You might also like

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Draft Scope Riverhead Logistics CenterDocument20 pagesDraft Scope Riverhead Logistics CenterRiverheadLOCALNo ratings yet

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Riverhead Budget Presentation March 22, 2022Document14 pagesRiverhead Budget Presentation March 22, 2022RiverheadLOCALNo ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- RXR/GGV Qualified & Eligible Documents (Final 09.26.22)Document23 pagesRXR/GGV Qualified & Eligible Documents (Final 09.26.22)RiverheadLOCALNo ratings yet

- Riverhead Town Board Comprehensive Plan Status Discussion Feb. 17, 2022Document30 pagesRiverhead Town Board Comprehensive Plan Status Discussion Feb. 17, 2022RiverheadLOCALNo ratings yet

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- AKRF Public Outreach Report AttachmentsDocument126 pagesAKRF Public Outreach Report AttachmentsRiverheadLOCALNo ratings yet

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Riverhead Town Proposed Battery Energy Storage CodeDocument10 pagesRiverhead Town Proposed Battery Energy Storage CodeRiverheadLOCALNo ratings yet

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- N.Y. Downtown Revitalization Initiative Round Five GuidebookDocument38 pagesN.Y. Downtown Revitalization Initiative Round Five GuidebookRiverheadLOCALNo ratings yet

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Robert E. KernDocument3 pagesRobert E. KernRiverheadLOCALNo ratings yet

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- 2022 - 03 - 16 - EPCAL Resolution & Letter AgreementDocument9 pages2022 - 03 - 16 - EPCAL Resolution & Letter AgreementRiverheadLOCALNo ratings yet

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Kenneth RothwellDocument5 pagesKenneth RothwellRiverheadLOCALNo ratings yet

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Juan Micieli-MartinezDocument3 pagesJuan Micieli-MartinezRiverheadLOCALNo ratings yet

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Catherine KentDocument7 pagesCatherine KentRiverheadLOCALNo ratings yet

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

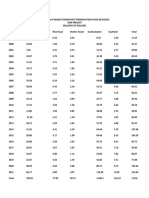

- Peconic Bay Region Community Preservation Fund Revenues 1999-2021Document1 pagePeconic Bay Region Community Preservation Fund Revenues 1999-2021RiverheadLOCALNo ratings yet

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- Yvette AguiarDocument10 pagesYvette AguiarRiverheadLOCALNo ratings yet

- Aguiar-Kent Campaign Finance Report 32-Day Pre GeneralDocument2 pagesAguiar-Kent Campaign Finance Report 32-Day Pre GeneralRiverheadLOCALNo ratings yet

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Riverhead Town Police Monthly Report July 2021Document6 pagesRiverhead Town Police Monthly Report July 2021RiverheadLOCALNo ratings yet

- Riverhead Town Police Report, August 2021Document6 pagesRiverhead Town Police Report, August 2021RiverheadLOCALNo ratings yet

- Evelyn Hobson-Womack Campaign Finance DisclosureDocument3 pagesEvelyn Hobson-Womack Campaign Finance DisclosureRiverheadLOCALNo ratings yet

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- Old Steeple Church Time CapsuleDocument4 pagesOld Steeple Church Time CapsuleRiverheadLOCALNo ratings yet

- League of Women Voters of NYS 2021 Voters Guide: Ballot PropositionsDocument2 pagesLeague of Women Voters of NYS 2021 Voters Guide: Ballot PropositionsRiverheadLOCAL67% (3)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Riverhead Town State of Emergency Order Issued May 12, 2021Document3 pagesRiverhead Town State of Emergency Order Issued May 12, 2021RiverheadLOCAL100% (1)

- 2021 General Election - Suffolk County Sample Ballot BookletDocument154 pages2021 General Election - Suffolk County Sample Ballot BookletRiverheadLOCALNo ratings yet

- Town of Southampton Police Reform PlanDocument308 pagesTown of Southampton Police Reform PlanRiverheadLOCALNo ratings yet

- Riverhead Town Marijuana SurveyDocument44 pagesRiverhead Town Marijuana SurveyRiverheadLOCALNo ratings yet

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Town of Riverhead Draft Solid Waste Management PlanDocument73 pagesTown of Riverhead Draft Solid Waste Management PlanRiverheadLOCALNo ratings yet

- Riverhead Police Reform Plan - FinalDocument96 pagesRiverhead Police Reform Plan - FinalRiverheadLOCALNo ratings yet

- "The Case of The DIsappering Landfill, or To Mine or Not To Mine" by Carl E. Fritz JR., PEDocument10 pages"The Case of The DIsappering Landfill, or To Mine or Not To Mine" by Carl E. Fritz JR., PERiverheadLOCALNo ratings yet

- Turtles of New York StateDocument2 pagesTurtles of New York StateRiverheadLOCALNo ratings yet

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- 2021-2022 Proposed Budget SummaryDocument2 pages2021-2022 Proposed Budget SummaryRiverheadLOCALNo ratings yet

- Town of Riverhead Railroad Street TOD RedevelopmentDocument54 pagesTown of Riverhead Railroad Street TOD RedevelopmentRiverheadLOCALNo ratings yet

- MathTextbooks9 12Document64 pagesMathTextbooks9 12Andrew0% (1)

- What Is Innovation A ReviewDocument33 pagesWhat Is Innovation A ReviewAnonymous EnIdJONo ratings yet

- Case Digest - de Roy Vs CoaDocument2 pagesCase Digest - de Roy Vs CoaLei Lei LeiNo ratings yet

- Letter Writing - Task1Document5 pagesLetter Writing - Task1gutha babuNo ratings yet

- 7A Detailed Lesson Plan in Health 7 I. Content Standard: Teacher's Activity Students' ActivityDocument10 pages7A Detailed Lesson Plan in Health 7 I. Content Standard: Teacher's Activity Students' ActivityLeizel C. LeonidoNo ratings yet

- EmanDocument3 pagesEmanCh NawazNo ratings yet

- Doloran Auxilliary PrayersDocument4 pagesDoloran Auxilliary PrayersJosh A.No ratings yet

- NursesExperiencesofGriefFollowing28 8 2017thepublishedDocument14 pagesNursesExperiencesofGriefFollowing28 8 2017thepublishedkathleen PerezNo ratings yet

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Exercise On Relative ClausesDocument5 pagesExercise On Relative ClausesSAmuel QuinteroNo ratings yet

- Dribssa Beyene Security Sector Reform Paradox Somalia PublishedDocument29 pagesDribssa Beyene Security Sector Reform Paradox Somalia PublishedNanny KebedeNo ratings yet

- Crim Pro Exam Sheet at A Glance.Document5 pagesCrim Pro Exam Sheet at A Glance.Heather Kinsaul Foster80% (5)

- NHÓM ĐỘNG TỪ BẤT QUY TẮCDocument4 pagesNHÓM ĐỘNG TỪ BẤT QUY TẮCNhựt HàoNo ratings yet

- Reading8 PilkingtonDocument8 pagesReading8 Pilkingtonab_amyNo ratings yet

- OITE - MCQ S QuestionsFinal2011Document67 pagesOITE - MCQ S QuestionsFinal2011KatKut99100% (7)

- Virtue EpistemologyDocument32 pagesVirtue EpistemologyJorge Torres50% (2)

- SuratiDocument2 pagesSuratiTariq Mehmood TariqNo ratings yet

- Waterfront Development Goals and ObjectivesDocument2 pagesWaterfront Development Goals and ObjectivesShruthi Thakkar100% (1)

- Use of ICT in School AdministartionDocument32 pagesUse of ICT in School AdministartionSyed Ali Haider100% (1)

- "International Finance": A Project Submitted ToDocument6 pages"International Finance": A Project Submitted ToAkshay HarekarNo ratings yet

- Module 4 Business EthicsDocument4 pagesModule 4 Business EthicsddddddaaaaeeeeNo ratings yet

- A Study On Mistakes and Errors in Consecutive Interpretation From Vietnamese To English. Dang Huu Chinh. Qhf.1Document38 pagesA Study On Mistakes and Errors in Consecutive Interpretation From Vietnamese To English. Dang Huu Chinh. Qhf.1Kavic100% (2)

- Quantile Regression (Final) PDFDocument22 pagesQuantile Regression (Final) PDFbooianca100% (1)

- Blue Mountain Coffee Case (ADBUDG)Document16 pagesBlue Mountain Coffee Case (ADBUDG)Nuria Sánchez Celemín100% (1)

- Parallels of Stoicism and KalamDocument95 pagesParallels of Stoicism and KalamLDaggersonNo ratings yet

- Magtajas vs. PryceDocument3 pagesMagtajas vs. PryceRoyce PedemonteNo ratings yet

- Rath'S Lectures: Longevity Related Notes On Vimsottari DasaDocument5 pagesRath'S Lectures: Longevity Related Notes On Vimsottari DasasudhinnnNo ratings yet

- Roman Catholic Bishop of Jaro v. Dela PenaDocument2 pagesRoman Catholic Bishop of Jaro v. Dela PenaBeltran KathNo ratings yet

- PPH CasestudyDocument45 pagesPPH CasestudyRona Mae PangilinanNo ratings yet

- Reflection (The We Entrepreneur)Document2 pagesReflection (The We Entrepreneur)Marklein DumangengNo ratings yet

- GEHealthcare Brochure - Discovery CT590 RT PDFDocument12 pagesGEHealthcare Brochure - Discovery CT590 RT PDFAnonymous ArdclHUONo ratings yet

- 2019 Business Credit with no Personal Guarantee: Get over 200K in Business Credit without using your SSNFrom Everand2019 Business Credit with no Personal Guarantee: Get over 200K in Business Credit without using your SSNRating: 4.5 out of 5 stars4.5/5 (3)

- These are the Plunderers: How Private Equity Runs—and Wrecks—AmericaFrom EverandThese are the Plunderers: How Private Equity Runs—and Wrecks—AmericaRating: 4.5 out of 5 stars4.5/5 (14)

- Creating Shareholder Value: A Guide For Managers And InvestorsFrom EverandCreating Shareholder Value: A Guide For Managers And InvestorsRating: 4.5 out of 5 stars4.5/5 (8)

- These Are the Plunderers: How Private Equity Runs—and Wrecks—AmericaFrom EverandThese Are the Plunderers: How Private Equity Runs—and Wrecks—AmericaRating: 3.5 out of 5 stars3.5/5 (8)

- John D. Rockefeller on Making Money: Advice and Words of Wisdom on Building and Sharing WealthFrom EverandJohn D. Rockefeller on Making Money: Advice and Words of Wisdom on Building and Sharing WealthRating: 4 out of 5 stars4/5 (20)

- The Six Secrets of Raising Capital: An Insider's Guide for EntrepreneursFrom EverandThe Six Secrets of Raising Capital: An Insider's Guide for EntrepreneursRating: 4.5 out of 5 stars4.5/5 (8)

- Summary of The Black Swan: by Nassim Nicholas Taleb | Includes AnalysisFrom EverandSummary of The Black Swan: by Nassim Nicholas Taleb | Includes AnalysisRating: 5 out of 5 stars5/5 (6)