You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (890)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- WHAT IS A BIRTH CERTIFICATE-Estate Equitable Title Receipt PDFDocument8 pagesWHAT IS A BIRTH CERTIFICATE-Estate Equitable Title Receipt PDFApril Clay75% (4)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- TACTICAL FINANCING DECISIONSDocument24 pagesTACTICAL FINANCING DECISIONSAccounting TeamNo ratings yet

- Concerns with DCF analysis for Intermediate Chemicals Group projectDocument2 pagesConcerns with DCF analysis for Intermediate Chemicals Group projectJia LeNo ratings yet

- AFISCO v. CADocument2 pagesAFISCO v. CASophiaFrancescaEspinosa100% (1)

- MWG GuidanceDocument73 pagesMWG Guidancejordimon1234No ratings yet

- 2015 Copy of Note - HarmonLaw - BryantDocument6 pages2015 Copy of Note - HarmonLaw - BryantTim Bryant100% (2)

- GSMSC Certificate - Involuntary RevokationDocument2 pagesGSMSC Certificate - Involuntary RevokationTim BryantNo ratings yet

- 2013 Copy of Note - HarmonLaw - BryantDocument6 pages2013 Copy of Note - HarmonLaw - BryantTim BryantNo ratings yet

- Note and Rider 2005Document8 pagesNote and Rider 2005Tim BryantNo ratings yet

- Extracting Signatures From Bank Checks - 2003Document10 pagesExtracting Signatures From Bank Checks - 2003Tim BryantNo ratings yet

- EFF - DocuColor Tracking Dot Decoding GuideDocument6 pagesEFF - DocuColor Tracking Dot Decoding GuideTim BryantNo ratings yet

- Mortgages Notes Deeds and Loans in Crime-Gary MichaelsDocument15 pagesMortgages Notes Deeds and Loans in Crime-Gary MichaelsTim Bryant100% (2)

- Mortgage Page 10 - Line Through SignatureDocument1 pageMortgage Page 10 - Line Through SignatureTim BryantNo ratings yet

- Harmon Notice of Foreclosure Sale - 05 22 2015 - HIGHLIGHTEDDocument10 pagesHarmon Notice of Foreclosure Sale - 05 22 2015 - HIGHLIGHTEDTim BryantNo ratings yet

- BofA To Nationstar 07 30 2013-80 BradfordDocument1 pageBofA To Nationstar 07 30 2013-80 BradfordTim BryantNo ratings yet

- Print Over SignatureDocument2 pagesPrint Over SignatureTim Bryant100% (2)

- Affidavits of Title - EXECUTED - 06 26 2015Document10 pagesAffidavits of Title - EXECUTED - 06 26 2015Tim BryantNo ratings yet

- FRB Report - 100517-Clearing Banks As Loan Funders-BONYDocument43 pagesFRB Report - 100517-Clearing Banks As Loan Funders-BONYTim BryantNo ratings yet

- Pinti V Emigrant 2015-Sjc-11742Document44 pagesPinti V Emigrant 2015-Sjc-11742Tim BryantNo ratings yet

- Paths of Notes and Mortgages - Loan 114726037Document24 pagesPaths of Notes and Mortgages - Loan 114726037Tim BryantNo ratings yet

- MA OCR - Mortgage Lending in Licensed Name Only-Summary of Selected Opinion 99-026Document1 pageMA OCR - Mortgage Lending in Licensed Name Only-Summary of Selected Opinion 99-026Tim BryantNo ratings yet

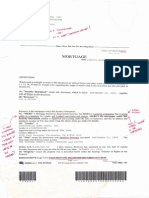

- Closing Version Mortgage-Rider 2005 BryantDocument16 pagesClosing Version Mortgage-Rider 2005 BryantTim BryantNo ratings yet

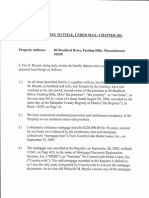

- Bryant Mortgage 2005 - RODDocument16 pagesBryant Mortgage 2005 - RODTim BryantNo ratings yet

- MERS To BAC Assignment 05 11 2011Document1 pageMERS To BAC Assignment 05 11 2011Tim BryantNo ratings yet

- GSAA Home Equity Trust 2005-15 / Received Mortgage Assignment 7 Yrs After Closing Date of The Trust.Document1 pageGSAA Home Equity Trust 2005-15 / Received Mortgage Assignment 7 Yrs After Closing Date of The Trust.Tim BryantNo ratings yet

- Bryant Mortgage PG 2Document1 pageBryant Mortgage PG 2Tim BryantNo ratings yet

- Nationstar Poa For HSBC Gsaa Het 2005-15-2014 HcrodDocument7 pagesNationstar Poa For HSBC Gsaa Het 2005-15-2014 HcrodTim BryantNo ratings yet

- Deutsche Bank National Trust Is Not Registered To Do Business in MADocument1 pageDeutsche Bank National Trust Is Not Registered To Do Business in MATim BryantNo ratings yet

- DBNT Not Registered To Do Business in NYDocument1 pageDBNT Not Registered To Do Business in NYTim BryantNo ratings yet

- GS Mortgage Securities Corp Not Authorized To Do Business in NYDocument1 pageGS Mortgage Securities Corp Not Authorized To Do Business in NYTim BryantNo ratings yet

- GSAA HET 2005 15 Not Registered To Do Business in MADocument2 pagesGSAA HET 2005 15 Not Registered To Do Business in MATim BryantNo ratings yet

- GSAA HET 2005 15 Not Registered To Do Business in NYDocument1 pageGSAA HET 2005 15 Not Registered To Do Business in NYTim BryantNo ratings yet

- A0T0CZ - GSAA Home Equity Trust 2005-15 Bond - 0.437% Until 01-25-2036 - FinanzenDocument3 pagesA0T0CZ - GSAA Home Equity Trust 2005-15 Bond - 0.437% Until 01-25-2036 - FinanzenTim BryantNo ratings yet

- Foundation MCQ 2012Document337 pagesFoundation MCQ 2012Prasenjit Sutradhar100% (1)

- Session 2-3 Interest Rate RiskDocument79 pagesSession 2-3 Interest Rate RiskGodfrey MacwanNo ratings yet

- 29 - IV TrimesterDocument27 pages29 - IV Trimestersivaraj278No ratings yet

- Impact of Financial Technology On Payment and Lending in AsiaDocument19 pagesImpact of Financial Technology On Payment and Lending in AsiaADBI EventsNo ratings yet

- Lecture 10 - Prospective Analysis - ForecastingDocument15 pagesLecture 10 - Prospective Analysis - ForecastingTrang Bùi Hà100% (1)

- DuPont Analysis On JNJDocument7 pagesDuPont Analysis On JNJviettuan91No ratings yet

- BFC5935 - Tutorial 3 Solutions PDFDocument6 pagesBFC5935 - Tutorial 3 Solutions PDFXue XuNo ratings yet

- Business Management EXTENDED ESSAY TITLESDocument6 pagesBusiness Management EXTENDED ESSAY TITLESS RameshNo ratings yet

- Review Jurnal Psikologi The LONG MEMORYDocument4 pagesReview Jurnal Psikologi The LONG MEMORYDiah Dwi Putri IriantoNo ratings yet

- Sri Lanka, CBSLDocument24 pagesSri Lanka, CBSLVyasIRMANo ratings yet

- Indian Salon Industry ReportDocument26 pagesIndian Salon Industry ReportReevolv Advisory Services Private Limited0% (1)

- ABM - Fundamentals of ABM 2 CGDocument6 pagesABM - Fundamentals of ABM 2 CGKassandra KayNo ratings yet

- Green Brick Partners, Inc. GRBK - The Best Kept Secret On Wall StreetDocument3 pagesGreen Brick Partners, Inc. GRBK - The Best Kept Secret On Wall StreetThe Focused Stock TraderNo ratings yet

- Presentation Hybrid MismatchDocument9 pagesPresentation Hybrid MismatchAbdul SattarNo ratings yet

- Tourism in Africa:: Harnessing Tourism For Growth and Improved LivelihoodsDocument12 pagesTourism in Africa:: Harnessing Tourism For Growth and Improved LivelihoodsDIPIN PNo ratings yet

- Women EntrepreneursDocument34 pagesWomen EntrepreneursANUP RNo ratings yet

- Ctset Research Systems: This Is The Limited Version of The Factset Research Systems Company ProfileDocument12 pagesCtset Research Systems: This Is The Limited Version of The Factset Research Systems Company ProfileSri HariniNo ratings yet

- Pel ReportDocument98 pagesPel Reportmr_hailian786100% (2)

- Development in Banking SectorDocument1 pageDevelopment in Banking Sectorhafiz1979No ratings yet

- Liquidity, Asset Management, Cost, and Profitability Ratios AnalysisDocument3 pagesLiquidity, Asset Management, Cost, and Profitability Ratios Analysisnicolaus copernicusNo ratings yet

- Taxonomy of Finance Theories and Their ImplicationsDocument16 pagesTaxonomy of Finance Theories and Their ImplicationsDr. Vernon T Cox0% (1)

- Uconn Foundation: Investment ManagementDocument35 pagesUconn Foundation: Investment ManagementBoqorka AmericaNo ratings yet

- Capital Structure MSCIDocument10 pagesCapital Structure MSCIinam ullahNo ratings yet

- Financial Statement Analysis - NestleDocument18 pagesFinancial Statement Analysis - NestleLukshman Rao Rao75% (4)

- ACT312 Quiz1 Online-1 PDFDocument6 pagesACT312 Quiz1 Online-1 PDFCharlie Harris0% (1)

- Keynes' Theory of Effective Demand and Underemployment EquilibriumDocument4 pagesKeynes' Theory of Effective Demand and Underemployment EquilibriumjohnpaulcorpusNo ratings yet