Japanese Bonds sell off

Macro Economic Research May 2013

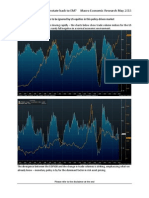

When the BoJ announced their stimulus programme on the 4th of April, Japanese bonds spiked higher in anticipation of the $75bn a month of purchases, with yields reaching as low as 33 basis points. Yields are currently 85bps, having sold off a massive 35bps in the last 3 trading days.

The 10 year bond future, after many years of slumber, has suddenly rediscovered volatility.

Japanese financial intermediaries collectively had some 30% of their assets invested directly in their governments bonds as at 12/2012 (BoJ Flow of Funds). Japanese households have indirect exposures (mainly via their life policies and pension funds) of more than 20% of their

Please refer to the disclaimer at the end

Japanese Bonds sell off

Macro Economic Research May 2013

financial assets (the second largest asset after an incredible 55% of financial assets in bank deposits). That bonds are being sold off despite the on-going massive intervention is a clear sign that the BoJs 2% inflation in 2 years target is gaining credibility. I believe the biggest disconnect in the Japanese market is an inability to answer the question If inflation gets to 2% what should the real yield on bonds be? Real yields based on the 10 year bond yield less the YoY CPI are currently 176bps for JGBs (shown below) and 44bps for USTs. JGB real yields have briefly spiked negative only twice. A negative real yield of -0.5% and a 2% CPI still imply a massive sell off in JGBs. A similar question can be asked for US bonds, again highlighting the difficulties of pricing in the end of QE.

I believe that given the massive skew in existing positioning in financial assets by households and institutions, they must rotate out of bonds and bank deposits into equities and foreign securities. Every dip in equities will be bought, every rally in the bonds sold, until the credibility of the BoJs 2% in 2 years target is established or destroyed.

Kevin Cousins is a portfolio manager at Brait Capital Management Limited. ("BraitCM"). This article is prepared by Kevin as an outside business activity. As such, BraitCM does not review or approve materials presented herein. The opinions and any recommendations expressed in this article are those of the author and do not reflect the opinions or recommendations of BraitCM. None of the information or opinions expressed in this article constitutes a solicitation for the purchase or sale of any security or other instrument. Nothing in this article constitutes investment advice and any recommendations that may be contained herein have not been based upon a consideration of the investment objectives, financial situation or particular needs of any specific recipient. Any purchase or sale activity in any securities or other instrument should be based upon your own analysis and conclusions. Either BraitCM or Kevin Cousins may hold or control long or short positions in the securities or instruments mentioned.

Please refer to the disclaimer at the end

You might also like

- Walt Disney Yen FinancingDocument10 pagesWalt Disney Yen FinancingAndy100% (3)

- Beyond Greed and FearDocument279 pagesBeyond Greed and Fearreviur100% (13)

- Free Algo Strategy PDFDocument31 pagesFree Algo Strategy PDFEnrique Blanco100% (2)

- Crypto Research Report June 2020 ENGDocument61 pagesCrypto Research Report June 2020 ENGForkLog0% (1)

- Chapter-Iv: Forfeiture and Surrender of SharesDocument13 pagesChapter-Iv: Forfeiture and Surrender of SharesKhalil AhmadNo ratings yet

- RJR NabiscoDocument17 pagesRJR Nabiscodanielcid100% (1)

- Negotiable Instruments Law Bar QnADocument22 pagesNegotiable Instruments Law Bar QnArgtan3100% (4)

- Japan The End of The Beginning 2013 04Document8 pagesJapan The End of The Beginning 2013 04kcousinsNo ratings yet

- Evolving Bond MarketDocument9 pagesEvolving Bond MarketcoolNo ratings yet

- Japan Follow Up Institutional Exposures 2013 05Document2 pagesJapan Follow Up Institutional Exposures 2013 05kcousinsNo ratings yet

- The World Economy... - 23/6/2010Document3 pagesThe World Economy... - 23/6/2010Rhb InvestNo ratings yet

- Blog Nico 10 November 201411Document17 pagesBlog Nico 10 November 201411Aris SunaryoNo ratings yet

- (LGT) 20210316 - DRU - Sector RotationDocument3 pages(LGT) 20210316 - DRU - Sector RotationRuehYinn YapNo ratings yet

- La Fine Del QeDocument5 pagesLa Fine Del QemercatoliberoNo ratings yet

- Bank of JapanDocument4 pagesBank of JapanimvavNo ratings yet

- Global Macro Commentary July 14Document2 pagesGlobal Macro Commentary July 14dpbasicNo ratings yet

- Monthly Outlook GoldDocument10 pagesMonthly Outlook GoldKapil KhandelwalNo ratings yet

- Bond Market Perspectives: The Yield Ascent ResumesDocument3 pagesBond Market Perspectives: The Yield Ascent Resumesapi-234126528No ratings yet

- Global Macro Commentary Nov 12Document2 pagesGlobal Macro Commentary Nov 12dpbasicNo ratings yet

- Tracking The World Economy... - 23/08/2010Document3 pagesTracking The World Economy... - 23/08/2010Rhb InvestNo ratings yet

- General Knowledge Today - 109Document2 pagesGeneral Knowledge Today - 109niranjan_meharNo ratings yet

- Where Do They Stand?: PerspectiveDocument8 pagesWhere Do They Stand?: Perspectiverajesh palNo ratings yet

- Optimal Fiscal Policy Rule For Achieving Fiscal Sustainability: A Japanese Case StudyDocument19 pagesOptimal Fiscal Policy Rule For Achieving Fiscal Sustainability: A Japanese Case StudyADBI PublicationsNo ratings yet

- Asia Maxima (Delirium) - 3Q14 20140703Document100 pagesAsia Maxima (Delirium) - 3Q14 20140703Hans WidjajaNo ratings yet

- Global Macro Commentary August 19 - Raging (Bond) BullDocument3 pagesGlobal Macro Commentary August 19 - Raging (Bond) BulldpbasicNo ratings yet

- The Federal Reserve Dont Let It Be MisunderstoodDocument18 pagesThe Federal Reserve Dont Let It Be MisunderstoodZerohedgeNo ratings yet

- UBS DEC Letter enDocument6 pagesUBS DEC Letter enDim moNo ratings yet

- Tracking The World Economy... - 22/7/2010Document2 pagesTracking The World Economy... - 22/7/2010Rhb InvestNo ratings yet

- Why Real Yields Matter - Pictet Asset ManagementDocument7 pagesWhy Real Yields Matter - Pictet Asset ManagementLOKE SENG ONNNo ratings yet

- Tracking The World Economy... - 09/09/2010Document2 pagesTracking The World Economy... - 09/09/2010Rhb InvestNo ratings yet

- Credit SpreadsDocument6 pagesCredit Spreadsspps140899No ratings yet

- Global Macro Commentary April 2Document3 pagesGlobal Macro Commentary April 2dpbasicNo ratings yet

- Global Macro Commentary Dec 4Document3 pagesGlobal Macro Commentary Dec 4dpbasicNo ratings yet

- Tracking The World Economy... - 13/08/2010Document3 pagesTracking The World Economy... - 13/08/2010Rhb InvestNo ratings yet

- Tracking The World Economy... - 13/12/2010Document3 pagesTracking The World Economy... - 13/12/2010Rhb InvestNo ratings yet

- Tracking The World Economy.. - 08/10/2010Document2 pagesTracking The World Economy.. - 08/10/2010Rhb InvestNo ratings yet

- Screenshot 2022-11-18 at 8.51.39 PM PDFDocument51 pagesScreenshot 2022-11-18 at 8.51.39 PM PDFJupiter's StringNo ratings yet

- General Research PDFDocument4 pagesGeneral Research PDFGeorge LernerNo ratings yet

- What Are Japanese Government BondsDocument2 pagesWhat Are Japanese Government Bondsrohit keluskarNo ratings yet

- Econ - An Afternoon With Jim Rogers - 2009!02!04 Maybank-IB ETDocument3 pagesEcon - An Afternoon With Jim Rogers - 2009!02!04 Maybank-IB ETwonderwNo ratings yet

- Global Macro Commentary October 9Document2 pagesGlobal Macro Commentary October 9dpbasicNo ratings yet

- India Market Outlook Aug 2013Document4 pagesIndia Market Outlook Aug 2013sindu_lawrenceNo ratings yet

- Etm 2011 8 22 33Document1 pageEtm 2011 8 22 33Saurabh DardaNo ratings yet

- Weekly Market Commentary 6-24-13Document3 pagesWeekly Market Commentary 6-24-13Stephen GierlNo ratings yet

- Global Macro Commentary Feb 26Document2 pagesGlobal Macro Commentary Feb 26dpbasicNo ratings yet

- Running Head: ECONOMICSDocument12 pagesRunning Head: ECONOMICSRajshekhar BoseNo ratings yet

- Global Macro Commentary September 2Document2 pagesGlobal Macro Commentary September 2dpbasicNo ratings yet

- The Pensford Letter - 8.26.13Document6 pagesThe Pensford Letter - 8.26.13Pensford FinancialNo ratings yet

- Niveshak Sept 2012Document24 pagesNiveshak Sept 2012Niveshak - The InvestorNo ratings yet

- Economics Club: Article Series - 2Document4 pagesEconomics Club: Article Series - 2Rahul SharmaNo ratings yet

- GreyOwl Q4 LetterDocument6 pagesGreyOwl Q4 LetterMarko AleksicNo ratings yet

- 12 - 16th February 2008 (160208)Document5 pages12 - 16th February 2008 (160208)Chaanakya_cuimNo ratings yet

- The World Economy... - 10/6/2010Document2 pagesThe World Economy... - 10/6/2010Rhb InvestNo ratings yet

- Stock Market Crash Survival GuideDocument18 pagesStock Market Crash Survival GuideFlorian MlNo ratings yet

- Mutual Fund Review: Equity MarketDocument15 pagesMutual Fund Review: Equity MarketHariprasad ManchiNo ratings yet

- Market Insight Q3FY12 RBI Policy Review Jan12Document3 pagesMarket Insight Q3FY12 RBI Policy Review Jan12poojarajeswariNo ratings yet

- Economist-Insights 1 JulyDocument2 pagesEconomist-Insights 1 JulybuyanalystlondonNo ratings yet

- LEI230920 BDocument11 pagesLEI230920 Bpderby1No ratings yet

- Japan Asia AugustDocument27 pagesJapan Asia AugustIronHarborNo ratings yet

- The World Economy - 29/06/2010Document2 pagesThe World Economy - 29/06/2010Rhb InvestNo ratings yet

- An Smu Economics Intelligence Club ProductionDocument10 pagesAn Smu Economics Intelligence Club ProductionSMU Political-Economics Exchange (SPEX)No ratings yet

- The World Economy... - 21/004/2010Document2 pagesThe World Economy... - 21/004/2010Rhb InvestNo ratings yet

- BondMarketPerspectives 060215Document4 pagesBondMarketPerspectives 060215dpbasicNo ratings yet

- Trading Strateg: April 2022 Pension Fund Rebalancing EstimatesDocument2 pagesTrading Strateg: April 2022 Pension Fund Rebalancing EstimatessirdquantsNo ratings yet

- The World Economy... - 10/08/2010Document2 pagesThe World Economy... - 10/08/2010Rhb InvestNo ratings yet

- 20130208Document40 pages20130208philline2009No ratings yet

- Common Sense Retirement Planning: Home, Savings and InvestmentFrom EverandCommon Sense Retirement Planning: Home, Savings and InvestmentNo ratings yet

- The True Risk StoryDocument25 pagesThe True Risk StorykcousinsNo ratings yet

- Chart Review - Can We Rotate Back To EM? Macro Economic Research May 2013Document4 pagesChart Review - Can We Rotate Back To EM? Macro Economic Research May 2013kcousinsNo ratings yet

- Situation Index Handbook 2014Document43 pagesSituation Index Handbook 2014kcousinsNo ratings yet

- Yen Impact On Corporates 2013 05Document2 pagesYen Impact On Corporates 2013 05kcousinsNo ratings yet

- 2011-07-31 Brait Multi StrategyDocument2 pages2011-07-31 Brait Multi StrategykcousinsNo ratings yet

- 2011-02-28 Brait Multi Strategy Fund OverviewDocument2 pages2011-02-28 Brait Multi Strategy Fund OverviewkcousinsNo ratings yet

- Double Dip 2010 05Document3 pagesDouble Dip 2010 05kcousinsNo ratings yet

- Motilal Oswal Securities Limited Analysis of Derivative and Stock MarketDocument104 pagesMotilal Oswal Securities Limited Analysis of Derivative and Stock MarketJitendra Virahyas100% (3)

- NV - Sewa Theodolite - MR Jundi PDFDocument1 pageNV - Sewa Theodolite - MR Jundi PDFZamruddin HambaliNo ratings yet

- Margin Jargon Cheat Sheet: BalanceDocument8 pagesMargin Jargon Cheat Sheet: Balancevalkar75No ratings yet

- Balhana Journal PDFDocument67 pagesBalhana Journal PDFSugeng Bintoko Sr.100% (2)

- Sap SD Sales or To PaymentDocument21 pagesSap SD Sales or To PaymentKrishna MoorthyNo ratings yet

- Covid 19 Impact On The Financial Services Sector PDFDocument13 pagesCovid 19 Impact On The Financial Services Sector PDFvishwanathNo ratings yet

- Jim Berg Tradingplantemplate PDFDocument126 pagesJim Berg Tradingplantemplate PDFAlvin100% (1)

- EO No. 226 - Omnibus Investments CodeDocument26 pagesEO No. 226 - Omnibus Investments CodeJen AnchetaNo ratings yet

- CH 10Document34 pagesCH 10PetersonNo ratings yet

- Wealth ManagementDocument3 pagesWealth ManagementAliasgar PatanwalaNo ratings yet

- Organizational Study of Hedge EquitiesDocument91 pagesOrganizational Study of Hedge EquitiesGopi Krishnan.nNo ratings yet

- Financial Intermediaries and Players Philippines Financial Intermediaries and PlayersDocument9 pagesFinancial Intermediaries and Players Philippines Financial Intermediaries and PlayersLeo-Alyssa Gregorio-CorporalNo ratings yet

- List of Regd Sub BrokersDocument435 pagesList of Regd Sub BrokersPramod RawalNo ratings yet

- TOS - UnbalancedbutterfliesDocument9 pagesTOS - UnbalancedbutterfliesthiendNo ratings yet

- Capital StrutureDocument27 pagesCapital StrutureSitaKumariNo ratings yet

- IPPTChap 012Document75 pagesIPPTChap 012CacaNo ratings yet

- On The Pricing of European SwaptionsDocument6 pagesOn The Pricing of European SwaptionsThomas GustafssonNo ratings yet

- 16th EPIRA Report Final - 05 July 2010Document59 pages16th EPIRA Report Final - 05 July 2010euroaccessNo ratings yet

- Beutel Goodman Canadian Equity Class F: Growth of 10,000 10-09-2009 - 10-09-2019 Morningstar Risk MeasuresDocument3 pagesBeutel Goodman Canadian Equity Class F: Growth of 10,000 10-09-2009 - 10-09-2019 Morningstar Risk MeasuresRoger SongNo ratings yet

- Analytical Study of Impact of FII On Indian Stock Market With Special Reference To BSE SENSEXDocument12 pagesAnalytical Study of Impact of FII On Indian Stock Market With Special Reference To BSE SENSEXtejaswijoshyula_b5No ratings yet

- MOA HavellsDocument86 pagesMOA Havellssm_rez1scribdNo ratings yet

- Cir v. Dakudao & Sons Inc.Document1 pageCir v. Dakudao & Sons Inc.Mico LrzNo ratings yet

- China Foods Limited 2017 PDFDocument275 pagesChina Foods Limited 2017 PDFAnastasiaNo ratings yet