You might also like

- Awo, Part I by Awo Fa'lokun FatunmbiDocument7 pagesAwo, Part I by Awo Fa'lokun FatunmbiodeNo ratings yet

- Entity Level ControlsDocument45 pagesEntity Level ControlsNiraj AlltimeNo ratings yet

- Quality Assurance Plan - CivilDocument11 pagesQuality Assurance Plan - CivilDeviPrasadNathNo ratings yet

- Updated COSO Internal Control Framework FAQs Second Edition ProtivitiDocument29 pagesUpdated COSO Internal Control Framework FAQs Second Edition ProtivitiAgus Pugariyadi100% (1)

- Entity Level ControlsDocument11 pagesEntity Level ControlsEmmanuel DonNo ratings yet

- Hardening by Auditing: A Handbook for Measurably and Immediately Improving the Security Management of Any OrganizationFrom EverandHardening by Auditing: A Handbook for Measurably and Immediately Improving the Security Management of Any OrganizationNo ratings yet

- Purchasing, Inventory, and Cash Disbursements: Common Frauds and Internal ControlsFrom EverandPurchasing, Inventory, and Cash Disbursements: Common Frauds and Internal ControlsRating: 5 out of 5 stars5/5 (1)

- Comprehensive Manual of Internal Audit Practice and Guide: The Most Practical Guide to Internal Auditing PracticeFrom EverandComprehensive Manual of Internal Audit Practice and Guide: The Most Practical Guide to Internal Auditing PracticeRating: 5 out of 5 stars5/5 (1)

- Audit Manual Version 5Document247 pagesAudit Manual Version 5MahediNo ratings yet

- 2015 SOx Guidance FINAL PDFDocument35 pages2015 SOx Guidance FINAL PDFMiruna RaduNo ratings yet

- COSO Framework - DeloitteDocument130 pagesCOSO Framework - DeloitteAlexandre Santos100% (5)

- Evaluating Internal Control Systems PDFDocument65 pagesEvaluating Internal Control Systems PDFAnonymous cyExpb2No ratings yet

- IS Auditor - Process of Auditing: Information Systems Auditor, #1From EverandIS Auditor - Process of Auditing: Information Systems Auditor, #1No ratings yet

- COSO Internal Control - Integrated FrameworkDocument348 pagesCOSO Internal Control - Integrated FrameworkMuhammad Saeed Babar88% (16)

- Auditing Information Systems and Controls: The Only Thing Worse Than No Control Is the Illusion of ControlFrom EverandAuditing Information Systems and Controls: The Only Thing Worse Than No Control Is the Illusion of ControlNo ratings yet

- Internal Control Over Financial Reporting (ICFR) - ICFR Benchmarking Survey 2016 by PWCDocument32 pagesInternal Control Over Financial Reporting (ICFR) - ICFR Benchmarking Survey 2016 by PWCgong688665No ratings yet

- Mechanics of Materials 7th Edition Beer Johnson Chapter 6Document134 pagesMechanics of Materials 7th Edition Beer Johnson Chapter 6Riston Smith95% (96)

- COSO GuidanceDocument71 pagesCOSO GuidancemahmudtohaNo ratings yet

- 0015.3 Coso Icefr CompendiumDocument172 pages0015.3 Coso Icefr Compendiummanolo perezNo ratings yet

- Internal Control Guide Sep 2017 - DTTDocument186 pagesInternal Control Guide Sep 2017 - DTTspandan67% (3)

- COSO Training - DeloitteDocument180 pagesCOSO Training - DeloitteHossein Davani100% (4)

- SOX Testing TemplateDocument2 pagesSOX Testing Templatestl0042230No ratings yet

- Updated COSO Internal Control Framework FAQs Second Edition ProtivitiDocument29 pagesUpdated COSO Internal Control Framework FAQs Second Edition ProtivitiDavid Apaza Quenaya100% (1)

- COSO CROWE COSO Internal Control Integrated FrameworkDocument36 pagesCOSO CROWE COSO Internal Control Integrated Frameworkgirish sainiNo ratings yet

- Coso Internal Control Integrated Framework and AppendicesDocument194 pagesCoso Internal Control Integrated Framework and AppendicesDavid Apaza QuenayaNo ratings yet

- GTAG3 Audit KontinyuDocument37 pagesGTAG3 Audit KontinyujonisupriadiNo ratings yet

- ICFR Day 1Document70 pagesICFR Day 1Toni Triyulianto100% (1)

- Internal Controls Survey Report 2018Document24 pagesInternal Controls Survey Report 2018kunal butolaNo ratings yet

- Icfr ChklistDocument16 pagesIcfr Chklistananda_joshi5178100% (1)

- COSO Internal Control - Integrated Framework May 2013Document198 pagesCOSO Internal Control - Integrated Framework May 2013David Apaza Quenaya100% (9)

- Internal Control-Integrated FrameworkDocument34 pagesInternal Control-Integrated FrameworkInternational Consortium on Governmental Financial Management100% (1)

- White Paper - Good Practice Internal Audit Reports: April 2018Document16 pagesWhite Paper - Good Practice Internal Audit Reports: April 2018Anam Siddique100% (1)

- ABC Private Limited: Entity Level Controls (ELC)Document54 pagesABC Private Limited: Entity Level Controls (ELC)Macmilan Trevor Jamu100% (1)

- BCA Entity Level Controls Checklists Makingiteasy GoodDocument32 pagesBCA Entity Level Controls Checklists Makingiteasy Goodsarvjeet_kaushalNo ratings yet

- Illustrative ToolsDocument102 pagesIllustrative Toolsvivekan_kumarNo ratings yet

- English 8 q3 w1 6 FinalDocument48 pagesEnglish 8 q3 w1 6 FinalJedidiah NavarreteNo ratings yet

- The New COSO Framework Amanda HerronDocument32 pagesThe New COSO Framework Amanda HerronMohammed OsmanNo ratings yet

- COSO 2013 Framework Training - DeloitteDocument180 pagesCOSO 2013 Framework Training - DeloitteDavid Apaza QuenayaNo ratings yet

- ICFR StagesDocument10 pagesICFR StagesWajahat AliNo ratings yet

- IIA Maturity Model PDFDocument13 pagesIIA Maturity Model PDFZsL6231No ratings yet

- Coso Erm 2017Document44 pagesCoso Erm 2017Daniel Garcia100% (4)

- SawyersDocument3 pagesSawyersfaldo82550% (2)

- Ryff's Six-Factor Model of Psychological Well-BeingDocument7 pagesRyff's Six-Factor Model of Psychological Well-BeingYogi Sastrawan100% (1)

- COSO ERM Volume2Document40 pagesCOSO ERM Volume2rangel2475% (4)

- Audit Manual 2015 Single File PDFDocument776 pagesAudit Manual 2015 Single File PDFImmad AhmedNo ratings yet

- GAIT MethodologyDocument41 pagesGAIT MethodologyHerbert NgwaraiNo ratings yet

- COSO ERM FrameworkDocument15 pagesCOSO ERM FrameworkأسامةروميNo ratings yet

- Factsheet Internal Audit and Risk Management Functions Working TogetherDocument2 pagesFactsheet Internal Audit and Risk Management Functions Working TogetherFikri Haikal Mukhsin100% (1)

- Sarbanes-Oxley Section 404:: A Guide For Management by Internal Controls PractitionersDocument78 pagesSarbanes-Oxley Section 404:: A Guide For Management by Internal Controls Practitionersaamsantos_web50% (2)

- 2015 Leveraging COSO 3LODDocument32 pages2015 Leveraging COSO 3LODalfonsodzibNo ratings yet

- Post Public Exposure Version: Internal Control-Integrated FrameworkDocument194 pagesPost Public Exposure Version: Internal Control-Integrated FrameworkKaren Somcio60% (5)

- GTAG 3 Continuous Auditing 2nd EditionDocument30 pagesGTAG 3 Continuous Auditing 2nd EditionDede AndriNo ratings yet

- Audit Planning TakeawayDocument40 pagesAudit Planning TakeawayAmar Lal Nihalani100% (3)

- Practice Aid: Enterprise Risk Management: Guidance For Practical Implementation and Assessment, 2018From EverandPractice Aid: Enterprise Risk Management: Guidance For Practical Implementation and Assessment, 2018No ratings yet

- Internal Control - Integrated Framework: Executive SummaryDocument20 pagesInternal Control - Integrated Framework: Executive SummaryAswin Artha100% (1)

- PDF CRMA Exam Study Guide 1st EditionDocument6 pagesPDF CRMA Exam Study Guide 1st EditionwesleypmNo ratings yet

- COSO WBCSD Release New Draft Guidance Online ViewingDocument79 pagesCOSO WBCSD Release New Draft Guidance Online ViewingAntónio FerreiraNo ratings yet

- Fractional Differential Equations: Bangti JinDocument377 pagesFractional Differential Equations: Bangti JinOmar GuzmanNo ratings yet

- Coso Erm Faq September 2017Document9 pagesCoso Erm Faq September 2017Alex Adrián Vargas MejíaNo ratings yet

- Erm Coso Framework PDFDocument2 pagesErm Coso Framework PDFMikeNo ratings yet

- Diagnostic Test Everybody Up 5, 2020Document2 pagesDiagnostic Test Everybody Up 5, 2020George Paz0% (1)

- COSODocument8 pagesCOSOParthasarathi JhaNo ratings yet

- Factsheet Operational AuditingDocument2 pagesFactsheet Operational AuditingMaria Jeannie CurayNo ratings yet

- Ingres in ReproductionDocument20 pagesIngres in ReproductionKarlNo ratings yet

- Lesson 3 - Adaptation AssignmentDocument3 pagesLesson 3 - Adaptation AssignmentEmmy RoseNo ratings yet

- Thesis Statement On Corporate Social ResponsibilityDocument5 pagesThesis Statement On Corporate Social Responsibilitypjrozhiig100% (2)

- Đề Anh DHBB K10 (15-16) CBNDocument17 pagesĐề Anh DHBB K10 (15-16) CBNThân Hoàng Minh0% (1)

- Vicente BSC2-4 WhoamiDocument3 pagesVicente BSC2-4 WhoamiVethinaVirayNo ratings yet

- Electromyostimulation StudyDocument22 pagesElectromyostimulation StudyAgnes Sophia PenuliarNo ratings yet

- As I Lay Writing How To Write Law Review ArticleDocument23 pagesAs I Lay Writing How To Write Law Review ArticleWalter Perez NiñoNo ratings yet

- DSS 2 (7th&8th) May2018Document2 pagesDSS 2 (7th&8th) May2018Piara SinghNo ratings yet

- 1.12 Properties of The Ism - FlexibilityDocument4 pages1.12 Properties of The Ism - FlexibilityyomnahelmyNo ratings yet

- SST Vs BBTDocument7 pagesSST Vs BBTFlaxkikare100% (1)

- Pharmacy System Project PlanDocument8 pagesPharmacy System Project PlankkumarNo ratings yet

- A List of 142 Adjectives To Learn For Success in The TOEFLDocument4 pagesA List of 142 Adjectives To Learn For Success in The TOEFLchintyaNo ratings yet

- GSM Based Prepaid Electricity System With Theft Detection Using Arduino For The Domestic UserDocument13 pagesGSM Based Prepaid Electricity System With Theft Detection Using Arduino For The Domestic UserSanatana RoutNo ratings yet

- Alan Freeman - Ernest - Mandels - Contribution - To - Economic PDFDocument34 pagesAlan Freeman - Ernest - Mandels - Contribution - To - Economic PDFhajimenozakiNo ratings yet

- F. Moyra Allen: A Life in Nursing, 1921-1996: Meryn Stuart, R.N., PH.DDocument9 pagesF. Moyra Allen: A Life in Nursing, 1921-1996: Meryn Stuart, R.N., PH.DRose Nirwana HandayaniNo ratings yet

- A Meta Analysis of The Relative Contribution of Leadership Styles To Followers Mental HealthDocument18 pagesA Meta Analysis of The Relative Contribution of Leadership Styles To Followers Mental HealthOnii ChanNo ratings yet

- Higher Vapor Pressure Lower Vapor PressureDocument10 pagesHigher Vapor Pressure Lower Vapor PressureCatalina PerryNo ratings yet

- EffectivenessDocument13 pagesEffectivenessPhillip MendozaNo ratings yet

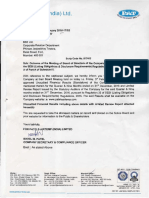

- Standalone Financial Results, Limited Review Report For December 31, 2016 (Result)Document4 pagesStandalone Financial Results, Limited Review Report For December 31, 2016 (Result)Shyam SunderNo ratings yet

- Refrigerador de Vacunas Vesfrost MKF 074Document5 pagesRefrigerador de Vacunas Vesfrost MKF 074Brevas CuchoNo ratings yet

- Service Manual: NISSAN Automobile Genuine AM/FM Radio 6-Disc CD Changer/ Cassette DeckDocument26 pagesService Manual: NISSAN Automobile Genuine AM/FM Radio 6-Disc CD Changer/ Cassette DeckEduardo Reis100% (1)

- INDUSTRIAL PHD POSITION - Sensor Fusion Enabled Indoor PositioningDocument8 pagesINDUSTRIAL PHD POSITION - Sensor Fusion Enabled Indoor Positioningzeeshan ahmedNo ratings yet

- Communication MethodDocument30 pagesCommunication MethodMisganaw GishenNo ratings yet