You might also like

- Approved: How to Get Your Business Loan Funded Faster, Cheaper, & with Less StressFrom EverandApproved: How to Get Your Business Loan Funded Faster, Cheaper, & with Less StressRating: 5 out of 5 stars5/5 (1)

- Non Performing Assets: Shrawanthi Amruthwar-3 Arun Aggarwal-13 Aniket Kurup-22 Shruti Pai-35Document17 pagesNon Performing Assets: Shrawanthi Amruthwar-3 Arun Aggarwal-13 Aniket Kurup-22 Shruti Pai-35Arun HariharanNo ratings yet

- Prudential NormsDocument42 pagesPrudential NormsraajendrachNo ratings yet

- PPT On NpaDocument20 pagesPPT On NpaNoor Preet KaurNo ratings yet

- Non Performing AssetsDocument8 pagesNon Performing AssetsManoj YadavNo ratings yet

- Institute of Managment Studies, Davv, Indore Finance and Administration - Semester Iv Credit Management and Retail BankingDocument3 pagesInstitute of Managment Studies, Davv, Indore Finance and Administration - Semester Iv Credit Management and Retail BankingSNo ratings yet

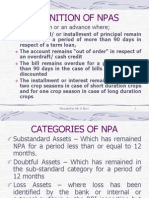

- Definition of Npas: A NPA Is A Loan or An Advance WhereDocument58 pagesDefinition of Npas: A NPA Is A Loan or An Advance WhereAnnu BallanNo ratings yet

- Non Performing Assets (Npa)Document16 pagesNon Performing Assets (Npa)Avin P RNo ratings yet

- A Study On Non Performing Assets of Sbi and Canara BankDocument75 pagesA Study On Non Performing Assets of Sbi and Canara BankeshuNo ratings yet

- Prudential NormsDocument7 pagesPrudential NormsArani KarthikNo ratings yet

- Irac NormsDocument9 pagesIrac NormsAtul ThakurNo ratings yet

- BF III - Prudential NormsDocument33 pagesBF III - Prudential NormsMd Ajmal malikNo ratings yet

- India and Non-Performing Assets: BanksDocument83 pagesIndia and Non-Performing Assets: BanksprashantgoswamiNo ratings yet

- Understanding NPA, SMA and NPA ProvisioningDocument8 pagesUnderstanding NPA, SMA and NPA ProvisioningabhinavNo ratings yet

- Debt RestructuringDocument5 pagesDebt RestructuringVinay TripathiNo ratings yet

- Chapter1: Introduction: Nonperforming Asset in BankDocument35 pagesChapter1: Introduction: Nonperforming Asset in BankMaridasrajanNo ratings yet

- A Study of Non Performing Assets in Bank of BarodaDocument68 pagesA Study of Non Performing Assets in Bank of BarodaSuryaNo ratings yet

- NpaDocument19 pagesNpasayantanpatra100% (1)

- Definition of Npas: A NPA Is A Loan or An Advance WhereDocument30 pagesDefinition of Npas: A NPA Is A Loan or An Advance WheremulchandranaNo ratings yet

- Management of Non-Performing Assets: Presentation by Mr. S. RaviDocument29 pagesManagement of Non-Performing Assets: Presentation by Mr. S. RaviRajesh MaddiNo ratings yet

- A Study of Non Performing Assets in Bank of BarodaDocument68 pagesA Study of Non Performing Assets in Bank of BarodaMohamed Tousif81% (21)

- Final ReportDocument39 pagesFinal ReportBhupendra KushwahaNo ratings yet

- Non Performing AssetsDocument24 pagesNon Performing AssetsAmarjeet DhobiNo ratings yet

- Babinpa 131210023706 Phpapp01Document32 pagesBabinpa 131210023706 Phpapp01KETANNo ratings yet

- Final EditDocument24 pagesFinal EditSapla IngiNo ratings yet

- What Is NPADocument4 pagesWhat Is NPAAmishaNo ratings yet

- Npa 119610079679343 5Document46 pagesNpa 119610079679343 5Teju AshuNo ratings yet

- NPA & Income RecognitionDocument56 pagesNPA & Income RecognitionDrashti Raichura100% (1)

- Asset Quality, Credit Delivery and Management FinalDocument21 pagesAsset Quality, Credit Delivery and Management FinalDebanjan DasNo ratings yet

- Recovery of LoansDocument50 pagesRecovery of LoansRajul AgrawalNo ratings yet

- Non-Performing Assets (NPA) : Asset Classification, Income Recognition and Provisioning NormsDocument52 pagesNon-Performing Assets (NPA) : Asset Classification, Income Recognition and Provisioning Normspriyankaarora9010No ratings yet

- NPA NotesDocument33 pagesNPA NotesAdv Sheetal SaylekarNo ratings yet

- Term Paper Banking and InsuranceDocument27 pagesTerm Paper Banking and InsuranceneenajoshiNo ratings yet

- Management of Stressed AssetsDocument17 pagesManagement of Stressed AssetsRamakrishnan AnantapadmanabhanNo ratings yet

- BRM Session 3Document38 pagesBRM Session 3Saksham BavejaNo ratings yet

- Impact of Non-Performing Assets On Banking Industry: The Indian PerspectiveDocument8 pagesImpact of Non-Performing Assets On Banking Industry: The Indian Perspectiveshubham kumarNo ratings yet

- Non Performing Assets (Npa) : K.ShaliniDocument50 pagesNon Performing Assets (Npa) : K.ShalinipavvvvvviNo ratings yet

- Problem FormulationDocument35 pagesProblem FormulationJewel Binoy100% (1)

- (Non Performing Assets) : Commercial Banks Assets Are of Various Types Such AsDocument15 pages(Non Performing Assets) : Commercial Banks Assets Are of Various Types Such AsChaarvi ShridherNo ratings yet

- NPA AnalysisDocument61 pagesNPA AnalysisSabyasachi PandaNo ratings yet

- Institute - Usb Department - BbaDocument20 pagesInstitute - Usb Department - BbaAmanNo ratings yet

- A Study On Npa of Public Sector Banks in India: Sulagna Das, AbhijitduttaDocument9 pagesA Study On Npa of Public Sector Banks in India: Sulagna Das, AbhijitduttaSunil Kumar PalikelaNo ratings yet

- Management of Non-Performing Assets: K K Jindal Managing Director Global Management Services New DelhiDocument34 pagesManagement of Non-Performing Assets: K K Jindal Managing Director Global Management Services New DelhiNoor Preet KaurNo ratings yet

- Prudential NormsDocument24 pagesPrudential NormsProf. Amit kashyapNo ratings yet

- Mob NpaDocument44 pagesMob NpaParthNo ratings yet

- Recovery Policy - 2012Document23 pagesRecovery Policy - 2012Dhawan SandeepNo ratings yet

- Literature ReviewDocument21 pagesLiterature ReviewGaurav JaiswalNo ratings yet

- Liquidity ManagementDocument35 pagesLiquidity ManagementJadMadiNo ratings yet

- Chapter - I: Non-Performing AssetDocument46 pagesChapter - I: Non-Performing AssetVigneshwaran BbaNo ratings yet

- Npa in SbiDocument96 pagesNpa in SbiApoorva M V100% (2)

- Simer Project On Non Performing Assets..Document61 pagesSimer Project On Non Performing Assets..Simer KaurNo ratings yet

- NPAkjhhkjhkjhjhjDocument54 pagesNPAkjhhkjhkjhjhjRintu AbrahamNo ratings yet

- NPA Management by Indian Banks-LATEST: Dr. Deepak Tandon IMI New DelhiDocument40 pagesNPA Management by Indian Banks-LATEST: Dr. Deepak Tandon IMI New Delhidev mhaispurkarNo ratings yet

- Sayali ProjectDocument63 pagesSayali ProjecthemangiNo ratings yet

- Introduction of The TopicDocument8 pagesIntroduction of The TopicPooja AgarwalNo ratings yet

- The Entrepreneur’S Dictionary of Business and Financial TermsFrom EverandThe Entrepreneur’S Dictionary of Business and Financial TermsNo ratings yet

- Textbook of Urgent Care Management: Chapter 46, Urgent Care Center FinancingFrom EverandTextbook of Urgent Care Management: Chapter 46, Urgent Care Center FinancingNo ratings yet

- Financial Control Blueprint: Building a Path to Growth and SuccessFrom EverandFinancial Control Blueprint: Building a Path to Growth and SuccessNo ratings yet

- Business Topics 1Document40 pagesBusiness Topics 1MCL EnglishNo ratings yet

- Contents of Project ProposalDocument2 pagesContents of Project ProposalFatima Razzaq100% (1)

- Issues and Challenges in Service MarketingDocument10 pagesIssues and Challenges in Service MarketingDivya GirishNo ratings yet

- CRISIL Mutual Fund Ranking Methodology Dec 2015Document5 pagesCRISIL Mutual Fund Ranking Methodology Dec 2015krajeshkumarxNo ratings yet

- BACOSTMX - Module 5 Part 2 - Lecture - Joint and by Product PDFDocument55 pagesBACOSTMX - Module 5 Part 2 - Lecture - Joint and by Product PDFDiane Cris DuqueNo ratings yet

- Introduction To Agricultural AccountingDocument54 pagesIntroduction To Agricultural AccountingManal ElkhoshkhanyNo ratings yet

- RoseDocument4 pagesRosePriyanka GirdariNo ratings yet

- Cambridge O Level: Accounting 7707/21 May/June 2020Document18 pagesCambridge O Level: Accounting 7707/21 May/June 2020Jack KowmanNo ratings yet

- Capgemini SpeakUpPolicy EnglishDocument13 pagesCapgemini SpeakUpPolicy EnglishGokul ChidambaramNo ratings yet

- FSCM Configuration Document - 1Document72 pagesFSCM Configuration Document - 1sachin nagpureNo ratings yet

- HDFC Bank DDPI - Resident Ver 2 - 17102022Document4 pagesHDFC Bank DDPI - Resident Ver 2 - 17102022riddhi SalviNo ratings yet

- Social Media Marketing and Digital Marketing ProjectDocument67 pagesSocial Media Marketing and Digital Marketing ProjectDivye Sharma50% (2)

- 201 - MM - Unit-3,4,5 MCQsDocument19 pages201 - MM - Unit-3,4,5 MCQsDilip PawarNo ratings yet

- Marketing Plan THYDocument17 pagesMarketing Plan THYnik_singerstr83% (6)

- Ecommerce ProjectDocument20 pagesEcommerce ProjectKumar BasnetNo ratings yet

- Performance Evaluation and CompensationDocument34 pagesPerformance Evaluation and CompensationarunprasadvrNo ratings yet

- CONCEPTUAL FRAMEWORK and ACCOUNTING STANDARD - OUTLINEDocument11 pagesCONCEPTUAL FRAMEWORK and ACCOUNTING STANDARD - OUTLINEBABANo ratings yet

- Vending Services Business PlanDocument40 pagesVending Services Business PlanLiudmyla ShersheniukNo ratings yet

- (TSJ) Bde Mv50kmt 190214 (Bony)Document2 pages(TSJ) Bde Mv50kmt 190214 (Bony)TMJNo ratings yet

- Process Costing Study GuideDocument14 pagesProcess Costing Study GuideTekaling NegashNo ratings yet

- Bmy S4CLD2111 BPD en FRDocument45 pagesBmy S4CLD2111 BPD en FRjihanemkaNo ratings yet

- Stock DividendsDocument7 pagesStock DividendsShaan HashmiNo ratings yet

- Industrial Visit)Document10 pagesIndustrial Visit)ZISHAN ALI-RM 21RM966No ratings yet

- Insur XDocument15 pagesInsur XJuan CumbradoNo ratings yet

- Circular 02 2020Document154 pagesCircular 02 2020jonnydeep1970virgilio.itNo ratings yet

- Sarah Chey's ResumeDocument1 pageSarah Chey's Resumeca8sarah15No ratings yet

- Production and Operation ManagementDocument19 pagesProduction and Operation Managementjuliobueno8974No ratings yet

- Sponsor and Commercial Partner - Stadium Naming Rights: BackgroundDocument1 pageSponsor and Commercial Partner - Stadium Naming Rights: BackgroundRiza El HakimNo ratings yet

- Aprds Safety ValveDocument2 pagesAprds Safety ValveMandeep SinghNo ratings yet

- Chapter 2 ExerciseDocument5 pagesChapter 2 Exercisegirlyn abadillaNo ratings yet