You might also like

- Michigan's New Driver's License Design and Security FeaturesDocument2 pagesMichigan's New Driver's License Design and Security FeaturesIgor EftimofNo ratings yet

- The Left, The Right, and The State (Read in "Fullscreen")Document570 pagesThe Left, The Right, and The State (Read in "Fullscreen")Ludwig von Mises Institute100% (68)

- Canada Post - Customs Data Collection - PrintDocument1 pageCanada Post - Customs Data Collection - PrintAnonymous EvHYcfNo ratings yet

- CA Enrollment FormDocument7 pagesCA Enrollment FormCarolineXiaNo ratings yet

- We're Reviewing Your Money Transfer.: ReceiptDocument4 pagesWe're Reviewing Your Money Transfer.: ReceiptSwiperNoSwipin0% (1)

- Instructions 1 PDFDocument2 pagesInstructions 1 PDFMhyla CunananNo ratings yet

- CRA's Intention To Revoke Letter To ISNA, Islamic Services of CanadaDocument61 pagesCRA's Intention To Revoke Letter To ISNA, Islamic Services of CanadasdbcraigNo ratings yet

- Required Docs for NC Driver's LicenseDocument3 pagesRequired Docs for NC Driver's Licensefelicia tayNo ratings yet

- Interested Party: The Standard On West Dallas: ConfirmationDocument1 pageInterested Party: The Standard On West Dallas: ConfirmationDaniel Lee Eisenberg JacobsNo ratings yet

- Your Koodo Bill: Account SummaryDocument6 pagesYour Koodo Bill: Account SummaryJuan Lorenzo García nuñezNo ratings yet

- Insurance ID Card and Important Information: Aravind Reddy Patlolla 399 Graphic BLVD New Milford, NJ 07646Document1 pageInsurance ID Card and Important Information: Aravind Reddy Patlolla 399 Graphic BLVD New Milford, NJ 07646Aravind ReddyNo ratings yet

- Between The World and MeDocument2 pagesBetween The World and Meapi-3886294240% (1)

- How K P Pinpoint Events Prasna PDFDocument129 pagesHow K P Pinpoint Events Prasna PDFRavindra ChandelNo ratings yet

- 8 Margauxs Way #8, Norfolk, MA 02056 - MLS# 71652630 - RedfinDocument7 pages8 Margauxs Way #8, Norfolk, MA 02056 - MLS# 71652630 - Redfinashes_xNo ratings yet

- Digitally signed Reliance Private Car Package Policy documentDocument11 pagesDigitally signed Reliance Private Car Package Policy documentNaseeb SinghNo ratings yet

- Member Benefits Costco Services 7 - 13 PDFDocument10 pagesMember Benefits Costco Services 7 - 13 PDFbhungi5693No ratings yet

- UTILITY BILL SUMMARYDocument2 pagesUTILITY BILL SUMMARYKaranbir SinghNo ratings yet

- Please Confirm To ContinueDocument4 pagesPlease Confirm To ContinueMahakaal Digital PointNo ratings yet

- Date Transaction Description Amount (In RS.) : Card No: 0036 1135 XXXX 3831 AAN: 0001015340002833839Document2 pagesDate Transaction Description Amount (In RS.) : Card No: 0036 1135 XXXX 3831 AAN: 0001015340002833839Satish RengarajanNo ratings yet

- American Express ProcessDocument6 pagesAmerican Express ProcessIsak VNo ratings yet

- Metocean Design and Operating ConsiderationsDocument7 pagesMetocean Design and Operating ConsiderationsNat Thana AnanNo ratings yet

- Lloyds of London Reinsurance Market GuideDocument4 pagesLloyds of London Reinsurance Market GuideVinayak NarichaniaNo ratings yet

- Ref - No. 16183558-19191991-3: Pramod Kumar S RDocument3 pagesRef - No. 16183558-19191991-3: Pramod Kumar S RS R PramodNo ratings yet

- Ngo Burca Vs RP DigestDocument1 pageNgo Burca Vs RP DigestIvy Paz100% (1)

- Kyc PDFDocument9 pagesKyc PDFOnn InternationalNo ratings yet

- Westpac Loan ApplicationDocument5 pagesWestpac Loan Applicationpatrick wafulaNo ratings yet

- Export Negotiation Collection Schedule-2015Document1 pageExport Negotiation Collection Schedule-2015kongbengNo ratings yet

- StatementsDocument5 pagesStatementsAdeelNo ratings yet

- Payment Step-By-Step: PT. Bit Coin IndonesiaDocument1 pagePayment Step-By-Step: PT. Bit Coin IndonesiaMad RajaNo ratings yet

- Payment Advices Detail ReportDocument1 pagePayment Advices Detail Reportrowena dela cruzNo ratings yet

- Bank of CyprusDocument7 pagesBank of CyprusLoizos LoizouNo ratings yet

- Bank@Campus Account - ICICI Bank LTDDocument1 pageBank@Campus Account - ICICI Bank LTDKumar RanjanNo ratings yet

- Ontario Inc.Document6 pagesOntario Inc.Metro English CanadaNo ratings yet

- BOC Account Opening FormDocument2 pagesBOC Account Opening FormCyberpoint Internet Cafe and Computer ShopNo ratings yet

- OpTransactionHistory07 10 2022Document2 pagesOpTransactionHistory07 10 2022Rg RrgNo ratings yet

- Credit Reports Scores 2Document4 pagesCredit Reports Scores 2Priya DasNo ratings yet

- KARUNANITHI SRINIVASAN1647319871895-credit-reportDocument26 pagesKARUNANITHI SRINIVASAN1647319871895-credit-reportHaritUchilNo ratings yet

- Small Business Bureau Registration Form OfficialDocument4 pagesSmall Business Bureau Registration Form OfficialNisherrie HoopsNo ratings yet

- Cimas Medical Aid Society StatementDocument2 pagesCimas Medical Aid Society Statementbertha kiaraNo ratings yet

- 2021 ArDocument142 pages2021 ArMark BöttnerNo ratings yet

- Incorporate and Grow Rich CompressDocument12 pagesIncorporate and Grow Rich CompressVictor DominguezNo ratings yet

- Deposit Bank - Google SearchDocument3 pagesDeposit Bank - Google SearchA.G. AshishNo ratings yet

- MR - Ramesh Rao DDocument2 pagesMR - Ramesh Rao DrameshraodNo ratings yet

- Digit Private Car Liability Only Policy ScheduleDocument2 pagesDigit Private Car Liability Only Policy ScheduleVishvkumar patelNo ratings yet

- Application For A Social Insurance Number Information Guide For ApplicantsDocument7 pagesApplication For A Social Insurance Number Information Guide For ApplicantsTHEBOSS09480No ratings yet

- ZYDUSLIFE 30052022203428 DLOFCoverLetterExchangesdt30052022Document81 pagesZYDUSLIFE 30052022203428 DLOFCoverLetterExchangesdt30052022Swarup JadhavNo ratings yet

- Experian Data Breach: Frequently Asked Questions For Individual ClientsDocument3 pagesExperian Data Breach: Frequently Asked Questions For Individual ClientsYusheel RamruthenNo ratings yet

- OneCard Statement Summary (20 Nov - 19 DecDocument4 pagesOneCard Statement Summary (20 Nov - 19 Decsouvik panNo ratings yet

- Bank Account Application FormDocument3 pagesBank Account Application Formeliastc76No ratings yet

- Merchant Banking in India: A GuideDocument65 pagesMerchant Banking in India: A Guideprathamesh kaduNo ratings yet

- Payment Application Form: Applicant'S ParticularsDocument2 pagesPayment Application Form: Applicant'S ParticularsVijay PuramNo ratings yet

- Money Matters FinalDocument3 pagesMoney Matters Finalapi-336224582No ratings yet

- Msi Employment Package Part1 CleanDocument11 pagesMsi Employment Package Part1 Cleanapi-474990711No ratings yet

- Borang CIMB Jan 2023Document15 pagesBorang CIMB Jan 2023anuaraqNo ratings yet

- MOTADI SAI PRASANNA statementDocument4 pagesMOTADI SAI PRASANNA statementNagarjuna SOCNo ratings yet

- Free Credit Score and Report - Free Monthly Credit CheckDocument3 pagesFree Credit Score and Report - Free Monthly Credit CheckSagar Chandra KhatuaNo ratings yet

- Mobile QR-Code For Smart Checkout System Using SETM AlgorithmDocument73 pagesMobile QR-Code For Smart Checkout System Using SETM AlgorithmVictor OkonkwoNo ratings yet

- Land and Property Taxation Systems Around the WorldDocument50 pagesLand and Property Taxation Systems Around the Worldaini nabillahNo ratings yet

- Account Opening FormDocument26 pagesAccount Opening Formshort vids sidNo ratings yet

- Novo Stanje: Novo Stanje: Minimalno Za Uplatu: Minimalno Za UplatuDocument8 pagesNovo Stanje: Novo Stanje: Minimalno Za Uplatu: Minimalno Za UplatuTemeljkovski DraganNo ratings yet

- Pay 2,000 GBP to Flywire for University FeesDocument3 pagesPay 2,000 GBP to Flywire for University FeesMuhammad Aqeel Anwar ButtNo ratings yet

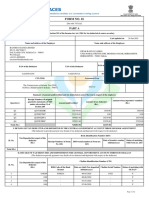

- Form No. 16: Part ADocument7 pagesForm No. 16: Part AMirza Aftab BaigNo ratings yet

- Remote Driver's Licence ApplicationDocument1 pageRemote Driver's Licence ApplicationFloyd McDermott100% (1)

- Cibil ScoreDocument2 pagesCibil ScoreAjay BaranwalNo ratings yet

- Corporate Rishi LeadershipDocument10 pagesCorporate Rishi Leadershipmeenakshi56No ratings yet

- MeenakshiDocument9 pagesMeenakshimeenakshi56No ratings yet

- A Report On "Balance of Payments": Concept QuestionsDocument28 pagesA Report On "Balance of Payments": Concept Questionsmeenakshi56No ratings yet

- Analysis Chapter5Document8 pagesAnalysis Chapter5meenakshi56No ratings yet

- Micro Finance Institutions Problems FVFFFFFFFFFFFFFFFFFFFFFFFFFFFFDocument1 pageMicro Finance Institutions Problems FVFFFFFFFFFFFFFFFFFFFFFFFFFFFFmeenakshi56No ratings yet

- Indian Depository ReceiptsDocument11 pagesIndian Depository Receiptsmeenakshi56100% (1)

- The role of corporate governance in productivity, social welfare and accountabilityDocument4 pagesThe role of corporate governance in productivity, social welfare and accountabilitymeenakshi56No ratings yet

- Slide 1Document5 pagesSlide 1meenakshi56No ratings yet

- Socialization Process IGDocument11 pagesSocialization Process IGmeenakshi56No ratings yet

- Saini Sir WordDocument10 pagesSaini Sir Wordmeenakshi56No ratings yet

- FILE008Document14 pagesFILE008meenakshi56No ratings yet

- External SeminarDocument7 pagesExternal Seminarmeenakshi56No ratings yet

- AmericaDocument8 pagesAmericameenakshi56No ratings yet

- The role of corporate governance in productivity, social welfare and accountabilityDocument4 pagesThe role of corporate governance in productivity, social welfare and accountabilitymeenakshi56No ratings yet

- Non Financial InformationDocument4 pagesNon Financial Informationmeenakshi56No ratings yet

- HimaniDocument10 pagesHimanimeenakshi56No ratings yet

- Review of LiteratureDocument7 pagesReview of Literaturemeenakshi56No ratings yet

- Micro Finance Institutions Problems FVFFFFFFFFFFFFFFFFFFFFFFFFFFFFDocument1 pageMicro Finance Institutions Problems FVFFFFFFFFFFFFFFFFFFFFFFFFFFFFmeenakshi56No ratings yet

- Thoreau's Walden Pond Experiment in Self-Reliance and SimplicityDocument10 pagesThoreau's Walden Pond Experiment in Self-Reliance and Simplicitymeenakshi56No ratings yet

- REFERENCEDocument1 pageREFERENCEmeenakshi56No ratings yet

- ENTERPDocument5 pagesENTERPmeenakshi56No ratings yet

- AdvantagesDocument6 pagesAdvantagesmeenakshi56No ratings yet

- Objective of The StudyDocument1 pageObjective of The Studymeenakshi56No ratings yet

- ConciliationDocument7 pagesConciliationmeenakshi56No ratings yet

- TVS Motors Mahindra & Mahindra Honda Motors: Bajaj AutoDocument5 pagesTVS Motors Mahindra & Mahindra Honda Motors: Bajaj Automeenakshi56No ratings yet

- Indian Banking Industry History and Current LandscapeDocument2 pagesIndian Banking Industry History and Current Landscapemeenakshi56No ratings yet

- Definition of ImportantDocument8 pagesDefinition of Importantmeenakshi56No ratings yet

- Indian Railways Online WebsiteDocument1 pageIndian Railways Online Websitemeenakshi56No ratings yet

- PNB DEPOSIT OR TERM DEPOSIT INTEREST RATES ACCORDING TO 3 AugustDocument2 pagesPNB DEPOSIT OR TERM DEPOSIT INTEREST RATES ACCORDING TO 3 Augustmeenakshi56No ratings yet

- Meaning of Internet F.RDocument3 pagesMeaning of Internet F.Rmeenakshi56No ratings yet

- Retail investment: Addressing timing and pricing issues through SIPsDocument52 pagesRetail investment: Addressing timing and pricing issues through SIPsMauryanNo ratings yet

- TARIFFS AND POLITICS - EVIDENCE FROM TRUMPS Trade War - Thiemo Fetze and Carlo Schwarz PDFDocument25 pagesTARIFFS AND POLITICS - EVIDENCE FROM TRUMPS Trade War - Thiemo Fetze and Carlo Schwarz PDFWilliam WulffNo ratings yet

- Answers and Equations for Investment Quotient Test ChaptersDocument3 pagesAnswers and Equations for Investment Quotient Test ChaptersJudeNo ratings yet

- ERP in Apparel IndustryDocument17 pagesERP in Apparel IndustrySuman KumarNo ratings yet

- Bautista CL MODULEDocument2 pagesBautista CL MODULETrisha Anne Aranzaso BautistaNo ratings yet

- Personal Values: Definitions & TypesDocument1 pagePersonal Values: Definitions & TypesGermaeGonzalesNo ratings yet

- Northern Nigeria Media History OverviewDocument7 pagesNorthern Nigeria Media History OverviewAdetutu AnnieNo ratings yet

- Annamalai University: B.A. SociologyDocument84 pagesAnnamalai University: B.A. SociologyJoseph John100% (1)

- Some People Think We Should Abolish All Examinations in School. What Is Your Opinion?Document7 pagesSome People Think We Should Abolish All Examinations in School. What Is Your Opinion?Bach Hua Hua100% (1)

- JNMF Scholarship Application Form-1Document7 pagesJNMF Scholarship Application Form-1arudhayNo ratings yet

- Ricoh MP 4001 Users Manual 121110Document6 pagesRicoh MP 4001 Users Manual 121110liliana vargas alvarezNo ratings yet

- High-Performance Work Practices: Labor UnionDocument2 pagesHigh-Performance Work Practices: Labor UnionGabriella LomanorekNo ratings yet

- Class Xi BST Chapter 6. Social Resoposibility (Competency - Based Test Items) Marks WiseDocument17 pagesClass Xi BST Chapter 6. Social Resoposibility (Competency - Based Test Items) Marks WiseNidhi ShahNo ratings yet

- Edsml Assignment SCM 2 - Velux GroupDocument20 pagesEdsml Assignment SCM 2 - Velux GroupSwapnil BhagatNo ratings yet

- GLORIADocument97 pagesGLORIAGovel EzraNo ratings yet

- F1 English PT3 Formatted Exam PaperDocument10 pagesF1 English PT3 Formatted Exam PaperCmot Qkf Sia-zNo ratings yet

- Student-Led School Hazard MappingDocument35 pagesStudent-Led School Hazard MappingjuliamarkNo ratings yet

- Fil 01 Modyul 7Document30 pagesFil 01 Modyul 7Jamie ann duquezNo ratings yet

- How Zagreb's Socialist Experiment Finally Matured Long After Socialism - Failed ArchitectureDocument12 pagesHow Zagreb's Socialist Experiment Finally Matured Long After Socialism - Failed ArchitectureAneta Mudronja PletenacNo ratings yet

- Winny Chepwogen CVDocument16 pagesWinny Chepwogen CVjeff liwaliNo ratings yet

- Chap1 HRM581 Oct Feb 2023Document20 pagesChap1 HRM581 Oct Feb 2023liana bahaNo ratings yet

- Hackers Speaking Test ReviewDocument21 pagesHackers Speaking Test ReviewMark Danniel SaludNo ratings yet

- Demonetisation IndiaDocument71 pagesDemonetisation IndiaVinay GuptaNo ratings yet

- 50 Simple Interest Problems With SolutionsDocument46 pages50 Simple Interest Problems With SolutionsArnel MedinaNo ratings yet

- A Practical Guide To The 1999 Red & Yellow Books, Clause8-Commencement, Delays & SuspensionDocument4 pagesA Practical Guide To The 1999 Red & Yellow Books, Clause8-Commencement, Delays & Suspensiontab77zNo ratings yet