You might also like

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5795)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Oct. 31 CineworldDocument96 pagesOct. 31 CineworldTHROnlineNo ratings yet

- FM Se6 SolutionsDocument39 pagesFM Se6 SolutionsOmar ManuelNo ratings yet

- Prelim Exam - Intermediate AccountingDocument4 pagesPrelim Exam - Intermediate AccountingLea Gabrielle Fariola0% (1)

- Actgfr Group 3 Chapter 8 Problem 8-6Document24 pagesActgfr Group 3 Chapter 8 Problem 8-6KrizahMarieCaballeroNo ratings yet

- Commercial Loan StructureDocument15 pagesCommercial Loan StructureSandesh GurungNo ratings yet

- Liability and ProvisionDocument45 pagesLiability and ProvisionDenise RoqueNo ratings yet

- Conservative Approach To Working Capital Financing: Financing Strategy in EquationDocument4 pagesConservative Approach To Working Capital Financing: Financing Strategy in Equationshamel marohomNo ratings yet

- Elite HARP Open Access ReliefDocument4 pagesElite HARP Open Access ReliefAccessLendingNo ratings yet

- Hybrid AnnuityDocument11 pagesHybrid AnnuitySumitAggarwal100% (1)

- PMC Application - MAY08Document17 pagesPMC Application - MAY08Nathan WilliamsNo ratings yet

- Credit Assessment of Housing Loans in Australia: Data Compiled by Dr. D. Sreenivasa CharyDocument45 pagesCredit Assessment of Housing Loans in Australia: Data Compiled by Dr. D. Sreenivasa Charysaumya tiwariNo ratings yet

- PK14 NotesDocument22 pagesPK14 NotesContessa PetriniNo ratings yet

- City Limits Magazine, March 1997 IssueDocument40 pagesCity Limits Magazine, March 1997 IssueCity Limits (New York)No ratings yet

- Real Estate Test 2 ReviewDocument19 pagesReal Estate Test 2 Reviewcarechung1900100% (1)

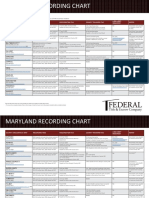

- Maryland Transfer and Recordation Tax Table (2020)Document2 pagesMaryland Transfer and Recordation Tax Table (2020)Federal Title & Escrow CompanyNo ratings yet

- FwisdDocument31 pagesFwisdJenLynnNo ratings yet

- Secondary Market Trade FinanceDocument11 pagesSecondary Market Trade FinanceAlex SoonNo ratings yet

- Muddy Waters Capital LLC: Director of Research: Carson C. BlockDocument34 pagesMuddy Waters Capital LLC: Director of Research: Carson C. BlockYash BhojwaniNo ratings yet

- Axial - CEO Guide To Debt FinancingDocument29 pagesAxial - CEO Guide To Debt FinancingcubanninjaNo ratings yet

- Statement of Financial Position Lecture 2Document3 pagesStatement of Financial Position Lecture 2AG VenturesNo ratings yet

- Intermediate Accounting IFRS 4e - 2021 (Donald E. Kieso 2021-1047-1089Document43 pagesIntermediate Accounting IFRS 4e - 2021 (Donald E. Kieso 2021-1047-1089FINNA HABIBATUSNo ratings yet

- Annuity, Sinking Fund, AmortizationDocument6 pagesAnnuity, Sinking Fund, AmortizationClydeLisboaNo ratings yet

- Subprime Mortgage CrisisDocument35 pagesSubprime Mortgage CrisisParaggNo ratings yet

- Financing and Prob CompDocument31 pagesFinancing and Prob CompRyan Joseph MagtibayNo ratings yet

- Cooperative Banking in Kerala Revamping The Role of Kerala BankDocument96 pagesCooperative Banking in Kerala Revamping The Role of Kerala Banksuryanellikkunnam2No ratings yet

- Steel NewsDocument32 pagesSteel NewsMoez MoezNo ratings yet

- Chapter 09 Testbank - StaticDocument52 pagesChapter 09 Testbank - StaticAlan ZhangNo ratings yet

- DBP Vs Court of Appeals - GR No 138703Document14 pagesDBP Vs Court of Appeals - GR No 138703Christia Sandee SuanNo ratings yet

- BKPloanapplicationDocument3 pagesBKPloanapplicationcunninghumNo ratings yet

- "Affordable Housing in Jaipur": A Report OnDocument47 pages"Affordable Housing in Jaipur": A Report OnAr Mukul SwamiNo ratings yet