You might also like

- RJR Nabisco Special Committee Members and AdvisorsDocument13 pagesRJR Nabisco Special Committee Members and AdvisorsRattan Preet Singh25% (4)

- Time Management AnalysisDocument1 pageTime Management AnalysisAnkur AgarwalNo ratings yet

- Students Management FrameworkDocument7 pagesStudents Management FrameworkAnkur AgarwalNo ratings yet

- Cognizant ReportDocument2 pagesCognizant ReportAnkur AgarwalNo ratings yet

- MFI RegulationsDocument2 pagesMFI RegulationsAnkur AgarwalNo ratings yet

- Class Groups (E)Document2 pagesClass Groups (E)Ankur AgarwalNo ratings yet

- Globalization AssignmentDocument2 pagesGlobalization AssignmentAnkur AgarwalNo ratings yet

- CFCL - SR 2010-11 (Live Responsibly - Final)Document84 pagesCFCL - SR 2010-11 (Live Responsibly - Final)Ankur AgarwalNo ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5784)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (890)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (72)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Poultry FarmDocument22 pagesPoultry Farmrisingprince89No ratings yet

- CheckwritingDocument2 pagesCheckwritingLiz Pasillas100% (6)

- Chapter 2 Macro SolutionDocument16 pagesChapter 2 Macro Solutionsaurabhsaurs80% (10)

- Datapoint Business Plan Diamond BankDocument25 pagesDatapoint Business Plan Diamond BankCyril Justus EkpoNo ratings yet

- Practice Exam Chapter 6-9Document4 pagesPractice Exam Chapter 6-9John Arvi ArmildezNo ratings yet

- International Management: An IntroductionDocument22 pagesInternational Management: An IntroductionTeodoro Criscione100% (1)

- Manufacturing Shampoo Project ProfileDocument2 pagesManufacturing Shampoo Project Profilevineetaggarwal50% (2)

- An Introduction To SwapsDocument5 pagesAn Introduction To SwapsCh RajkamalNo ratings yet

- Lbo Model Short FormDocument6 pagesLbo Model Short FormHeu Sai HoeNo ratings yet

- East Hill Home Healthcare Services Was Organized On January 1Document1 pageEast Hill Home Healthcare Services Was Organized On January 1trilocksp SinghNo ratings yet

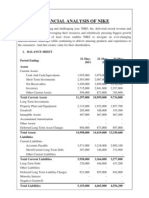

- Financial Analysis of NikeDocument5 pagesFinancial Analysis of NikenimmymathewpkkthlNo ratings yet

- HTTP WWW - Fciweb.nic - in RTI DOP-Adm Powers - HTMDocument4 pagesHTTP WWW - Fciweb.nic - in RTI DOP-Adm Powers - HTMNeha SharmaNo ratings yet

- Top - 100 Outsourcing Location Ranking - 2013 Tholons PDFDocument11 pagesTop - 100 Outsourcing Location Ranking - 2013 Tholons PDFvendetta82pgNo ratings yet

- Joint Venture PPT FinalDocument13 pagesJoint Venture PPT FinalKazi Taher SiddiqueeyNo ratings yet

- Fundraising Best Practices: 2020 EditionDocument23 pagesFundraising Best Practices: 2020 EditionFounder InstituteNo ratings yet

- A Study On The Investment Avenues For Indian InvestorDocument86 pagesA Study On The Investment Avenues For Indian Investormohd aleem50% (4)

- Analyzing Financial Data: Ratio AnalysisDocument12 pagesAnalyzing Financial Data: Ratio AnalysiscpdNo ratings yet

- FI Document: List of Update Terminations: SA38 SE38Document11 pagesFI Document: List of Update Terminations: SA38 SE38Manohar G ShankarNo ratings yet

- Brett Ishler ResumeDocument3 pagesBrett Ishler ResumebishlerNo ratings yet

- JLL Zuidas Office Market Monitor 2014 Q4 DEFDocument16 pagesJLL Zuidas Office Market Monitor 2014 Q4 DEFvdmaraNo ratings yet

- What Is An Extended TrialDocument19 pagesWhat Is An Extended TrialocalmaviliNo ratings yet

- Commodity Channel IndexDocument45 pagesCommodity Channel IndexVarlei Rezer100% (2)

- Chapter 6 - Slides HittDocument24 pagesChapter 6 - Slides HittNur ShafieQahNo ratings yet

- TCS-Registration Process - User Flow DocumentDocument8 pagesTCS-Registration Process - User Flow DocumentMadhan kumarNo ratings yet

- Assignment 2Document3 pagesAssignment 2KARLANo ratings yet

- Uncertainty and Risk Analysis in Petroleum Exploration and ProductionDocument12 pagesUncertainty and Risk Analysis in Petroleum Exploration and ProductionOladimeji TaiwoNo ratings yet

- Presented By: Presented By: - Rohit Goel Rohit Goel (M.B.A. HONS. 2.2) (M.B.A. HONS. 2.2) Roll No ROLL NO - 2207 2207Document12 pagesPresented By: Presented By: - Rohit Goel Rohit Goel (M.B.A. HONS. 2.2) (M.B.A. HONS. 2.2) Roll No ROLL NO - 2207 2207meetrohitgoel0% (1)

- Goat Farm BudgetingDocument9 pagesGoat Farm Budgetingqfarms100% (1)

- Mrs. StoneDocument11 pagesMrs. StonespanischkindNo ratings yet

- Unisa PDFDocument325 pagesUnisa PDFzukiswa0% (1)