You might also like

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- Relative Value Methodologies For Global Credit Bond Portfolio ManagementDocument13 pagesRelative Value Methodologies For Global Credit Bond Portfolio ManagementeucludeNo ratings yet

- Analysis of Corporate Valuation Theories and A Valuation of ISSDocument112 pagesAnalysis of Corporate Valuation Theories and A Valuation of ISSJacob Bar100% (2)

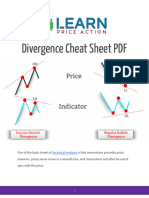

- Divergence Cheat Sheet PDFDocument17 pagesDivergence Cheat Sheet PDFlightbarq100% (1)

- Deeni TaleemDocument33 pagesDeeni TaleemauliasworldNo ratings yet

- Fateh e Alam Membership FormDocument1 pageFateh e Alam Membership Formrehan263No ratings yet

- Exchange Rate TheoriesDocument20 pagesExchange Rate TheoriesNoufal AnsariNo ratings yet

- Pakistan International Airlines - PIADocument1 pagePakistan International Airlines - PIAMuhammad Rehan TahirNo ratings yet

- Aetikaf-Kay-Fazail. Syed Shah Turab Ul Haq QadriDocument23 pagesAetikaf-Kay-Fazail. Syed Shah Turab Ul Haq QadriMuhammad Rehan TahirNo ratings yet

- Eid e Milaad. Syed Shah Turab Ul Haq QadriDocument7 pagesEid e Milaad. Syed Shah Turab Ul Haq QadriMuhammad Rehan TahirNo ratings yet

- Asset Market Approach: PakistanDocument23 pagesAsset Market Approach: PakistanMuhammad Rehan TahirNo ratings yet

- Pakistan - CurricularDocument1 pagePakistan - CurricularMuhammad Rehan TahirNo ratings yet

- Solar SystemDocument20 pagesSolar Systemapi-241170918No ratings yet

- Student Exchange Program (M REHAN TAHIR)Document4 pagesStudent Exchange Program (M REHAN TAHIR)Muhammad Rehan TahirNo ratings yet

- An - Analysis - of - Environmental - Challenges - Facing - Pakistan 2Document8 pagesAn - Analysis - of - Environmental - Challenges - Facing - Pakistan 2Muhammad Rehan TahirNo ratings yet

- Culture. PPT M REHAN TAHIRDocument13 pagesCulture. PPT M REHAN TAHIRMuhammad Rehan TahirNo ratings yet

- Youth of Uk: Rehan TahirDocument3 pagesYouth of Uk: Rehan TahirMuhammad Rehan TahirNo ratings yet

- UNIW 9th International Youth Gathering - Doc M REHAN TAHIRDocument3 pagesUNIW 9th International Youth Gathering - Doc M REHAN TAHIRMuhammad Rehan TahirNo ratings yet

- Valley of The Wolves Palestine CampaignDocument5 pagesValley of The Wolves Palestine CampaignMuhammad Rehan TahirNo ratings yet

- IUCN - Application - Form - en - Doc M REHAN PAKISTAN HTTP://WWW - facebook.com/MuhammadRehanTahirSocialYouthActivistDocument12 pagesIUCN - Application - Form - en - Doc M REHAN PAKISTAN HTTP://WWW - facebook.com/MuhammadRehanTahirSocialYouthActivistMuhammad Rehan TahirNo ratings yet

- Anjuman Talba e Islam (Shuhada e Anjuman Form)Document2 pagesAnjuman Talba e Islam (Shuhada e Anjuman Form)Muhammad Rehan TahirNo ratings yet

- WAY - Information FormDocument2 pagesWAY - Information FormMuhammad Rehan TahirNo ratings yet

- 7th IygDocument15 pages7th IygMuhammad Rehan TahirNo ratings yet

- Church Militant of Islam. Rehan PakistanDocument2 pagesChurch Militant of Islam. Rehan PakistanMuhammad Rehan TahirNo ratings yet

- Turkey - Pakistan (REHAN TAHIR)Document1 pageTurkey - Pakistan (REHAN TAHIR)Muhammad Rehan TahirNo ratings yet

- Muhammad Rehan Tahir's EventDocument1 pageMuhammad Rehan Tahir's EventMuhammad Rehan TahirNo ratings yet

- Rehan's WorkDocument1 pageRehan's WorkMuhammad Rehan TahirNo ratings yet

- Valley of The Wolves Palestine CampaignDocument4 pagesValley of The Wolves Palestine CampaignMuhammad Rehan TahirNo ratings yet

- An Analysis of Environmental Challenges Facing PakistanDocument7 pagesAn Analysis of Environmental Challenges Facing PakistanMuhammad Rehan TahirNo ratings yet

- List of Universities of Istanbul (Research) M Rehan Tahir / MS EPM, MSC PhysicsDocument3 pagesList of Universities of Istanbul (Research) M Rehan Tahir / MS EPM, MSC PhysicsMuhammad Rehan TahirNo ratings yet

- Cultural Economy and Globalization HSEDocument2 pagesCultural Economy and Globalization HSEMuhammad Rehan TahirNo ratings yet

- ErgonomicsDocument2 pagesErgonomicsMuhammad Rehan TahirNo ratings yet

- Enlightenment - Muhammad Rehan TahirDocument7 pagesEnlightenment - Muhammad Rehan TahirMuhammad Rehan TahirNo ratings yet

- Cost of Capital Lecture NotesDocument52 pagesCost of Capital Lecture NotesPRECIOUSNo ratings yet

- Financial Planning PresentationDocument27 pagesFinancial Planning PresentationSeidu AbdullahiNo ratings yet

- 2020 Registered Insurance Intermediaries As at 19th October 2020-MergedDocument202 pages2020 Registered Insurance Intermediaries As at 19th October 2020-MergedericmNo ratings yet

- SFMSOLUTIONS Master Minds PDFDocument10 pagesSFMSOLUTIONS Master Minds PDFHari KrishnaNo ratings yet

- Cash Flow Statement Important QuestionsDocument20 pagesCash Flow Statement Important QuestionsSatinder SinghNo ratings yet

- KPG Research Report On Nova Minerals LimitedDocument24 pagesKPG Research Report On Nova Minerals LimitedEli BernsteinNo ratings yet

- Secretarial Practices: Important QuestionsDocument3 pagesSecretarial Practices: Important QuestionsdisushahNo ratings yet

- Volatility Clustering, Leverage Effects and Risk-Return Trade-Off in The Nigerian Stock MarketDocument14 pagesVolatility Clustering, Leverage Effects and Risk-Return Trade-Off in The Nigerian Stock MarketrehanbtariqNo ratings yet

- ALGOGENE - A Trend Following Strategy Based On Volatility ApproachDocument7 pagesALGOGENE - A Trend Following Strategy Based On Volatility Approachde deNo ratings yet

- Jordan RiverDocument5 pagesJordan RiverLouise Anne MelanoNo ratings yet

- Updated Operational Circular For Issue and Listing of Commercial Paper - April 13 2022Document120 pagesUpdated Operational Circular For Issue and Listing of Commercial Paper - April 13 2022Vani PattnaikNo ratings yet

- UAW 2015 LM2 BDocument288 pagesUAW 2015 LM2 Bthe kingfishNo ratings yet

- Private Capital Investing: Private Equity - Private DebtDocument20 pagesPrivate Capital Investing: Private Equity - Private Debtw_fibNo ratings yet

- 1 - Intro To FinanceDocument23 pages1 - Intro To FinanceYudna YuNo ratings yet

- Suggested Answer CAP III June 2018 PDFDocument155 pagesSuggested Answer CAP III June 2018 PDFRajani Shrestha0% (1)

- Taxonomia NIIF IlustradaDocument187 pagesTaxonomia NIIF IlustradaJesús David Izquierdo DíazNo ratings yet

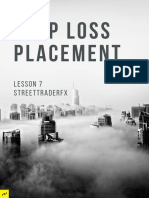

- Lesson 7 Stop Loss PlacementDocument7 pagesLesson 7 Stop Loss PlacementrosalinNo ratings yet

- Set B Multiple Choice, Chapter 24 - Capital Investment AnalysisDocument2 pagesSet B Multiple Choice, Chapter 24 - Capital Investment AnalysisJohn Carlos DoringoNo ratings yet

- Type YZ - FLO - 251123Document5 pagesType YZ - FLO - 251123Oky Arnol SunjayaNo ratings yet

- Abn 84 121 700 105Document132 pagesAbn 84 121 700 105api-25923204No ratings yet

- Demystifying Private Climate FinanceDocument62 pagesDemystifying Private Climate FinanceSaurav SumanNo ratings yet

- Chapter 3 Exponential Functions ReviewDocument10 pagesChapter 3 Exponential Functions Reviewstealthysky0129No ratings yet

- Financial Regulatory Bodies in IndiaDocument6 pagesFinancial Regulatory Bodies in IndiaRaman SrivastavaNo ratings yet

- Systematic Risk and The Equity Risk Premium: ER W ER W ERDocument12 pagesSystematic Risk and The Equity Risk Premium: ER W ER W ERLeanne TehNo ratings yet

- Staff Salary CIMB AccountDocument26 pagesStaff Salary CIMB Accountmieka8687631No ratings yet

- Screenshot 2021-11-13 at 16.04.40Document19 pagesScreenshot 2021-11-13 at 16.04.40Shahram KazemiNo ratings yet

- DAF 1307 FINANCIAL MANAGEMENT - CAT SOLUTIONS - WalterDocument6 pagesDAF 1307 FINANCIAL MANAGEMENT - CAT SOLUTIONS - WaltercyrusNo ratings yet