You might also like

- Lemp ExperienceDocument18 pagesLemp Experiencearchanahrdept100% (3)

- Barclays - India IT Services Group Mid-Cap Conversations Suggest Steady DemandDocument26 pagesBarclays - India IT Services Group Mid-Cap Conversations Suggest Steady DemandProfitbytesNo ratings yet

- Barclays-Infosys Ltd. - The Next Three Years PDFDocument17 pagesBarclays-Infosys Ltd. - The Next Three Years PDFProfitbytesNo ratings yet

- DIsh TV 130701 Nomura Reiterate Buy Focus On Value-Focused Subscribers and FCF, Industry Dynamics Improving Buy TGT 108 Upside 77%Document16 pagesDIsh TV 130701 Nomura Reiterate Buy Focus On Value-Focused Subscribers and FCF, Industry Dynamics Improving Buy TGT 108 Upside 77%ProfitbytesNo ratings yet

- J. P Morgan - New Bank Licenses - Picking The WinnersDocument9 pagesJ. P Morgan - New Bank Licenses - Picking The WinnersProfitbytesNo ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (120)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

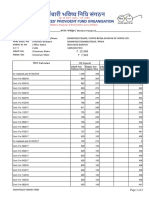

- Composite Claim Form (Non-Aadhar) : Employees' Provident Funds OrganisationDocument2 pagesComposite Claim Form (Non-Aadhar) : Employees' Provident Funds OrganisationEr Aniket HarekarNo ratings yet

- Book Understanding Act Practice PDFDocument14 pagesBook Understanding Act Practice PDFWilly BanGo0% (4)

- NHRS' Day of ReckoningDocument3 pagesNHRS' Day of ReckoningNHGOPSenateNo ratings yet

- RSA Vs RSUDocument15 pagesRSA Vs RSUEleonora Buzzetti0% (1)

- Exercise No. 4 in ECON 11deferred AnnuityDocument2 pagesExercise No. 4 in ECON 11deferred AnnuityMarlon BautistaNo ratings yet

- AP MPL Act 1965 SectionsDocument32 pagesAP MPL Act 1965 SectionsRaghu RamNo ratings yet

- Confederation For Unity, Recognition and Advancement of Government EmployeesDocument2 pagesConfederation For Unity, Recognition and Advancement of Government EmployeesBenjie SalesNo ratings yet

- Rules On Gross Income TaxationDocument15 pagesRules On Gross Income TaxationEar TanNo ratings yet

- SsDocument8 pagesSsAnonymous cPS4htyNo ratings yet

- Brief Notes of Income From SalaryDocument10 pagesBrief Notes of Income From SalaryAnupam BaliNo ratings yet

- FBP To-Be Process - April 1 India ReleaseDocument24 pagesFBP To-Be Process - April 1 India Releaseraghava_cseNo ratings yet

- Math of Investment QuizDocument1 pageMath of Investment QuizLino GumpalNo ratings yet

- Wey FinMan 4e TB AppK Other-Significant-LiabilitiesDocument11 pagesWey FinMan 4e TB AppK Other-Significant-LiabilitiesJim AxelNo ratings yet

- Income TaxDocument98 pagesIncome TaxGunjan Maheshwari50% (2)

- Itr-1 Sahaj Indian Income Tax Return: Acknowledgement Number: Assessment Year: 2019-20Document6 pagesItr-1 Sahaj Indian Income Tax Return: Acknowledgement Number: Assessment Year: 2019-20Gajanan DestotNo ratings yet

- F Business Taxation 671079211Document4 pagesF Business Taxation 671079211anand0% (1)

- CFP Mock Test Tax PlanningDocument8 pagesCFP Mock Test Tax PlanningDeep Shikha67% (3)

- Account Transfer Form (ACAT)Document6 pagesAccount Transfer Form (ACAT)MichelleNo ratings yet

- Form 6744Document6 pagesForm 6744api-495108136No ratings yet

- ESTATE and Trust TaxationDocument8 pagesESTATE and Trust TaxationVida Urduja B. Liwag-Cena50% (2)

- DSNHP00237190000175866Document2 pagesDSNHP00237190000175866Pankaj GuleriaNo ratings yet

- Quiz 5B - Exclusions From Gross IncomeDocument11 pagesQuiz 5B - Exclusions From Gross IncomeMychie Lynne MayugaNo ratings yet

- MC 0707Document10 pagesMC 0707mcchronicleNo ratings yet

- Income-Tax-Calculator 2023-24Document8 pagesIncome-Tax-Calculator 2023-24AlokNo ratings yet

- The Payment of Bonus & Gratuity Act. Bonus Act-1965 & Gratuity Act-1972Document34 pagesThe Payment of Bonus & Gratuity Act. Bonus Act-1965 & Gratuity Act-1972Dhruti AthaNo ratings yet

- MCSR (Pension)Document51 pagesMCSR (Pension)akshayryuk0% (1)

- Modern Auditing Chapter 16Document13 pagesModern Auditing Chapter 16Charis SubiantoNo ratings yet

- 1st Prelim Feu Answer Key Problem SolvingDocument6 pages1st Prelim Feu Answer Key Problem SolvinganggandakonohNo ratings yet

- Financial Life Cycle 1Document13 pagesFinancial Life Cycle 1api-381832809No ratings yet