You might also like

- Notice To The MarketDocument1 pageNotice To The MarketJBS RINo ratings yet

- Notice To The MarketDocument1 pageNotice To The MarketJBS RINo ratings yet

- Notice To The MarketDocument1 pageNotice To The MarketJBS RINo ratings yet

- JBS S.A. Releases Its 2016 Annual and Sustainability ReportDocument1 pageJBS S.A. Releases Its 2016 Annual and Sustainability ReportJBS RINo ratings yet

- 1Q17 Earnings PresentationDocument15 pages1Q17 Earnings PresentationJBS RINo ratings yet

- JBS S.A. Announces The Conclusion of Plumrose AcquisitionDocument1 pageJBS S.A. Announces The Conclusion of Plumrose AcquisitionJBS RINo ratings yet

- 1Q17 Financial StatementsDocument31 pages1Q17 Financial StatementsJBS RINo ratings yet

- 1Q17 Conference Call TranscriptDocument13 pages1Q17 Conference Call TranscriptJBS RINo ratings yet

- Minutes of The Board of Directors' Meeting Held On May 08, 2017Document2 pagesMinutes of The Board of Directors' Meeting Held On May 08, 2017JBS RINo ratings yet

- Release and FS 1Q17Document53 pagesRelease and FS 1Q17JBS RINo ratings yet

- Minutes of The Fiscal Council's Meeting Held On May 04, 2017Document2 pagesMinutes of The Fiscal Council's Meeting Held On May 04, 2017JBS RINo ratings yet

- Minutes of The Board of Directors' Meeting Held On May 05, 2017Document2 pagesMinutes of The Board of Directors' Meeting Held On May 05, 2017JBS RINo ratings yet

- Minutes of The Fiscal Council's Meeting Held On April 05, 2017Document5 pagesMinutes of The Fiscal Council's Meeting Held On April 05, 2017JBS RINo ratings yet

- JBS - Annual and Sustainability Report 2016Document144 pagesJBS - Annual and Sustainability Report 2016JBS RINo ratings yet

- MGMT Report FS 2015 (Reap 2017)Document95 pagesMGMT Report FS 2015 (Reap 2017)JBS RINo ratings yet

- MGMT Report FS 2016 (Reap 2017)Document97 pagesMGMT Report FS 2016 (Reap 2017)JBS RINo ratings yet

- REMOTE VOTING FORM OF OESM To Be Held On April 28, 2017Document5 pagesREMOTE VOTING FORM OF OESM To Be Held On April 28, 2017JBS RINo ratings yet

- JBS - ARCA - 2017 04 06 - Aprovao Reapresentao DFs 2015 e 2016 (JUCESP) EngDocument5 pagesJBS - ARCA - 2017 04 06 - Aprovao Reapresentao DFs 2015 e 2016 (JUCESP) EngJBS RINo ratings yet

- Minutes of The Board of Directors' Meeting Held On March 13, 2017Document4 pagesMinutes of The Board of Directors' Meeting Held On March 13, 2017JBS RINo ratings yet

- JBS Institutional Presentation Including 4Q16 and 2016 ResultsDocument24 pagesJBS Institutional Presentation Including 4Q16 and 2016 ResultsJBS RINo ratings yet

- 4Q16 and 2016 Earnings PresentationDocument21 pages4Q16 and 2016 Earnings PresentationJBS RINo ratings yet

- 4Q16 Conference Call TranscriptDocument16 pages4Q16 Conference Call TranscriptJBS RINo ratings yet

- MgmtReport FSDocument96 pagesMgmtReport FSJBS RINo ratings yet

- JBS - ARCF - 2017 03 10 - Aprovao DFs 4T2016 (Livro) MZT EngDocument4 pagesJBS - ARCF - 2017 03 10 - Aprovao DFs 4T2016 (Livro) MZT EngJBS RINo ratings yet

- MgmtReport FSDocument96 pagesMgmtReport FSJBS RINo ratings yet

- UntitledDocument4 pagesUntitledJBS RINo ratings yet

- Notice To The Market - Federal Police OperationDocument1 pageNotice To The Market - Federal Police OperationJBS RINo ratings yet

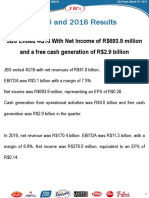

- 4Q16 and 2016 Earnings ReleaseDocument31 pages4Q16 and 2016 Earnings ReleaseJBS RI100% (1)

- MATERIAL FACT - JBS Announces The Acquisition of Plumrose USADocument2 pagesMATERIAL FACT - JBS Announces The Acquisition of Plumrose USAJBS RINo ratings yet

- Minutes of The Board of Directors' Meeting Held On February 23, 2017Document20 pagesMinutes of The Board of Directors' Meeting Held On February 23, 2017JBS RINo ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (894)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Grand StrategiesDocument7 pagesGrand StrategiesSeher NazNo ratings yet

- Little Black Book of Options Secrets AbDocument12 pagesLittle Black Book of Options Secrets AbRaju.KonduruNo ratings yet

- The Effect of Financial Leverage On Profitability and Risk of Restaurant FirmsDocument20 pagesThe Effect of Financial Leverage On Profitability and Risk of Restaurant Firmsmaine pamintuanNo ratings yet

- Form 16 of ANIT SINGHDocument5 pagesForm 16 of ANIT SINGHAnit SinghNo ratings yet

- 45Document9 pages45Anonymous yMOMM9bsNo ratings yet

- List of Investment BanksDocument10 pagesList of Investment BanksSKNYUYNo ratings yet

- Top stockbrokers in Chandigarh regionDocument5 pagesTop stockbrokers in Chandigarh regionKelly BaileyNo ratings yet

- Merchant Company and Enterprise in AndorraDocument9 pagesMerchant Company and Enterprise in AndorraKai SanNo ratings yet

- Currency Future & Option For StudentsDocument8 pagesCurrency Future & Option For StudentsAmit SinhaNo ratings yet

- Arbitrage Trade Analysis of Stock Trading in Bse and Nse - India InfolineDocument12 pagesArbitrage Trade Analysis of Stock Trading in Bse and Nse - India InfolineLOGIC SYSTEMSNo ratings yet

- Real Estate Investment Portfolio and Real Estate Investment Climate in Batangas ProvinceDocument9 pagesReal Estate Investment Portfolio and Real Estate Investment Climate in Batangas ProvinceIJARP PublicationsNo ratings yet

- Intellectual Property Rights and Hostile TakeoverDocument8 pagesIntellectual Property Rights and Hostile TakeoverDanNo ratings yet

- Adjusting EntriesDocument108 pagesAdjusting EntriesChristine Salvador100% (3)

- Working Capital Tulasi SeedsDocument22 pagesWorking Capital Tulasi SeedsVamsi SakhamuriNo ratings yet

- Indian Banking System OverviewDocument67 pagesIndian Banking System Overviewvandana_daki3941No ratings yet

- Writing The Business Plan IDG VenturesDocument9 pagesWriting The Business Plan IDG VentureswindevilNo ratings yet

- Top Executives of Major PSUs in IndiaDocument335 pagesTop Executives of Major PSUs in IndiaRishab WahalNo ratings yet

- Interim Order in The Matter of Aspen Nirman India LimitedDocument20 pagesInterim Order in The Matter of Aspen Nirman India LimitedShyam SunderNo ratings yet

- AIG's Dangerous Collapse - by Daniel R. Amerman, FSU Editoria..Document10 pagesAIG's Dangerous Collapse - by Daniel R. Amerman, FSU Editoria..Todd BengertNo ratings yet

- A Study On Life InsuranceDocument76 pagesA Study On Life Insurancepooja negiNo ratings yet

- CRM HSBCDocument26 pagesCRM HSBCRavi Shankar100% (1)

- America's New Robber Barons PDFDocument17 pagesAmerica's New Robber Barons PDFdasjo asmnjfNo ratings yet

- Manage ReceivablesDocument25 pagesManage ReceivablesBon Jovi0% (1)

- Faysal Bank Limited Was Incorporated in Pakistan On October 3rdDocument22 pagesFaysal Bank Limited Was Incorporated in Pakistan On October 3rdfahad pansotaNo ratings yet

- Maintenance CapexDocument2 pagesMaintenance CapexGaurav JainNo ratings yet

- Icici Bank LTDDocument8 pagesIcici Bank LTDAmit TripathiNo ratings yet

- Model Question Paper: EconomicsDocument3 pagesModel Question Paper: Economicssharathk916No ratings yet

- Dell Working CapitalDocument5 pagesDell Working CapitalSushil Kumar TripathyNo ratings yet

- Long-Term Asset and Liability ManagementDocument27 pagesLong-Term Asset and Liability ManagementImtiaz MasroorNo ratings yet