You might also like

- Rohit Summer Internship Report.....Document69 pagesRohit Summer Internship Report.....Manas Pandey100% (2)

- E Commerce Indian ScenarioDocument2 pagesE Commerce Indian ScenarioVishal BansodeNo ratings yet

- Abstract RetailDocument9 pagesAbstract Retailmoorthi_psNo ratings yet

- FIRSTCRYDocument10 pagesFIRSTCRYrey cedricNo ratings yet

- 14.2 Myntra - Com - B-Plan SummaryDocument40 pages14.2 Myntra - Com - B-Plan SummaryNikita Agarwal100% (1)

- A Comparative Study Between Flipkart and Amazon IndiaDocument33 pagesA Comparative Study Between Flipkart and Amazon IndiaRupal Rohan DalalNo ratings yet

- Analysis of Firstcry.com's Business Model and Strategy in the Indian E-retailing IndustryDocument50 pagesAnalysis of Firstcry.com's Business Model and Strategy in the Indian E-retailing IndustryRainee KocharNo ratings yet

- 212f1475 Naan MudhalvanDocument18 pages212f1475 Naan Mudhalvanswesow753No ratings yet

- Ecommerce in IndiaDocument78 pagesEcommerce in IndiaArvind Sanu Misra100% (2)

- Project Report: Submitted in Partial Fulfillment of The Degree of Masters of Business Administration Session (2016-2017)Document69 pagesProject Report: Submitted in Partial Fulfillment of The Degree of Masters of Business Administration Session (2016-2017)Shahrukh Khan100% (1)

- A Comparative Study Between Flipkart and Amazon IndiaDocument11 pagesA Comparative Study Between Flipkart and Amazon Indiaprashant chavanNo ratings yet

- Unique Pricing Strategies of FlipkartDocument3 pagesUnique Pricing Strategies of Flipkartpari shuklaNo ratings yet

- E Commerce in India Literature ReviewDocument54 pagesE Commerce in India Literature ReviewShahnoor Hossain50% (2)

- Coustmer-Perception Towards-FlipkartDocument69 pagesCoustmer-Perception Towards-Flipkartprabhujaya97893No ratings yet

- Marketing Plan (2012)Document16 pagesMarketing Plan (2012)Suneita0% (1)

- FROM AMAZON TO ALIBABA: THE RISE OF FLIPKARTDocument24 pagesFROM AMAZON TO ALIBABA: THE RISE OF FLIPKARTPrav Ebe RichNo ratings yet

- FlipkartDocument18 pagesFlipkartwww_suhaylan100% (2)

- E-Commerce Fundamentals for BBA StudentsDocument56 pagesE-Commerce Fundamentals for BBA StudentsGaurav VikalNo ratings yet

- Report On Online ShoppingDocument179 pagesReport On Online ShoppingKeval PatelNo ratings yet

- Social Media Strategies For OnlineDocument69 pagesSocial Media Strategies For OnlineNamitaGupta100% (2)

- ACKNOWLEDGEMENTDocument90 pagesACKNOWLEDGEMENTanon_586799434No ratings yet

- Marketing Strategy of FlipkartDocument32 pagesMarketing Strategy of FlipkartGaurav SinghNo ratings yet

- A Research Project Report On "Comparative Analysis of Marketing Strategy of Nestle, Amul & Cadbury Chocolates"Document47 pagesA Research Project Report On "Comparative Analysis of Marketing Strategy of Nestle, Amul & Cadbury Chocolates"Anonymous UWMOBhDiNo ratings yet

- Detailed Literature Review of Multilevel Marketing ComponentsDocument12 pagesDetailed Literature Review of Multilevel Marketing ComponentsSameedAsgharKhanNo ratings yet

- Study On Customer Satisfaction Regarding E-Commerce CompanyDocument65 pagesStudy On Customer Satisfaction Regarding E-Commerce CompanyShweta RajputNo ratings yet

- Case On:: What Lies in Store For The Retailing Industry in India?Document26 pagesCase On:: What Lies in Store For The Retailing Industry in India?gagandeep4everNo ratings yet

- Project On Vishal MegamartDocument69 pagesProject On Vishal MegamartMohit Kumar100% (1)

- First CryDocument4 pagesFirst CrysamikshaNo ratings yet

- Myntra's acquisition by Flipkart to compete against Amazon in Indian e-commerceDocument4 pagesMyntra's acquisition by Flipkart to compete against Amazon in Indian e-commerceLovEly LOoksNo ratings yet

- Working Capital Management Techniques at Tata SteelDocument19 pagesWorking Capital Management Techniques at Tata SteelRam ChandNo ratings yet

- Online Marketing Strategies For Increasing Sales Revenues of SmalDocument148 pagesOnline Marketing Strategies For Increasing Sales Revenues of SmalTugonon M Leo Roswald100% (1)

- Internship Report on Comparing E-commerce GiantsDocument57 pagesInternship Report on Comparing E-commerce Giantssruthy satheesan100% (1)

- Digital Marketing Project ReportDocument53 pagesDigital Marketing Project ReportharshalNo ratings yet

- Consumer Behavior Project On Big Bazaar QuestionnaireDocument16 pagesConsumer Behavior Project On Big Bazaar Questionnairesarvottema67% (3)

- Case AnalysisDocument9 pagesCase Analysiskeerthan sunnyNo ratings yet

- 61497b8bcf903 Stylbiz 2021 - Problem StatementDocument4 pages61497b8bcf903 Stylbiz 2021 - Problem StatementAniket DograNo ratings yet

- Big Bazaar Project FOR BMSDocument31 pagesBig Bazaar Project FOR BMSSAURABHNo ratings yet

- Organised Retail Industry Growth in IndiaDocument56 pagesOrganised Retail Industry Growth in IndiaAkshat Kapoor100% (1)

- Evolution of Rural MarketingDocument25 pagesEvolution of Rural MarketingttirvNo ratings yet

- Bata Marketing MixDocument23 pagesBata Marketing Mixmazhar453038No ratings yet

- Online ShoppingDocument7 pagesOnline ShoppingIkjot JoharNo ratings yet

- Case Study-Azz FoodsDocument11 pagesCase Study-Azz FoodsAli HussainNo ratings yet

- FlipkartDocument25 pagesFlipkartAbhishek Kumar0% (1)

- Priyanka (02714188818) Project..Document88 pagesPriyanka (02714188818) Project..Priyanka ChauhanNo ratings yet

- A Study On Customer Awareness and Satisfaction Towards Flipkart Shopping - With Special Reference To Pollachi TalukDocument4 pagesA Study On Customer Awareness and Satisfaction Towards Flipkart Shopping - With Special Reference To Pollachi TalukMukul SomgadeNo ratings yet

- Project Traditional Retailing WithDocument44 pagesProject Traditional Retailing WithChaitanya Kasi0% (1)

- Findings: 1. Enabling An Intelligent PlantDocument13 pagesFindings: 1. Enabling An Intelligent PlantMurali Krishna100% (1)

- Ecommerce 1 PDFDocument34 pagesEcommerce 1 PDFtejan shetNo ratings yet

- Hero Honda Marketing ReportDocument155 pagesHero Honda Marketing Reportepost.sb100% (1)

- 4Ps of PantaloonsDocument15 pages4Ps of PantaloonsVibhav BhideNo ratings yet

- Vishal Mega Mart 1 PDFDocument58 pagesVishal Mega Mart 1 PDFbagal07No ratings yet

- Research ProjectDocument18 pagesResearch ProjectAssad NaseerNo ratings yet

- Summer Project Report: Social Media Strategies For Online Shopping Cart in IndiaDocument70 pagesSummer Project Report: Social Media Strategies For Online Shopping Cart in IndiaNAMRATA SHARMANo ratings yet

- ANALYSIS OF ONLINE SHOPPING TRENDSDocument15 pagesANALYSIS OF ONLINE SHOPPING TRENDSDipanita DashNo ratings yet

- Bibliography and QuestionnaireDocument9 pagesBibliography and QuestionnaireprateekNo ratings yet

- Rahul Rbmi Customer Satisfaction Pantaloon FinalDocument55 pagesRahul Rbmi Customer Satisfaction Pantaloon FinalAnonymous YH6N4cpuJzNo ratings yet

- Grant Proposal 1Document4 pagesGrant Proposal 1api-494636648No ratings yet

- SEO Discovery: - Search Engine Optimization: A Summer Internship Report OnDocument28 pagesSEO Discovery: - Search Engine Optimization: A Summer Internship Report OnVISHAL RATHOURNo ratings yet

- Importance of Digital Marketing for StartupsDocument51 pagesImportance of Digital Marketing for StartupsMitesh Bhore Jain81% (16)

- Instagram Perspectives: Summer Report Analyzes Platform ViewsDocument30 pagesInstagram Perspectives: Summer Report Analyzes Platform ViewsSwarup Kumar BeraNo ratings yet

- Nirma's Journey from Humble Beginnings to Market LeaderDocument34 pagesNirma's Journey from Humble Beginnings to Market LeaderSaurav KumarNo ratings yet

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- Presented By: Sidhant Bajaj Ruchika Sharma Shivapriya Siddharth GautamDocument9 pagesPresented By: Sidhant Bajaj Ruchika Sharma Shivapriya Siddharth GautamSaurav KumarNo ratings yet

- Global Mba Ranking 2013Document1 pageGlobal Mba Ranking 2013Saurav KumarNo ratings yet

- Direct Marketing SamsungDocument58 pagesDirect Marketing SamsungSaurav Kumar33% (3)

- Lifebuoy StrategyDocument3 pagesLifebuoy StrategySaurav KumarNo ratings yet

- Gavin Humphries Global Consumer TrendsDocument59 pagesGavin Humphries Global Consumer TrendsSaurav KumarNo ratings yet

- RB Case Study DettolDocument31 pagesRB Case Study DettolNitesh SantNo ratings yet

- Winter Internship ReportDocument39 pagesWinter Internship ReportSaurav KumarNo ratings yet

- LiveMedia FinalDocument28 pagesLiveMedia FinalSaurav KumarNo ratings yet

- Project On Dettol Soap Reckitt and BenckiserDocument14 pagesProject On Dettol Soap Reckitt and Benckiserbipender87% (15)

- Rural marketing strategies of Lifebuoy soapDocument19 pagesRural marketing strategies of Lifebuoy soapSaurav KumarNo ratings yet

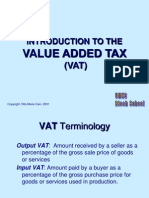

- Introduction to VAT Terminology and E-Commerce IssuesDocument11 pagesIntroduction to VAT Terminology and E-Commerce IssuesSaurav KumarNo ratings yet

- Analysis of BRUDocument25 pagesAnalysis of BRUSaurav KumarNo ratings yet

- Unit-Ii: Socket Address StructuresDocument17 pagesUnit-Ii: Socket Address Structuresakbarviveka_16156616No ratings yet

- How To Reduce Your HANA Database Size by 30% - SAP BlogsDocument12 pagesHow To Reduce Your HANA Database Size by 30% - SAP BlogsivanNo ratings yet

- Adapter Widget Dev GuideDocument22 pagesAdapter Widget Dev GuidePrestoneKNo ratings yet

- Midterm Exam in Gen MathDocument3 pagesMidterm Exam in Gen MathAldyn PintoyNo ratings yet

- Recover Lost Partitions with TestDisk Step-by-Step GuideDocument12 pagesRecover Lost Partitions with TestDisk Step-by-Step GuidezoeksidoNo ratings yet

- DSA Notes Unit 1 To Unit 6Document587 pagesDSA Notes Unit 1 To Unit 6manusheejaudayakumarNo ratings yet

- Counterfactuals by David Lewis Review - Steven E. Boër and William G. LycanDocument8 pagesCounterfactuals by David Lewis Review - Steven E. Boër and William G. LycanTiffany WangNo ratings yet

- PRO192Document218 pagesPRO192Thành NguyễnNo ratings yet

- Oracle Primavera Risk Analysis Overview (Full) 1Document30 pagesOracle Primavera Risk Analysis Overview (Full) 1Igor Čuček33% (3)

- Assignments of CGDocument10 pagesAssignments of CGAshok MallNo ratings yet

- Laptop ListDocument3 pagesLaptop ListKrishna ManoharNo ratings yet

- Production Planning and Control Anna University Question BankDocument4 pagesProduction Planning and Control Anna University Question BankSankar KumarNo ratings yet

- Cryin' Bass Tabs - Aerosmith @Document6 pagesCryin' Bass Tabs - Aerosmith @Deeu LoodNo ratings yet

- GEI100517a-Modbus For HMIsDocument76 pagesGEI100517a-Modbus For HMIscsolorzanop100% (3)

- Stuxnet AnalysisDocument7 pagesStuxnet AnalysisMr .XNo ratings yet

- Opman ReviewerDocument2 pagesOpman ReviewerArkhie DavocolNo ratings yet

- Lab 1: Study of Gates & Flip-Flops: - Digital IC Trainer KitDocument81 pagesLab 1: Study of Gates & Flip-Flops: - Digital IC Trainer KitforghanNo ratings yet

- Has To Be Based On The ADM Estimator Outcome and The Agreed Split of Responsibilities Between Client and AccentureDocument10 pagesHas To Be Based On The ADM Estimator Outcome and The Agreed Split of Responsibilities Between Client and AccentureMOORTHYNo ratings yet

- Unix QuotationDocument8 pagesUnix QuotationJerel John CalanaoNo ratings yet

- Hamming and Huffman Coding Tutorial: by Tom S. LeeDocument6 pagesHamming and Huffman Coding Tutorial: by Tom S. Leewk4lifeNo ratings yet

- CSC C85 Summer 2004: Assembly Language ProgrammingDocument45 pagesCSC C85 Summer 2004: Assembly Language ProgrammingAli AhmadNo ratings yet

- Linear ProgrammingDocument14 pagesLinear ProgrammingJulius Harris FamilaraNo ratings yet

- Kazue Sako (Eds.) ) Topics in Cryptology - CT-RSADocument456 pagesKazue Sako (Eds.) ) Topics in Cryptology - CT-RSANenad Dragan Jovananović100% (1)

- New Microsoft Office Word Document124Document5 pagesNew Microsoft Office Word Document124Abdul Razak KaladgiNo ratings yet

- SDP Deep DiveDocument15 pagesSDP Deep DivenscintaNo ratings yet

- Oasis Montaj 7.2 Viewer: The Core Software Platform For Working With Large Volume Spatial DataDocument0 pagesOasis Montaj 7.2 Viewer: The Core Software Platform For Working With Large Volume Spatial DataJonathan GarciaNo ratings yet

- Multimedia For Learning: Methods and Development (3Th Edition) - Book ReviewDocument7 pagesMultimedia For Learning: Methods and Development (3Th Edition) - Book ReviewKharis MaulanaNo ratings yet

- Instruction Format 8051Document26 pagesInstruction Format 8051alex24arulNo ratings yet

- MATRIX ALGEBRA With MATHEMATICA PDFDocument235 pagesMATRIX ALGEBRA With MATHEMATICA PDFMustapha El MetouiNo ratings yet

- Caching & Compression Blue CoatDocument10 pagesCaching & Compression Blue CoataqibkhanliveNo ratings yet