You might also like

- Cheatsheet Supervised LearningDocument4 pagesCheatsheet Supervised LearningAmar Kumar100% (1)

- ARIMA Modelling and Forecasting: By: Amar KumarDocument22 pagesARIMA Modelling and Forecasting: By: Amar KumarAmar Kumar100% (1)

- Its About KIDS: Information Summary About Incredible Institute in PanvanDocument13 pagesIts About KIDS: Information Summary About Incredible Institute in PanvanAmar KumarNo ratings yet

- 12 Week A YearDocument9 pages12 Week A YearAmar Kumar67% (3)

- Random ForestDocument13 pagesRandom ForestAmar KumarNo ratings yet

- Rotation Shifts - SCNDocument6 pagesRotation Shifts - SCNAmar KumarNo ratings yet

- SAP MSS EHP6 POWL Based Leave Approval Refresh ..Document4 pagesSAP MSS EHP6 POWL Based Leave Approval Refresh ..Amar KumarNo ratings yet

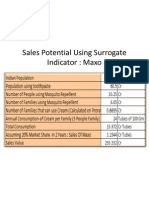

- Sales Potential Using Surrogate Indicator: MaxoDocument1 pageSales Potential Using Surrogate Indicator: MaxoAmar KumarNo ratings yet

- SAP Travel Management ..Document23 pagesSAP Travel Management ..Amar Kumar100% (1)

- EHP 5 New ProcurementiDocument5 pagesEHP 5 New ProcurementimkhicharNo ratings yet

- What Is Data ScienceDocument8 pagesWhat Is Data ScienceAmar KumarNo ratings yet

- Ifsc-Code of Icici Bank Branches in IndiaDocument10,725 pagesIfsc-Code of Icici Bank Branches in IndiaVenkatachalam KolandhasamyNo ratings yet

- Templates: Your Own Sub HeadlineDocument22 pagesTemplates: Your Own Sub HeadlineAmar KumarNo ratings yet

- QM OverviewDocument16 pagesQM Overviewrvk386No ratings yet

- Glimpse CertificateDocument1 pageGlimpse CertificateAmar KumarNo ratings yet

- LSCM: Individual Assignment-Analysis of IBM Global Supply ChainDocument7 pagesLSCM: Individual Assignment-Analysis of IBM Global Supply ChainAmar Kumar100% (1)

- SDM Presentation - Sales PotentialDocument6 pagesSDM Presentation - Sales PotentialAmar KumarNo ratings yet

- SPIL CaseDocument3 pagesSPIL CaseAmar KumarNo ratings yet

- Bright Engg CompDocument6 pagesBright Engg CompAmar KumarNo ratings yet

- Channel PartnerDocument7 pagesChannel PartnerAmar Kumar100% (1)

- Amar Kumar G12007 Ruchika GuptaDocument10 pagesAmar Kumar G12007 Ruchika GuptaAmar KumarNo ratings yet

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Boston ChickenDocument4 pagesBoston ChickenSaurabh SinghalNo ratings yet

- Market Risk Premium PDFDocument3 pagesMarket Risk Premium PDFmelinaguimaraesNo ratings yet

- Pulau Carey KenangaDocument17 pagesPulau Carey KenangaAzim FauziNo ratings yet

- Agile - 11 - A - Property HoldingsDocument211 pagesAgile - 11 - A - Property HoldingsMuteba NgongaNo ratings yet

- BOI - Promoting Investments Through ServicingDocument15 pagesBOI - Promoting Investments Through ServicingAnonymous yKUdPvwjNo ratings yet

- Top Ten Pitch Tips: Contact: Patrick Lor / Pat@lor - VC / WWW - Lor.vcDocument9 pagesTop Ten Pitch Tips: Contact: Patrick Lor / Pat@lor - VC / WWW - Lor.vcscribd2601RNo ratings yet

- ACCT 1005 Worksheet 1 Selected Solutions 2016 Practice QuestionsDocument2 pagesACCT 1005 Worksheet 1 Selected Solutions 2016 Practice QuestionsChan SynergisticNo ratings yet

- Freeport-McMoRan Annual Report 2018Document136 pagesFreeport-McMoRan Annual Report 2018kennygNo ratings yet

- Prospectus and Statement in Lieu of Prospectus:: How It Works (Example)Document13 pagesProspectus and Statement in Lieu of Prospectus:: How It Works (Example)Satyam PathakNo ratings yet

- Lecture 6: Valuation of Bonds and SharesDocument12 pagesLecture 6: Valuation of Bonds and SharesHabibullah SarkerNo ratings yet

- Rnis College of Financial Planning - 15 Mock-Test - Module-IVDocument10 pagesRnis College of Financial Planning - 15 Mock-Test - Module-IVAbhilash ParakhNo ratings yet

- Average Cost MethodDocument3 pagesAverage Cost MethodRaja MonemNo ratings yet

- Difference Between Large Mid Small Cap FundsDocument14 pagesDifference Between Large Mid Small Cap FundsNaresh KotrikeNo ratings yet

- Hedge Fund Book V3Document197 pagesHedge Fund Book V3http://besthedgefund.blogspot.comNo ratings yet

- Questions AFARDocument12 pagesQuestions AFARKatrina youngNo ratings yet

- Cash Flow Statement Disclosures A Study of Banking Companies in Bangladesh.Document18 pagesCash Flow Statement Disclosures A Study of Banking Companies in Bangladesh.MD. REZAYA RABBINo ratings yet

- GMR Finance ReportDocument14 pagesGMR Finance ReportsaranshjainNo ratings yet

- 1daily DerivativesDocument3 pages1daily DerivativesGauriGanNo ratings yet

- Answwr of Quiz 5 (MBA)Document2 pagesAnswwr of Quiz 5 (MBA)Wael_Barakat_3179No ratings yet

- May 2011 Strategic Financial ManagementDocument10 pagesMay 2011 Strategic Financial ManagementchandreshNo ratings yet

- Option Valuation ModelsDocument37 pagesOption Valuation ModelssakshiNo ratings yet

- Financial ManagementDocument6 pagesFinancial ManagementAshish PrajapatiNo ratings yet

- Annual Reports - 2013 - Malaysia - Airports - Holding - Berhad PDFDocument373 pagesAnnual Reports - 2013 - Malaysia - Airports - Holding - Berhad PDFAnonymous 05Ra5rgNo ratings yet

- Act 701 Assignment 2Document3 pagesAct 701 Assignment 2Nahid HawkNo ratings yet

- Consolidated Balance Sheet of Reliance Industries: - in Rs. Cr.Document58 pagesConsolidated Balance Sheet of Reliance Industries: - in Rs. Cr.rotiNo ratings yet

- Approaches To Valuation Discounted Cashflow Relative Real OptionDocument29 pagesApproaches To Valuation Discounted Cashflow Relative Real OptionJNo ratings yet

- The Cost of Capital: © 2019 Pearson Education LTDDocument8 pagesThe Cost of Capital: © 2019 Pearson Education LTDLeanne TehNo ratings yet

- Existing International Arrangements, Globalization and Foreign Investment, Introduction To FDIDocument30 pagesExisting International Arrangements, Globalization and Foreign Investment, Introduction To FDIpranati sharmaNo ratings yet

- 54594bos43759 p3 PDFDocument23 pages54594bos43759 p3 PDFWaleed Bin RaoufNo ratings yet