You might also like

- 05A ImpairmentDocument22 pages05A ImpairmentEuglena VerdeNo ratings yet

- Financial Reporting and Auditing in Sovereign Operations: Technical Guidance NoteFrom EverandFinancial Reporting and Auditing in Sovereign Operations: Technical Guidance NoteNo ratings yet

- Conceptual Framework For Financial ReportingDocument8 pagesConceptual Framework For Financial ReportingQueeny Man-oyaoNo ratings yet

- Conceptual Framework Objectives of Financial ReportingDocument5 pagesConceptual Framework Objectives of Financial ReportingAllaine ElfaNo ratings yet

- International Financial Statement AnalysisFrom EverandInternational Financial Statement AnalysisRating: 1 out of 5 stars1/5 (1)

- IASB Update September 2009Document9 pagesIASB Update September 2009Gon FreecsNo ratings yet

- 19996ipcc Paper5 App1Document17 pages19996ipcc Paper5 App1anilNo ratings yet

- Financial StatementDocument22 pagesFinancial StatementHJ ManviNo ratings yet

- 66487bos53751 Accp 1Document21 pages66487bos53751 Accp 1Sabareesh KpNo ratings yet

- 02FAccReporting1 SM Ch2 2LPDocument5 pages02FAccReporting1 SM Ch2 2LPNazirul HazwanNo ratings yet

- Module 002 Overview of Conceptual Framework and Financial Reporting ObjectivesDocument11 pagesModule 002 Overview of Conceptual Framework and Financial Reporting ObjectivesCriselito EnigrihoNo ratings yet

- Financial Accounting and Reporting - Week 1 Topic 3 - Conceptual Framework Level 1Document9 pagesFinancial Accounting and Reporting - Week 1 Topic 3 - Conceptual Framework Level 1LuisitoNo ratings yet

- Tutorial 2 SolutionsDocument4 pagesTutorial 2 SolutionsnaboumilikaNo ratings yet

- Asc 944Document172 pagesAsc 944Babymetal LoNo ratings yet

- 3sm Finalnew Accpro-Part1Document18 pages3sm Finalnew Accpro-Part1B GANAPATHYNo ratings yet

- ACCO 20063 Homework 1 Assigned Activities From IM 1Document3 pagesACCO 20063 Homework 1 Assigned Activities From IM 1Vincent Luigil AlceraNo ratings yet

- Report - The Conceptual FrameworkDocument5 pagesReport - The Conceptual FrameworkmarinNo ratings yet

- Week 1 Conceptual Framework For Financial ReportingDocument17 pagesWeek 1 Conceptual Framework For Financial ReportingSHANE NAVARRONo ratings yet

- Conceptual Framework (Feb 2011)Document30 pagesConceptual Framework (Feb 2011)Deborah LyeNo ratings yet

- The Conceptual Framework for Financial ReportingDocument14 pagesThe Conceptual Framework for Financial ReportingMaryrose SumulongNo ratings yet

- Framework For The Preparation and Presentation of Financial StatementsDocument14 pagesFramework For The Preparation and Presentation of Financial StatementsHasnain MahmoodNo ratings yet

- Kothari CH 2Document38 pagesKothari CH 2alexajungNo ratings yet

- CONCEPTUAL FRAMEWORK PROGRAMME - VIII - (B)Document8 pagesCONCEPTUAL FRAMEWORK PROGRAMME - VIII - (B)najiath mzeeNo ratings yet

- 01 Acctg 321 A&B Mock Test-1Document26 pages01 Acctg 321 A&B Mock Test-1Drayce FerranNo ratings yet

- Conceptual Framework For Financial ReportingDocument54 pagesConceptual Framework For Financial ReportingAlthea Claire Yhapon100% (1)

- Financial Accounting and Reporting 03Document6 pagesFinancial Accounting and Reporting 03Nuah SilvestreNo ratings yet

- Chapter 2 - Framework For Preparation and Presentation of Financial StatementsDocument34 pagesChapter 2 - Framework For Preparation and Presentation of Financial StatementsSumit PattanaikNo ratings yet

- W2 Module 3 Conceptual Framework Andtheoretical Structure of Financial Accounting and Reporting Part 1Document6 pagesW2 Module 3 Conceptual Framework Andtheoretical Structure of Financial Accounting and Reporting Part 1Rose RaboNo ratings yet

- Stice Chap 1 Exercises SummaryDocument188 pagesStice Chap 1 Exercises SummaryMariel SalangsangNo ratings yet

- Corporate ReportingDocument29 pagesCorporate ReportingVignesh BalachandarNo ratings yet

- Applying International Financial Reporting Standards Picker 3rd Edition Test BankDocument7 pagesApplying International Financial Reporting Standards Picker 3rd Edition Test Bankscottharperydconefmit100% (47)

- Philippine School of Business Administration: Cpa ReviewDocument9 pagesPhilippine School of Business Administration: Cpa ReviewLeisleiRagoNo ratings yet

- Chapter 1 Conceptual Framework Sample QuizDocument26 pagesChapter 1 Conceptual Framework Sample QuizMargeNo ratings yet

- GaumaDocument3 pagesGaumaAngela Beatrix GaumaNo ratings yet

- Conceptual Framework Lecture NotesDocument5 pagesConceptual Framework Lecture NotesAnna Micaella Dela CruzNo ratings yet

- The Conceptual Framework for Financial ReportingDocument7 pagesThe Conceptual Framework for Financial Reportingvitria zhuanita100% (1)

- Framework FOR Preparation AND Presentation OF Financial StatementsDocument34 pagesFramework FOR Preparation AND Presentation OF Financial Statementssamartha umbareNo ratings yet

- Chapter 1.2-3 Objectives of Financial StatementsDocument2 pagesChapter 1.2-3 Objectives of Financial StatementsAmyNo ratings yet

- Ans To Exercises Stice Chap 1 and Hall Chap 1234 5 11 All ProblemsDocument188 pagesAns To Exercises Stice Chap 1 and Hall Chap 1234 5 11 All ProblemsLouise GazaNo ratings yet

- Full Download Financial Reporting and Analysis 5th Edition Revsine Solutions ManualDocument20 pagesFull Download Financial Reporting and Analysis 5th Edition Revsine Solutions Manualkarolynzwilling100% (44)

- Solution Manual For Applying International Financial Reporting Standards Picker Leo Loftus Wise Clark Alfredson 3rd EditionDocument6 pagesSolution Manual For Applying International Financial Reporting Standards Picker Leo Loftus Wise Clark Alfredson 3rd Editionbrillspillowedfv6nvm100% (27)

- IFRS Accounting Standards IdentificationDocument3 pagesIFRS Accounting Standards IdentificationMarcus MonocayNo ratings yet

- Conceptual Framework SummaryDocument2 pagesConceptual Framework SummaryPhoebe AbadNo ratings yet

- Module 4 - Corporate FinanceDocument6 pagesModule 4 - Corporate FinanceAripin SangcopanNo ratings yet

- Conceptual Framework: Objective of Financial ReportingDocument47 pagesConceptual Framework: Objective of Financial Reporting버니 모지코No ratings yet

- Assigned Activities From IM 1Document3 pagesAssigned Activities From IM 1Maria Kathreena Andrea AdevaNo ratings yet

- 11Document27 pages11James Gliponio CamanteNo ratings yet

- Chapter 16 - AnswerDocument8 pagesChapter 16 - Answerwynellamae100% (2)

- GEC Elect 2 Module 5Document15 pagesGEC Elect 2 Module 5Aira Mae Quinones OrendainNo ratings yet

- Conceptual Framework For Financial Reporting Objectives of Financial ReportingDocument31 pagesConceptual Framework For Financial Reporting Objectives of Financial ReportingteryNo ratings yet

- Introduction To Finance 1Document11 pagesIntroduction To Finance 1skrzakNo ratings yet

- Financial AnalysisDocument67 pagesFinancial Analysisdushya4100% (1)

- Overview of Accounting Standards, Ind AS and IFRS - Taxguru - inDocument13 pagesOverview of Accounting Standards, Ind AS and IFRS - Taxguru - inPurohit Raju1No ratings yet

- FM MJ20 Detailed CommentaryDocument4 pagesFM MJ20 Detailed CommentaryleylaNo ratings yet

- Corporate Finance Product and ProcessDocument19 pagesCorporate Finance Product and ProcessniharjNo ratings yet

- IASB Frawwork - NotesDocument7 pagesIASB Frawwork - NotesAbdul MuneemNo ratings yet

- Financial Management & Capital Budgeting ExplainedDocument11 pagesFinancial Management & Capital Budgeting Explainedamit2981987No ratings yet

- Mocha Coffee CakeDocument13 pagesMocha Coffee CakeEuglena VerdeNo ratings yet

- Instant Pot Oreo CheesecakeDocument24 pagesInstant Pot Oreo CheesecakeEuglena VerdeNo ratings yet

- Eyagendafiscala2015 150127002314 Conversion Gate01 PDFDocument136 pagesEyagendafiscala2015 150127002314 Conversion Gate01 PDFEuglena VerdeNo ratings yet

- EY Eurozone Outlook For FS Autumn 2013Document32 pagesEY Eurozone Outlook For FS Autumn 2013Euglena VerdeNo ratings yet

- Creamy Lemon and Raspberry SliceDocument8 pagesCreamy Lemon and Raspberry SliceEuglena VerdeNo ratings yet

- EY Diversity and Inclusiveness Review 2013Document40 pagesEY Diversity and Inclusiveness Review 2013Euglena VerdeNo ratings yet

- 11 Secrets To Ending Fights in Your Relationships PDFDocument11 pages11 Secrets To Ending Fights in Your Relationships PDFEuglena VerdeNo ratings yet

- Dark Chocolate Cranberry Bundt CakeDocument15 pagesDark Chocolate Cranberry Bundt CakeEuglena VerdeNo ratings yet

- Glazed Orange SconesDocument20 pagesGlazed Orange SconesEuglena VerdeNo ratings yet

- 222t Getting Enough Vitamin D.Document4 pages222t Getting Enough Vitamin D.Euglena VerdeNo ratings yet

- Ey Eurozone Sept 2013 Main ReportDocument60 pagesEy Eurozone Sept 2013 Main ReportEuglena VerdeNo ratings yet

- EY Automotive Changing Lanes 2014-15Document8 pagesEY Automotive Changing Lanes 2014-15Euglena VerdeNo ratings yet

- EY Global Review 2013Document88 pagesEY Global Review 2013Euglena VerdeNo ratings yet

- EY Diversity Drives DiversityDocument20 pagesEY Diversity Drives DiversityEuglena VerdeNo ratings yet

- 2013G - CM3494 - TP - UN Launches Practical Manual On TP For Developing CountriesDocument4 pages2013G - CM3494 - TP - UN Launches Practical Manual On TP For Developing CountriesEuglena VerdeNo ratings yet

- 2013G - CM4021 - Italy Increases 2013 and 2014 Corporate Income Tax Advance PaymentsDocument4 pages2013G - CM4021 - Italy Increases 2013 and 2014 Corporate Income Tax Advance PaymentsEuglena VerdeNo ratings yet

- 2Q13 Global Themes Report - Final (27 August 2013)Document22 pages2Q13 Global Themes Report - Final (27 August 2013)Euglena VerdeNo ratings yet

- 2013 Worldwide VAT GST and Sales Tax GuideDocument828 pages2013 Worldwide VAT GST and Sales Tax GuideEuglena VerdeNo ratings yet

- View From The Top Global Technology Trends and Performance October 2012 February 2013Document24 pagesView From The Top Global Technology Trends and Performance October 2012 February 2013Euglena VerdeNo ratings yet

- ,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,Document8 pages,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,,Saptarshi MitraNo ratings yet

- EY Global Oil and Gas Reserves Study 2013Document112 pagesEY Global Oil and Gas Reserves Study 2013Joao Carlos DrumondNo ratings yet

- Privacy Trends 2013 - The Uphill Climb ContinuesDocument32 pagesPrivacy Trends 2013 - The Uphill Climb ContinuesEuglena VerdeNo ratings yet

- EY Conserving Value in A Maturing Russian Market 8 August 2013Document8 pagesEY Conserving Value in A Maturing Russian Market 8 August 2013Euglena VerdeNo ratings yet

- Mhealth Report - Final - 19 Nov 12Document54 pagesMhealth Report - Final - 19 Nov 12Euglena VerdeNo ratings yet

- EY Global Mobility SurveyDocument24 pagesEY Global Mobility SurveyEuglena VerdeNo ratings yet

- Strategy and Risk Appetite-16 January 2013Document12 pagesStrategy and Risk Appetite-16 January 2013Euglena VerdeNo ratings yet

- Digital Agility Now FP0002Document36 pagesDigital Agility Now FP0002Euglena VerdeNo ratings yet

- EY Audit Committee Bulletin Issue 5 October 2013Document16 pagesEY Audit Committee Bulletin Issue 5 October 2013Euglena VerdeNo ratings yet

- Business Risks Facing Mining and Metals 2013-2014 ER0069Document64 pagesBusiness Risks Facing Mining and Metals 2013-2014 ER0069Euglena VerdeNo ratings yet

- ViewPoints 33 - Cybersecurity - 16 January 2013Document15 pagesViewPoints 33 - Cybersecurity - 16 January 2013Euglena VerdeNo ratings yet

- Stock Research Report For UNH As of 7/27/11 - Chaikin Power ToolsDocument4 pagesStock Research Report For UNH As of 7/27/11 - Chaikin Power ToolsChaikin Analytics, LLCNo ratings yet

- CekaDocument3 pagesCekaChitra DwiNo ratings yet

- 1ST Sem P.Y. Acct PaperDocument30 pages1ST Sem P.Y. Acct PaperSuraj KumarNo ratings yet

- Investment Analysis - ICICIDocument17 pagesInvestment Analysis - ICICISudeep ChinnabathiniNo ratings yet

- Theories of Venture Capital and Capital Market ImperfectionDocument32 pagesTheories of Venture Capital and Capital Market ImperfectionДр. ЦчатерйееNo ratings yet

- Findings: Mutual FundDocument4 pagesFindings: Mutual FundAbdulRahman ElhamNo ratings yet

- Awareness Among The Traders About The Settlement of Online TradingDocument13 pagesAwareness Among The Traders About The Settlement of Online TradingElson Antony PaulNo ratings yet

- (Bank of America) Hybrid ARM MBS - Valuation and Risk MeasuresDocument22 pages(Bank of America) Hybrid ARM MBS - Valuation and Risk Measures00aaNo ratings yet

- Investors' Perceptions of Equity Market Investment in ShareKhan Ltd Man!alore StudyDocument81 pagesInvestors' Perceptions of Equity Market Investment in ShareKhan Ltd Man!alore StudyWilfred Dsouza63% (8)

- Capital Budgeting: Project Life-CycleDocument31 pagesCapital Budgeting: Project Life-CycleaauaniNo ratings yet

- Impact of Corona Virus On Mutual Fund by Sadanand IbitwarDocument14 pagesImpact of Corona Virus On Mutual Fund by Sadanand Ibitwarjai shree ramNo ratings yet

- Afs - Final Project - Bajaj Auto PDFDocument19 pagesAfs - Final Project - Bajaj Auto PDFKaushik GowdaNo ratings yet

- CDSC FAQ EnglishDocument44 pagesCDSC FAQ EnglishSanjeev Bikram KarkiNo ratings yet

- Accounting for Non-Current Assets (IAS 16, IAS 38Document9 pagesAccounting for Non-Current Assets (IAS 16, IAS 38storky05600% (1)

- Tutorial For Option Pricing Using The Black Scholes ModelDocument5 pagesTutorial For Option Pricing Using The Black Scholes ModelInformation should be FREE0% (1)

- Risk and Rates of ReturnDocument23 pagesRisk and Rates of ReturnIo Aya100% (1)

- 23 P1 (1) .1y ch22 PDFDocument20 pages23 P1 (1) .1y ch22 PDFAdrian NutaNo ratings yet

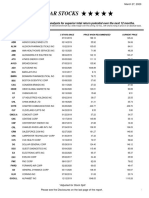

- Five Star StocksDocument5 pagesFive Star StocksJeff SturgeonNo ratings yet

- Understanding of Compulsorily Convertible Debentures Vinod KothariDocument7 pagesUnderstanding of Compulsorily Convertible Debentures Vinod KothariNazir kondkariNo ratings yet

- Long Term InvestingDocument8 pagesLong Term InvestingkrishchellaNo ratings yet

- FS 006245 Mag 06 2023Document1 pageFS 006245 Mag 06 2023grshop euNo ratings yet

- HUKUM SekuritisasiDocument17 pagesHUKUM SekuritisasiAninditaNo ratings yet

- Dr. Sharan Shetty PHD (Banking & Finance) Mba (Finance) B. Com (Hons)Document54 pagesDr. Sharan Shetty PHD (Banking & Finance) Mba (Finance) B. Com (Hons)Nagesh Pai MysoreNo ratings yet

- 2020 NoertjahyanaDocument9 pages2020 NoertjahyanaAli AzizNo ratings yet

- Bancom - Memoirs - by DR Sixto K Roxas - Ebook PDFDocument305 pagesBancom - Memoirs - by DR Sixto K Roxas - Ebook PDFVinci RoxasNo ratings yet

- The Cost of Capital, Corporation Finance and The Theory of InvestmentDocument19 pagesThe Cost of Capital, Corporation Finance and The Theory of Investmentlinda zyongweNo ratings yet

- Payback NPV Irr ArrDocument7 pagesPayback NPV Irr ArrSanthosh Chandran RNo ratings yet

- Practice For Quiz #3 Solutions For StudentsDocument10 pagesPractice For Quiz #3 Solutions For Studentssylstria.mcNo ratings yet

- Business Finance PPT - 12 Short Term Sources of FinancingDocument25 pagesBusiness Finance PPT - 12 Short Term Sources of FinancingELMSS100% (1)

- Case Study - Assessing A Firms Future Financial HealthDocument1 pageCase Study - Assessing A Firms Future Financial Healthveda20100% (2)