You might also like

- Outline Foreclosure Defense - Tila & RespaDocument13 pagesOutline Foreclosure Defense - Tila & RespaEdward BrownNo ratings yet

- Fannie Mae Term Sheet For The Citigroup - New Century Mortgage Deal 2006-09-07 Cmlti 2006-NC2Document50 pagesFannie Mae Term Sheet For The Citigroup - New Century Mortgage Deal 2006-09-07 Cmlti 2006-NC283jjmackNo ratings yet

- World Bank Insider Blows Whistle On Corruption - Federal Reserve May 2013Document8 pagesWorld Bank Insider Blows Whistle On Corruption - Federal Reserve May 2013CarrieonicNo ratings yet

- Class V III ProspectusDocument209 pagesClass V III ProspectusCarrieonicNo ratings yet

- SEC Vs Citigroup CDOs RMBS and Class V III Funding Comp-Pr2011-214Document21 pagesSEC Vs Citigroup CDOs RMBS and Class V III Funding Comp-Pr2011-214CarrieonicNo ratings yet

- Citigroup Whistle-Blower Says Bank's Brute Force' Hid Bad Loans From U.SDocument5 pagesCitigroup Whistle-Blower Says Bank's Brute Force' Hid Bad Loans From U.SCarrieonicNo ratings yet

- FCA Citi Mortgage Complaint-In-InterventionDocument36 pagesFCA Citi Mortgage Complaint-In-InterventionjodiebrittNo ratings yet

- r01c 079901Document522 pagesr01c 079901CarrieonicNo ratings yet

- In RE CitiGroup Inc Securities Litigation 1Document547 pagesIn RE CitiGroup Inc Securities Litigation 1CarrieonicNo ratings yet

- Bloomberg Markets Magazine - Citifraud July 2012Document10 pagesBloomberg Markets Magazine - Citifraud July 2012CarrieonicNo ratings yet

- Citi V SMITH WDocument4 pagesCiti V SMITH WCarrieonicNo ratings yet

- FHFA V Citigroup Inc. (09-02-11)Document95 pagesFHFA V Citigroup Inc. (09-02-11)Master ChiefNo ratings yet

- Citi Portfolio CorpDocument2 pagesCiti Portfolio CorpCarrieonicNo ratings yet

- Subsidiarys of Citigroup Inc. 2009 Exhibit21-01Document5 pagesSubsidiarys of Citigroup Inc. 2009 Exhibit21-01CarrieonicNo ratings yet

- Citi Subsidiarys 2010 Exhibit 21-01Document4 pagesCiti Subsidiarys 2010 Exhibit 21-01CarrieonicNo ratings yet

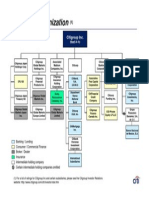

- Corp Struct CitigroupDocument1 pageCorp Struct CitigroupCarrieonicNo ratings yet

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Islamic Economics and FinanceDocument20 pagesIslamic Economics and FinancearyonsNo ratings yet

- Effect of Credit Risk Management On The Performance of Commercial Banks in Nigeria 1 To 3Document57 pagesEffect of Credit Risk Management On The Performance of Commercial Banks in Nigeria 1 To 3MajestyNo ratings yet

- VVIMP Corporate Law Summary CA Final Corporate Allied Laws Specially For Nov 12 Attempt (1) Neeraj MudgalDocument37 pagesVVIMP Corporate Law Summary CA Final Corporate Allied Laws Specially For Nov 12 Attempt (1) Neeraj MudgalLisa SanchezNo ratings yet

- Financial MatrixDocument6 pagesFinancial MatrixAsNo ratings yet

- Primer On Securitization 2019Document36 pagesPrimer On Securitization 2019Anonymous tgYyno0w6No ratings yet

- 7Document24 pages7JDNo ratings yet

- Qaz 11Document9 pagesQaz 11Shreeamar SinghNo ratings yet

- Background On Mortgages: Mortgage MarketsDocument7 pagesBackground On Mortgages: Mortgage MarketsPaw VerdilloNo ratings yet

- Chapter1 Slides FIN 4354Document14 pagesChapter1 Slides FIN 4354Shakkhor ChowdhuryNo ratings yet

- NCFM Nse Wealth Management Module BasicsDocument49 pagesNCFM Nse Wealth Management Module BasicssunnyNo ratings yet

- Form of Engagement Letter (Annotated) PDFDocument16 pagesForm of Engagement Letter (Annotated) PDFJay GiardinaNo ratings yet

- NHMFCDocument20 pagesNHMFCJohn Emanuel Alcantara100% (1)

- Financial Model: Prepared By: The Marquee GroupDocument16 pagesFinancial Model: Prepared By: The Marquee GroupSZA100% (1)

- 6-Two Faces of DebtDocument29 pages6-Two Faces of DebtscottyupNo ratings yet

- Financial Year: 2020-21 Assessment Year: 2021-22: TDS RATE CHART FY: 2020-21 (AY: 2021-22)Document2 pagesFinancial Year: 2020-21 Assessment Year: 2021-22: TDS RATE CHART FY: 2020-21 (AY: 2021-22)Mahesh Shinde100% (1)

- Aud Prob Part 1Document106 pagesAud Prob Part 1Ma. Hazel Donita DiazNo ratings yet

- Financial Ring & ComputationDocument647 pagesFinancial Ring & ComputationjorgesabatNo ratings yet

- Commercial Mortgage Loan ProcessDocument8 pagesCommercial Mortgage Loan Processlyocco1100% (1)

- Non-Legal Measures For Loan RecoveryDocument5 pagesNon-Legal Measures For Loan RecoveryJannat Taqwa100% (2)

- Ibanez DecisionDocument414 pagesIbanez Decisionmike_engle100% (1)

- CS Annual Report 2020Document225 pagesCS Annual Report 2020Anonymous kgSMlxNo ratings yet

- Think Like A Banker - Three Commercial mREIT Buys - Seeking AlphaDocument19 pagesThink Like A Banker - Three Commercial mREIT Buys - Seeking AlphaProsperidade ExponencialNo ratings yet

- Shariah Issue in Ijarah ContractDocument20 pagesShariah Issue in Ijarah ContractSapna MananNo ratings yet

- 01 Task Performance 12Document3 pages01 Task Performance 12Adrasteia ZachryNo ratings yet

- En 20120404Document24 pagesEn 20120404Hai Hoang ThanhNo ratings yet

- 114 Marshall Wells vs. ElserDocument5 pages114 Marshall Wells vs. Elserenan_intonNo ratings yet

- Sino Forest Corp FinancialsDocument94 pagesSino Forest Corp FinancialsCalibrated Confidence BlogNo ratings yet

- Human Resource Management Practices of Bangladesh: IDLC Finance LimitedDocument20 pagesHuman Resource Management Practices of Bangladesh: IDLC Finance LimitedMahabub AlamNo ratings yet

- Fitch REIT TrupsDocument6 pagesFitch REIT TrupsekuzminaNo ratings yet

- Fundamental Analysis of Banking SectorsDocument56 pagesFundamental Analysis of Banking Sectorssidhant kumarNo ratings yet