You might also like

- (KRX) Management+Plan+for+Algorithmic+Trading (1) Algorithmic Trading in The KRX Derivatives MarketDocument27 pages(KRX) Management+Plan+for+Algorithmic+Trading (1) Algorithmic Trading in The KRX Derivatives MarketJay LeeNo ratings yet

- Algo Trading Case StudyDocument2 pagesAlgo Trading Case Studyreev011No ratings yet

- MS&E448: Statistical Arbitrage: Group 5: Carolyn Soo, Zhengyi Lian, Jiayu Lou, Hang YangDocument31 pagesMS&E448: Statistical Arbitrage: Group 5: Carolyn Soo, Zhengyi Lian, Jiayu Lou, Hang Yang123No ratings yet

- A Dynamic Model of The Limit Order Book: Ioanid Ros UDocument41 pagesA Dynamic Model of The Limit Order Book: Ioanid Ros Upinokio504No ratings yet

- The Value of Queue Position in A Limit Order BookDocument48 pagesThe Value of Queue Position in A Limit Order Bookadeka1100% (1)

- Fixed Income SecuritiesDocument3 pagesFixed Income SecuritiesPRAPTI TIWARINo ratings yet

- The Grossman–Miller Market Making Model with and without Trading CostsDocument18 pagesThe Grossman–Miller Market Making Model with and without Trading CostsvickyNo ratings yet

- Darryl Shen - OrderImbalanceStrategy PDFDocument70 pagesDarryl Shen - OrderImbalanceStrategy PDFmichaelguan326No ratings yet

- Manage Risk with Order TypesDocument31 pagesManage Risk with Order TypesChristian Nicolaus MbiseNo ratings yet

- Limit Order Book Model For Latency ArbitrageDocument28 pagesLimit Order Book Model For Latency ArbitrageJong-Kwon LeeNo ratings yet

- CH 3Document8 pagesCH 3z_k_j_vNo ratings yet

- Microstructure Stock MarketDocument10 pagesMicrostructure Stock Marketmirando93No ratings yet

- Trading 101 BasicsDocument3 pagesTrading 101 BasicsNaveen KumarNo ratings yet

- Risk HFT FlyerDocument20 pagesRisk HFT FlyerYongho ShinNo ratings yet

- FCF Ch02 Excel Master StudentDocument24 pagesFCF Ch02 Excel Master Studentannu technologyNo ratings yet

- Trading Baskets ImplementationDocument44 pagesTrading Baskets ImplementationSanchit Gupta100% (1)

- High Frequency Market Making Model Analyzes Liquidity ProvisionDocument72 pagesHigh Frequency Market Making Model Analyzes Liquidity ProvisionIrfan SihabNo ratings yet

- Algo Trading Intro 2013 Steinki Session 8 PDFDocument21 pagesAlgo Trading Intro 2013 Steinki Session 8 PDFMichael ARKNo ratings yet

- Deep HedgingDocument21 pagesDeep HedgingRaju KaliperumalNo ratings yet

- Survey of Microstructure of Fixed Income Market PDFDocument46 pagesSurvey of Microstructure of Fixed Income Market PDF11: 11100% (1)

- Maker TakerDocument50 pagesMaker TakerEduardo TocchettoNo ratings yet

- Zero Hold Time - FAQs PDFDocument4 pagesZero Hold Time - FAQs PDFJorge LuisNo ratings yet

- Market Microstructure PDFDocument13 pagesMarket Microstructure PDFHarun Ahad100% (2)

- Day Trading Guide to High Probability StrategiesDocument3 pagesDay Trading Guide to High Probability StrategiesAbhishek SharmaNo ratings yet

- HFT New PaperDocument19 pagesHFT New Papersgruen9903No ratings yet

- How To Play The: FlatteningDocument7 pagesHow To Play The: FlatteningThea LandichoNo ratings yet

- A Brief Introduction On Swaps: UQ Business SchoolDocument44 pagesA Brief Introduction On Swaps: UQ Business SchoolSaitou HidekiNo ratings yet

- Questionable Legality of High-Speed Trading TacticsDocument92 pagesQuestionable Legality of High-Speed Trading Tacticslanassa2785No ratings yet

- MarketMaking Models - SummaryDocument35 pagesMarketMaking Models - SummaryRemoCPINo ratings yet

- Class 23: Fixed Income, Interest Rate SwapsDocument21 pagesClass 23: Fixed Income, Interest Rate SwapsKarya BangunanNo ratings yet

- UMDF MarketDataSpecification v2.1.7 PDFDocument75 pagesUMDF MarketDataSpecification v2.1.7 PDFSandieNo ratings yet

- Ts Algo SurveyDocument16 pagesTs Algo Surveyprasadpatankar9No ratings yet

- Order Flow TradingDocument15 pagesOrder Flow TradingOUEDRAOGO RolandNo ratings yet

- Futures vs forwards differencesDocument5 pagesFutures vs forwards differencesSam JamtshoNo ratings yet

- Valuaton and Risk Models - Questions and AnswersDocument335 pagesValuaton and Risk Models - Questions and Answerssneha prakashNo ratings yet

- Earnings Theory PaperDocument64 pagesEarnings Theory PaperPrateek SabharwalNo ratings yet

- Market vs Limit Orders: Understanding Execution UncertaintyDocument19 pagesMarket vs Limit Orders: Understanding Execution UncertaintyAshna0188No ratings yet

- Systemic Liquidity Risk and Bipolar Markets: Wealth Management in Today's Macro Risk On / Risk Off Financial EnvironmentFrom EverandSystemic Liquidity Risk and Bipolar Markets: Wealth Management in Today's Macro Risk On / Risk Off Financial EnvironmentNo ratings yet

- Crypto Dashboard: Track Prices, Metrics & PortfolioDocument43 pagesCrypto Dashboard: Track Prices, Metrics & PortfolioPeterNo ratings yet

- What Is Position Delta - Options Trading Concept Guide - ProjectoptionDocument9 pagesWhat Is Position Delta - Options Trading Concept Guide - Projectoptionjose58No ratings yet

- Trading From Private Consumer Survey Data - Machine Learning Meets Survey Research (Talk at Columbia, Feb. 2020)Document24 pagesTrading From Private Consumer Survey Data - Machine Learning Meets Survey Research (Talk at Columbia, Feb. 2020)Graham GillerNo ratings yet

- Valdi Algo Trading Complex MapDocument12 pagesValdi Algo Trading Complex MaptabbforumNo ratings yet

- WorldQuant TutorialDocument14 pagesWorldQuant TutorialParth GaglaniNo ratings yet

- SMARTS PlatformDocument19 pagesSMARTS Platformoli999No ratings yet

- Understanding Order ProcessDocument7 pagesUnderstanding Order ProcessfilipNo ratings yet

- JPM Flows Liquidity 2016-10-07 2145906Document18 pagesJPM Flows Liquidity 2016-10-07 2145906chaotic_pandemoniumNo ratings yet

- Empirical Market MicrostructureDocument203 pagesEmpirical Market MicrostructureKonstantinos AngelidakisNo ratings yet

- A Practical Guide To Volatility Forecasting Through Calm and StormDocument23 pagesA Practical Guide To Volatility Forecasting Through Calm and StormwillyNo ratings yet

- FX Arbitrage: Capturing Price Differences Across MarketsDocument1 pageFX Arbitrage: Capturing Price Differences Across MarketsKajal ChaudharyNo ratings yet

- Cost of Trading and Clearing OTC Derivatives in The Wake of Margining and Other New Regulations Codex1529Document13 pagesCost of Trading and Clearing OTC Derivatives in The Wake of Margining and Other New Regulations Codex1529Ignasio Pedro Sanches ArguellesNo ratings yet

- Rder Anagement Ystems: Chris Cook Electronic Trading Sales 214-978-4736Document26 pagesRder Anagement Ystems: Chris Cook Electronic Trading Sales 214-978-4736Pinaki MishraNo ratings yet

- Volatility Exchange-Traded Notes - Curse or CureDocument25 pagesVolatility Exchange-Traded Notes - Curse or CurelastkraftwagenfahrerNo ratings yet

- Trade Surveillance QADocument2 pagesTrade Surveillance QAManoj GuptaNo ratings yet

- Research Hub OverviewDocument13 pagesResearch Hub OverviewjndfnsfklNo ratings yet

- CLS Currency Program Briefing BookDocument24 pagesCLS Currency Program Briefing BookNitin NagpureNo ratings yet

- Swap Chapter 1Document18 pagesSwap Chapter 1sudhakarhereNo ratings yet

- Convertible WarrantDocument3 pagesConvertible WarrantrameshkumartNo ratings yet

- Investigation Results On Unfair Securities Trading Practices, First Half 2014 PDFDocument2 pagesInvestigation Results On Unfair Securities Trading Practices, First Half 2014 PDFJay LeeNo ratings yet

- Weekly Market Briefing (April 7, 2014)Document1 pageWeekly Market Briefing (April 7, 2014)Jay LeeNo ratings yet

- Weekly Market Briefing (January 13, 2014)Document1 pageWeekly Market Briefing (January 13, 2014)Jay LeeNo ratings yet

- Weekly Market Briefing (December 30, 2013)Document1 pageWeekly Market Briefing (December 30, 2013)Jay LeeNo ratings yet

- Weekly Market Briefing (July 1, 2013)Document1 pageWeekly Market Briefing (July 1, 2013)Jay LeeNo ratings yet

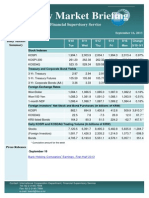

- Weekly Market Briefing (September 16, 2013)Document1 pageWeekly Market Briefing (September 16, 2013)Jay LeeNo ratings yet

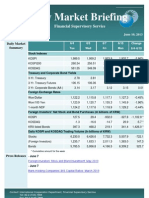

- Weekly Newsletter (September 9, 2013)Document1 pageWeekly Newsletter (September 9, 2013)Jay LeeNo ratings yet

- Derivatives Trading by Financial Companies, 2013Document3 pagesDerivatives Trading by Financial Companies, 2013Jay LeeNo ratings yet

- Weekly Market Briefing (January 6, 2014)Document1 pageWeekly Market Briefing (January 6, 2014)Jay LeeNo ratings yet

- Weekly Newsletter (December 23, 2013, Vol. XIV, No. 51)Document1 pageWeekly Newsletter (December 23, 2013, Vol. XIV, No. 51)Jay LeeNo ratings yet

- Weekly Market Briefing (Aug 12, 2013)Document1 pageWeekly Market Briefing (Aug 12, 2013)Jay LeeNo ratings yet

- Weekly Market Briefing (Aug 7, 2013)Document2 pagesWeekly Market Briefing (Aug 7, 2013)Jay LeeNo ratings yet

- Weekly Market Briefing (September 23, 2013)Document1 pageWeekly Market Briefing (September 23, 2013)Jay LeeNo ratings yet

- Weekly Market Briefing (Aug 26, 2013)Document1 pageWeekly Market Briefing (Aug 26, 2013)Jay LeeNo ratings yet

- Weekly Market Briefing (July 1, 2013)Document1 pageWeekly Market Briefing (July 1, 2013)Jay LeeNo ratings yet

- Weekly Market Briefing (July 22)Document1 pageWeekly Market Briefing (July 22)Jay LeeNo ratings yet

- Weekly Market Briefing (July 1, 2013)Document1 pageWeekly Market Briefing (July 1, 2013)Jay LeeNo ratings yet

- Weekly Market Briefing (July 1, 2013)Document1 pageWeekly Market Briefing (July 1, 2013)Jay LeeNo ratings yet

- Weekly Market Briefing (July 1, 2013)Document1 pageWeekly Market Briefing (July 1, 2013)Jay LeeNo ratings yet

- 24 Weekly Newsletter June 17, 2013Document1 page24 Weekly Newsletter June 17, 2013Jay LeeNo ratings yet

- Weekly Newsletter (June 24, 2013, Vol. XIV, No. 25)Document1 pageWeekly Newsletter (June 24, 2013, Vol. XIV, No. 25)Jay LeeNo ratings yet

- Weekly Market Briefing (July 1, 2013)Document1 pageWeekly Market Briefing (July 1, 2013)Jay LeeNo ratings yet

- Korea Stock Market VolatilityDocument5 pagesKorea Stock Market VolatilityJay LeeNo ratings yet

- Weekly Market Brifing June 10, 2013Document1 pageWeekly Market Brifing June 10, 2013Jay LeeNo ratings yet

- Weekly Newsletter (May 13, 2013, Vol. XIV, No. 19)Document1 pageWeekly Newsletter (May 13, 2013, Vol. XIV, No. 19)Jay LeeNo ratings yet

- Best Execution Policy For Korean ATSDocument5 pagesBest Execution Policy For Korean ATSJay LeeNo ratings yet

- Weekly Market Briefing (June 3, 2013)Document1 pageWeekly Market Briefing (June 3, 2013)Jay LeeNo ratings yet

- Weekly Market Briefing (May 27, 2013, Vol. XIV, No. 21)Document1 pageWeekly Market Briefing (May 27, 2013, Vol. XIV, No. 21)Jay LeeNo ratings yet

- Weekly Newsletter (May 13, 2013, Vol. XIV, No. 19)Document1 pageWeekly Newsletter (May 13, 2013, Vol. XIV, No. 19)Jay LeeNo ratings yet

- Risk Management in The Global EconomyDocument47 pagesRisk Management in The Global EconomyHenry dragoNo ratings yet

- Credit Risk ManagementDocument24 pagesCredit Risk ManagementAl-Imran Bin Khodadad100% (2)

- Audit and assurance homework controls deficiencies recommendationsDocument3 pagesAudit and assurance homework controls deficiencies recommendationsChrisNo ratings yet

- 4D Molecular Therapeutics Reports Full Year 2021 Financial ResultsDocument3 pages4D Molecular Therapeutics Reports Full Year 2021 Financial ResultsMkNo ratings yet

- Bba (Hons) 2016Document156 pagesBba (Hons) 2016Saqib HanifNo ratings yet

- On Financial Frauds and Their Causes Investor OverconfidenceDocument18 pagesOn Financial Frauds and Their Causes Investor Overconfidence1013luisNo ratings yet

- Audit Sampling: An Application To Substantive Tests of Account BalancesDocument57 pagesAudit Sampling: An Application To Substantive Tests of Account Balanceslaurencia raharjoNo ratings yet

- Designing Substantive Procedures: Prepared by DR Phil SajDocument28 pagesDesigning Substantive Procedures: Prepared by DR Phil SajMëŕĕ ĻöľõmãNo ratings yet

- BP Group Process Safety Training: Course AdminDocument9 pagesBP Group Process Safety Training: Course AdminNguyễnTrườngNo ratings yet

- Town Gas PRS Quantitative Risk AssessmentDocument81 pagesTown Gas PRS Quantitative Risk AssessmentDavid ColeNo ratings yet

- CEZ Group Corporate Social Responsibility Report 2010-2011 - enDocument111 pagesCEZ Group Corporate Social Responsibility Report 2010-2011 - enCSRMedia NetworkNo ratings yet

- Risk Targeting in Seismic Design Codes: The State of The Art, Outstanding Issues and Possible Paths ForwardDocument13 pagesRisk Targeting in Seismic Design Codes: The State of The Art, Outstanding Issues and Possible Paths ForwardfaisaladeNo ratings yet

- A6 - Integrating Stakeholder Theory and Sustainability AccountingDocument12 pagesA6 - Integrating Stakeholder Theory and Sustainability AccountingIsabella Velasquez RodriguezNo ratings yet

- 2022 AifDocument127 pages2022 AifIsabel LoyolaNo ratings yet

- Embedding ESG Into Bank StrategiesDocument4 pagesEmbedding ESG Into Bank Strategiesali kiyaniNo ratings yet

- Jurnal Stigma Kanker Paru PDFDocument16 pagesJurnal Stigma Kanker Paru PDFsri subektiNo ratings yet

- 10.chapter 1 (Introduction To Investments) PDFDocument41 pages10.chapter 1 (Introduction To Investments) PDFEswari Devi100% (1)

- The Role of One Health in Wildlife Conservation: A Challenge and OpportunityDocument9 pagesThe Role of One Health in Wildlife Conservation: A Challenge and OpportunitySrikar KalidossNo ratings yet

- International Journal of Disaster Risk Reduction: Swarna Bintay KadirDocument9 pagesInternational Journal of Disaster Risk Reduction: Swarna Bintay KadirMeilha DwiNo ratings yet

- June 2010 Family Office Conference AgendaDocument11 pagesJune 2010 Family Office Conference Agendacraig2786100% (1)

- Blueprint - How To Start A Recruiting Agency in 2021, Part Two - CrelateDocument8 pagesBlueprint - How To Start A Recruiting Agency in 2021, Part Two - CrelateRajaNo ratings yet

- 6 April 2022 ExamDocument12 pages6 April 2022 ExamRafa'eel BickooNo ratings yet

- HIRA Register ExampleDocument1 pageHIRA Register ExampleSaravana kumar NagarajanNo ratings yet

- Participant Information SheetDocument5 pagesParticipant Information Sheetjagrit angrishNo ratings yet

- Specifications For The Protection of Cold Areas: Comité Européen Des AssurancesDocument20 pagesSpecifications For The Protection of Cold Areas: Comité Européen Des AssurancesArielNo ratings yet

- Bpt2601 Assignment 2Document4 pagesBpt2601 Assignment 2Anastasia DMNo ratings yet

- Neelam Dissertation Final ProjectDocument78 pagesNeelam Dissertation Final ProjectNeelam SharmaNo ratings yet

- A Meta-Analytic Study On Exploration and ExploitationDocument19 pagesA Meta-Analytic Study On Exploration and ExploitationkazekageNo ratings yet

- Entry Point Take Profit and Stop LossDocument2 pagesEntry Point Take Profit and Stop LossJay R Fuenzalida ValerosoNo ratings yet

- An Institutional Theory of Momentum and Revealsal Rev. Financ. Stud.-2013-Vayanos-1087-145Document59 pagesAn Institutional Theory of Momentum and Revealsal Rev. Financ. Stud.-2013-Vayanos-1087-145IGift WattanatornNo ratings yet