Mining & Investment Latin America Summit 2016Document12 pagesMining & Investment Latin America Summit 2016eduardoleonsNo ratings yet

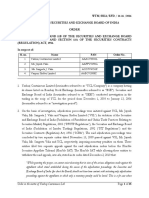

- Order in Respect of Yashraj Containeurs Limited, Mr. Jayesh Valia, Ms. Sangeeta J. Valia and Vasparr Shelter LimitedDocument15 pagesOrder in Respect of Yashraj Containeurs Limited, Mr. Jayesh Valia, Ms. Sangeeta J. Valia and Vasparr Shelter LimitedShyam SunderNo ratings yet

- Bajaj Holding - Initiating Coverage - 250221Document14 pagesBajaj Holding - Initiating Coverage - 250221Vivek BansalNo ratings yet

- SIP PROJECT REPORT FOR College RealDocument60 pagesSIP PROJECT REPORT FOR College RealTanaya GhosalNo ratings yet

- CORPORATION CODE OF THE PHILIPPINES SUMMARYDocument61 pagesCORPORATION CODE OF THE PHILIPPINES SUMMARYBing MendozaNo ratings yet

- Course Materials BAFINMAX Week2Document6 pagesCourse Materials BAFINMAX Week2emmanvillafuerteNo ratings yet

- Thailand'S: Top Local KnowledgeDocument10 pagesThailand'S: Top Local KnowledgebodaiNo ratings yet

- Sikkim Manipal University 3 Semester Fall 2010Document14 pagesSikkim Manipal University 3 Semester Fall 2010Dilipk86No ratings yet

- Dabur Financial Marketing AnalysisDocument63 pagesDabur Financial Marketing AnalysisAbhishek Kr. MishraNo ratings yet