You might also like

- Capital Asset Pricing Theory and Arbitrage Pricing TheoryDocument19 pagesCapital Asset Pricing Theory and Arbitrage Pricing TheoryMohammed ShafiNo ratings yet

- Описание плагинов ChatGPT (eng)Document237 pagesОписание плагинов ChatGPT (eng)GriNo ratings yet

- Botswana - Guideline 2 - Pavement Testing, Analysis and Interpretation of Test Data (2000) PDFDocument99 pagesBotswana - Guideline 2 - Pavement Testing, Analysis and Interpretation of Test Data (2000) PDFDimitra KampouriNo ratings yet

- ARIMA Modeling & Forecast in ExcelDocument2 pagesARIMA Modeling & Forecast in ExcelNumXL ProNo ratings yet

- Chapter 02 Investment AppraisalDocument3 pagesChapter 02 Investment AppraisalMarzuka Akter KhanNo ratings yet

- Risk N Return BasicsDocument47 pagesRisk N Return BasicsRosli OthmanNo ratings yet

- Capital Structure: Theory and PolicyDocument31 pagesCapital Structure: Theory and PolicySuraj ShelarNo ratings yet

- SSRN Id3550293 PDFDocument143 pagesSSRN Id3550293 PDFKojiro Fuuma100% (1)

- Fertiliser Sector Report - PINC ResearchDocument72 pagesFertiliser Sector Report - PINC Researchsatish_xpNo ratings yet

- Kernel Density Estimation (KDE) in Excel TutorialDocument8 pagesKernel Density Estimation (KDE) in Excel TutorialNumXL ProNo ratings yet

- 2.4 Earnings Per ShareDocument40 pages2.4 Earnings Per ShareMinal Bihani100% (1)

- How Ab-Initio Job Is Run What Happens When You Push The "Run" Button?Document39 pagesHow Ab-Initio Job Is Run What Happens When You Push The "Run" Button?praveen kumar100% (2)

- GICS MapbookDocument52 pagesGICS MapbookVivek AryaNo ratings yet

- Higher Education Policy Analysis Using Quantitative TechniquesDocument249 pagesHigher Education Policy Analysis Using Quantitative TechniquesMonicaNo ratings yet

- Wacc MisconceptionsDocument27 pagesWacc MisconceptionsstariccoNo ratings yet

- Actuarial Mathematics and Life Table StatisticsDocument187 pagesActuarial Mathematics and Life Table StatisticsJose Carlos Rocha DiasNo ratings yet

- Foundational Theories and Techniques for Risk Management, A Guide for Professional Risk Managers in Financial Services - Part II - Financial InstrumentsFrom EverandFoundational Theories and Techniques for Risk Management, A Guide for Professional Risk Managers in Financial Services - Part II - Financial InstrumentsNo ratings yet

- Camel Rating FrameworkDocument3 pagesCamel Rating FrameworkAmrita GhartiNo ratings yet

- 2 Risk&ReturnDocument23 pages2 Risk&ReturnFebson Lee MathewNo ratings yet

- Cost Volume ProfitDocument4 pagesCost Volume ProfitProf_RamanaNo ratings yet

- Investment Analysis and Portfolio Management Christmas Worksheet 2009Document2 pagesInvestment Analysis and Portfolio Management Christmas Worksheet 2009farrukhazeemNo ratings yet

- Cost of CapitalDocument4 pagesCost of Capitalshan50% (2)

- Ifrs CasesDocument23 pagesIfrs CasesDan SimpsonNo ratings yet

- Telecom Egypt Credit RatingDocument10 pagesTelecom Egypt Credit RatingHesham TabarNo ratings yet

- I 04.05studentDocument20 pagesI 04.05studentKhánh Huyền0% (2)

- Tutorial 3 Cost of CapitalDocument1 pageTutorial 3 Cost of Capitaltai kianhongNo ratings yet

- Financial Statement Analysis ControlDocument7 pagesFinancial Statement Analysis ControlTareq MahmoodNo ratings yet

- Corporate Finance PDFDocument185 pagesCorporate Finance PDFrodgington duneNo ratings yet

- Chapter 9Document33 pagesChapter 9Annalyn Molina0% (1)

- Ch01 SMDocument33 pagesCh01 SMcalz_ccccssssdddd_550% (1)

- Nokia Analysis Report: András Csizmár, Quyen Vu, Stefanie WethDocument32 pagesNokia Analysis Report: András Csizmár, Quyen Vu, Stefanie Wethjason7sean-30030No ratings yet

- NBS Non Performing LoansDocument28 pagesNBS Non Performing LoansGreg ZuccariniNo ratings yet

- Internship Report On: Financial Analysis of KDS Accessories LimitedDocument50 pagesInternship Report On: Financial Analysis of KDS Accessories Limitedshohagh kumar ghoshNo ratings yet

- Balance Sheet Statement of Financial PositionDocument17 pagesBalance Sheet Statement of Financial PositionAhmed FawzyNo ratings yet

- Fauji Fertilizer Company (FFC) : Target Price StanceDocument17 pagesFauji Fertilizer Company (FFC) : Target Price StanceAli CheenahNo ratings yet

- 5.1 Questions: Chapter 5 Relevant Information For Decision Making With A Focus On Pricing DecisionsDocument37 pages5.1 Questions: Chapter 5 Relevant Information For Decision Making With A Focus On Pricing DecisionsLiyana ChuaNo ratings yet

- The Application of Ifrs Oil and Gas PDFDocument18 pagesThe Application of Ifrs Oil and Gas PDFSahilJainNo ratings yet

- Assignment 5 - CH 10 - The Cost of Capital PDFDocument6 pagesAssignment 5 - CH 10 - The Cost of Capital PDFAhmedFawzy0% (1)

- Chapter 10 Questions V2Document7 pagesChapter 10 Questions V2Lavanya KosuriNo ratings yet

- Case AlibrisDocument25 pagesCase AlibrisSyed Ashraful TusharNo ratings yet

- Discounted Cash Flow (DCF) Definition - InvestopediaDocument2 pagesDiscounted Cash Flow (DCF) Definition - Investopedianaviprasadthebond9532No ratings yet

- Ba1727 Security Analysis and Portfolio ManagementDocument2 pagesBa1727 Security Analysis and Portfolio Managementbhuvanesh87No ratings yet

- Fitch RatingsDocument7 pagesFitch RatingsTareqNo ratings yet

- Capital BudgetingDocument3 pagesCapital BudgetingMikz PolzzNo ratings yet

- Test Bank For New Zealand Financial Accounting 6th Edition by CraigDocument67 pagesTest Bank For New Zealand Financial Accounting 6th Edition by CraigCarolparker100% (1)

- UQAM CFA ResearchChallenge2014Document22 pagesUQAM CFA ResearchChallenge2014tomz678No ratings yet

- AppendixA SpoilageDocument19 pagesAppendixA SpoilageMohamad Nur HadiNo ratings yet

- The Cost of Capital: Prof. Dr. MD Mohan UddinDocument57 pagesThe Cost of Capital: Prof. Dr. MD Mohan UddinMd. Mehedi HasanNo ratings yet

- Cost Volume Profit Analysis For Paper 10Document6 pagesCost Volume Profit Analysis For Paper 10Zaira Anees100% (1)

- Material Requirement Planning (MRP)Document21 pagesMaterial Requirement Planning (MRP)Ramesh GarikapatiNo ratings yet

- Simple Linear Regression and Correlation: Model and Examine The Relationship Between A and One or More (Predictors)Document31 pagesSimple Linear Regression and Correlation: Model and Examine The Relationship Between A and One or More (Predictors)محمد بركاتNo ratings yet

- Corporate Finance and Investment AnalysisDocument80 pagesCorporate Finance and Investment AnalysisCristina PopNo ratings yet

- SMCH 12Document101 pagesSMCH 12FratFool33% (3)

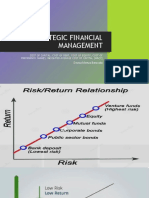

- Strategic Financial ManagementDocument28 pagesStrategic Financial ManagementDayana MasturaNo ratings yet

- Forward Rate AgreementDocument8 pagesForward Rate AgreementNaveen BhatiaNo ratings yet

- BD3 SM17Document3 pagesBD3 SM17Nguyễn Bành100% (1)

- Model Management Guidance PDFDocument70 pagesModel Management Guidance PDFChen CharlesNo ratings yet

- Solutions BD3 SM24 GEDocument4 pagesSolutions BD3 SM24 GEAgnes ChewNo ratings yet

- Cost of Capital ProblemsDocument5 pagesCost of Capital ProblemsYusairah Benito DomatoNo ratings yet

- Topic 7 - Financial Leverage - ExtraDocument57 pagesTopic 7 - Financial Leverage - ExtraBaby KhorNo ratings yet

- Take Home QuizDocument8 pagesTake Home QuizJean CabigaoNo ratings yet

- Weighted Average Cost of Capital: Banikanta MishraDocument21 pagesWeighted Average Cost of Capital: Banikanta MishraManu ThomasNo ratings yet

- III.B.6 Credit Risk Capital CalculationDocument28 pagesIII.B.6 Credit Risk Capital CalculationvladimirpopovicNo ratings yet

- Hillier Model 3Document19 pagesHillier Model 3kavyaambekarNo ratings yet

- Corporate Financial Analysis with Microsoft ExcelFrom EverandCorporate Financial Analysis with Microsoft ExcelRating: 5 out of 5 stars5/5 (1)

- X13ARIMA-SEATS Modeling Part 2 - ForecastingDocument7 pagesX13ARIMA-SEATS Modeling Part 2 - ForecastingNumXL ProNo ratings yet

- KDE Optimization - Unbiased Cross-ValidationDocument4 pagesKDE Optimization - Unbiased Cross-ValidationNumXL ProNo ratings yet

- Migration From X12ARIMA To X13ARIMA-SEATSDocument8 pagesMigration From X12ARIMA To X13ARIMA-SEATSNumXL ProNo ratings yet

- KDE Optimization PrimerDocument8 pagesKDE Optimization PrimerNumXL ProNo ratings yet

- X13ARIMA-SEATS Modeling Part 3 - RegressionDocument8 pagesX13ARIMA-SEATS Modeling Part 3 - RegressionNumXL ProNo ratings yet

- KDE - Direct Plug-In MethodDocument5 pagesKDE - Direct Plug-In MethodNumXL ProNo ratings yet

- Technical Note - Autoregressive ModelDocument12 pagesTechnical Note - Autoregressive ModelNumXL ProNo ratings yet

- SARIMAX Modeling & Forecast in ExcelDocument3 pagesSARIMAX Modeling & Forecast in ExcelNumXL ProNo ratings yet

- X13ARIMA-SEATS Modeling Part 1 - Seasonal AdjustmentDocument6 pagesX13ARIMA-SEATS Modeling Part 1 - Seasonal AdjustmentNumXL ProNo ratings yet

- SARIMA Modeling & Forecast in ExcelDocument2 pagesSARIMA Modeling & Forecast in ExcelNumXL ProNo ratings yet

- Technical Note - MLR Forecast ErrorDocument3 pagesTechnical Note - MLR Forecast ErrorNumXL ProNo ratings yet

- Time Series Simulation Tutorial in ExcelDocument5 pagesTime Series Simulation Tutorial in ExcelNumXL ProNo ratings yet

- Data Preparation For Strategy ReturnsDocument6 pagesData Preparation For Strategy ReturnsNumXL ProNo ratings yet

- EWMA TutorialDocument6 pagesEWMA TutorialNumXL ProNo ratings yet

- Technical Note - Moving Average ModelDocument9 pagesTechnical Note - Moving Average ModelNumXL ProNo ratings yet

- WTI Futures Curve Analysis Using PCA (Part I)Document7 pagesWTI Futures Curve Analysis Using PCA (Part I)NumXL ProNo ratings yet

- X12 ARIMA in NumXL NotesDocument14 pagesX12 ARIMA in NumXL NotesNumXL ProNo ratings yet

- Cointegration TestingDocument8 pagesCointegration TestingNumXL ProNo ratings yet

- Discrete Fourier Transform in Excel TutorialDocument10 pagesDiscrete Fourier Transform in Excel TutorialNumXL ProNo ratings yet

- Empirical Distribution Function (EDF) in Excel TutorialDocument6 pagesEmpirical Distribution Function (EDF) in Excel TutorialNumXL ProNo ratings yet

- Data Preparation For Futures ReturnsDocument6 pagesData Preparation For Futures ReturnsNumXL ProNo ratings yet

- NumXL VBA SDK - Getting StartedDocument7 pagesNumXL VBA SDK - Getting StartedNumXL ProNo ratings yet

- Case Study: Making Sense of Diesel PricesDocument11 pagesCase Study: Making Sense of Diesel PricesNumXL ProNo ratings yet

- Principal Component Analysis in Excel Tutorial 102Document9 pagesPrincipal Component Analysis in Excel Tutorial 102NumXL ProNo ratings yet

- Principal Component Analysis Tutorial 101 With NumXLDocument10 pagesPrincipal Component Analysis Tutorial 101 With NumXLNumXL ProNo ratings yet

- Regression Tutorial 201 With NumXLDocument12 pagesRegression Tutorial 201 With NumXLNumXL ProNo ratings yet

- Regression Tutorial 202 With NumXLDocument4 pagesRegression Tutorial 202 With NumXLNumXL ProNo ratings yet

- Assignment 2 - Update 1Document3 pagesAssignment 2 - Update 1Putri Ayuningtyas KusumawatiNo ratings yet

- Post Graduate Diploma in Data Science and Statistics (PGDDSS)Document3 pagesPost Graduate Diploma in Data Science and Statistics (PGDDSS)Monte CarloNo ratings yet

- BoxPlot LeveneDocument21 pagesBoxPlot LeveneMarco Antonio Zavaleta SanchezNo ratings yet

- Thesis 2012 AlFahad PDFDocument531 pagesThesis 2012 AlFahad PDFiliyas j sNo ratings yet

- Decsci Reviewer CHAPTER 1: Statistics and DataDocument7 pagesDecsci Reviewer CHAPTER 1: Statistics and DataGabriel Ian ZamoraNo ratings yet

- Organization Theory and Design Canadian 2nd Edition Daft Test BankDocument24 pagesOrganization Theory and Design Canadian 2nd Edition Daft Test Banksyrupselvedgezg8100% (20)

- Lógicas Inducción Deducción AbducciónDocument28 pagesLógicas Inducción Deducción Abducciónariadnatl77No ratings yet

- Lab 3 - Linear RegressionDocument15 pagesLab 3 - Linear RegressionNikhilesh PrabhakarNo ratings yet

- Maths Project On StatisticsDocument7 pagesMaths Project On Statisticschandrasekhar hazraNo ratings yet

- Module 1Document10 pagesModule 1Tess LegaspiNo ratings yet

- Path AnalysisDocument13 pagesPath AnalysisRangga B. DesaptaNo ratings yet

- ch1 Slides PDFDocument41 pagesch1 Slides PDFpepepompin89No ratings yet

- Ukkd JournalDocument10 pagesUkkd Journalyad shmNo ratings yet

- Business Econometrics Lecture Notes Quiz Econ2271Document2 pagesBusiness Econometrics Lecture Notes Quiz Econ2271gedtmaxNo ratings yet

- Week 3 Multiple Regression ModelDocument9 pagesWeek 3 Multiple Regression ModelCico CocoNo ratings yet

- CAPSULEDocument8 pagesCAPSULEJanine MalinaoNo ratings yet

- Albizia - Research PlanDocument9 pagesAlbizia - Research PlanSean Ezekiel SalvadorNo ratings yet

- M11n - Lesson 3.2 - PPT - Handout - Measures of Variability - 1sem22-23Document8 pagesM11n - Lesson 3.2 - PPT - Handout - Measures of Variability - 1sem22-23Travelers FamilyNo ratings yet

- Am (121-130) Analisis MultinivelDocument10 pagesAm (121-130) Analisis Multinivelmaximal25No ratings yet

- Error Analysis in Measurement PDFDocument2 pagesError Analysis in Measurement PDFJohnNo ratings yet

- BYK MacDocument5 pagesBYK MacNatdanai LimprasertNo ratings yet

- Using Hermeneutic Phenomenology To Investigate How Experienced PRDocument29 pagesUsing Hermeneutic Phenomenology To Investigate How Experienced PRStan AnisNo ratings yet

- BARC BI Trend Monitor 2019 PDFDocument70 pagesBARC BI Trend Monitor 2019 PDFElvis Arnez SaraviaNo ratings yet

- Homework 3Document10 pagesHomework 3canqarazadeanarNo ratings yet

- Ba Unit 4 - Part1Document7 pagesBa Unit 4 - Part1Arunim YadavNo ratings yet

- 14 - Chapter 7 PDFDocument39 pages14 - Chapter 7 PDFMay Anne M. ArceoNo ratings yet