You might also like

- America's Healthy Future Act of 2009Document223 pagesAmerica's Healthy Future Act of 2009KFFHealthNewsNo ratings yet

- XTO Energy Liquidity and Solvency AnalysisDocument6 pagesXTO Energy Liquidity and Solvency AnalysisCarneadesNo ratings yet

- Components of RNOA - Profit Margin and Asset TurnoverDocument3 pagesComponents of RNOA - Profit Margin and Asset TurnoverCarneadesNo ratings yet

- Democrats and Out of State Campaign ContributionsDocument3 pagesDemocrats and Out of State Campaign ContributionsCarneadesNo ratings yet

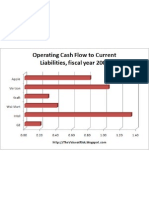

- OCF To Current LiabilitiesDocument1 pageOCF To Current LiabilitiesCarneadesNo ratings yet

- Bond Pricing 101Document3 pagesBond Pricing 101CarneadesNo ratings yet

- Vertical Analysis of Financial Statements - Pepsi V CokeDocument2 pagesVertical Analysis of Financial Statements - Pepsi V CokeCarneades33% (3)

- Basic V Diluted EPSDocument1 pageBasic V Diluted EPSCarneadesNo ratings yet

- Earnings Quality Analysis - Operating Cash Flow To Net IncomeDocument3 pagesEarnings Quality Analysis - Operating Cash Flow To Net IncomeCarneadesNo ratings yet

- Net Operating Profit Margin (NOPM)Document1 pageNet Operating Profit Margin (NOPM)CarneadesNo ratings yet

- Monthly CMBS Delinquency August 2009Document1 pageMonthly CMBS Delinquency August 2009CarneadesNo ratings yet

- Introduction To Credit Risk Analysis: Debt To Equity RatioDocument3 pagesIntroduction To Credit Risk Analysis: Debt To Equity RatioCarneadesNo ratings yet

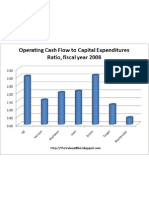

- OCF To CapexDocument1 pageOCF To CapexCarneadesNo ratings yet

- Duke Energy Allowances To ReceivablesDocument1 pageDuke Energy Allowances To ReceivablesCarneadesNo ratings yet

- Aetna Q2 09 Financial ResultsDocument14 pagesAetna Q2 09 Financial ResultsCarneadesNo ratings yet

- Social Security COLA History 1999-2009Document1 pageSocial Security COLA History 1999-2009CarneadesNo ratings yet

- Housing Starts August 2009Document1 pageHousing Starts August 2009CarneadesNo ratings yet

- ENSYS Cap and Trade Briefing 8-20-09Document25 pagesENSYS Cap and Trade Briefing 8-20-09CarneadesNo ratings yet

- SP/Case Shiller Index Through June 2009Document1 pageSP/Case Shiller Index Through June 2009CarneadesNo ratings yet

- Semiconductor Data Through July 2009Document2 pagesSemiconductor Data Through July 2009CarneadesNo ratings yet

- RealPoint CMBS Delinquency Report July 2009Document15 pagesRealPoint CMBS Delinquency Report July 2009Carneades100% (1)

- The SEC's Role Regarding and Oversight of Nationally Recognized Statistical Rating OrganizationsDocument124 pagesThe SEC's Role Regarding and Oversight of Nationally Recognized Statistical Rating OrganizationsCarneadesNo ratings yet

- Prison Population As % of US Population 1980-2007Document1 pagePrison Population As % of US Population 1980-2007CarneadesNo ratings yet

- Medicare Modernization ActDocument416 pagesMedicare Modernization ActCarneadesNo ratings yet

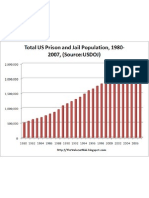

- US Prison Population 1980-2007Document1 pageUS Prison Population 1980-2007CarneadesNo ratings yet

- Moodys CPPI August 2009Document1 pageMoodys CPPI August 2009CarneadesNo ratings yet

- July 2009 Housing Starts 1959-PresentDocument1 pageJuly 2009 Housing Starts 1959-PresentCarneadesNo ratings yet

- July 2009 Housing Starts 2005-PresentDocument1 pageJuly 2009 Housing Starts 2005-PresentCarneadesNo ratings yet

- TIC Data June 2009Document1 pageTIC Data June 2009CarneadesNo ratings yet

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (890)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Training Material On West Bengal Financial Rules and Office ProceduresDocument150 pagesTraining Material On West Bengal Financial Rules and Office Proceduresswarnendu_janaNo ratings yet

- What Missourians Need To Know About The Show Me InstituteDocument21 pagesWhat Missourians Need To Know About The Show Me InstituteProgress Missouri0% (1)

- Governmental Operating Statement Accounts Budgetary AccountingDocument75 pagesGovernmental Operating Statement Accounts Budgetary Accountingመስቀል ኃይላችን ነው0% (2)

- Time To Rebuild The Ark:: Why The U.S. Cannot "Grow" Out of Its DebtDocument18 pagesTime To Rebuild The Ark:: Why The U.S. Cannot "Grow" Out of Its DebtcommonsensecongressNo ratings yet

- Domestic Resource Mobilisation IndiaDocument63 pagesDomestic Resource Mobilisation Indiaashish1981No ratings yet

- Public Fiscal Administration Part 1-1Document10 pagesPublic Fiscal Administration Part 1-1phoebeNo ratings yet

- Oakland County Candidate and Proposals ListDocument21 pagesOakland County Candidate and Proposals ListpkampeNo ratings yet

- ScriptDocument16 pagesScriptWarlitha DucayNo ratings yet

- DH 1114Document12 pagesDH 1114The Delphos HeraldNo ratings yet

- DILG - Rationalizing The Local Planning System of The PhilippinesDocument222 pagesDILG - Rationalizing The Local Planning System of The PhilippinesMia Monica Fojas Loyola100% (4)

- Introduction To Tax Ideology and PolicyDocument64 pagesIntroduction To Tax Ideology and PolicyfazrinbusirinNo ratings yet

- Booklet OECD Transfer Pricing Guidelines 2017Document24 pagesBooklet OECD Transfer Pricing Guidelines 2017Tommy StevenNo ratings yet

- House Hearing, 107TH Congress - President's Tax Relief Proposals: Individual Income Tax RatesDocument144 pagesHouse Hearing, 107TH Congress - President's Tax Relief Proposals: Individual Income Tax RatesScribd Government DocsNo ratings yet

- 2R Financial Utilization ReportDocument2 pages2R Financial Utilization Reportsabah8800No ratings yet

- Inheritance TaxDocument24 pagesInheritance TaxpeiyingongNo ratings yet

- Meaning of Consuelo RevisedDocument4 pagesMeaning of Consuelo Revisedapi-271652417No ratings yet

- Taxation Law Memory AidDocument130 pagesTaxation Law Memory AidToper HernandezNo ratings yet

- Butch Abad - On The Cusp of Budget TransformationDocument32 pagesButch Abad - On The Cusp of Budget TransformationFacebook.com/OscarFranklinTanNo ratings yet

- Lecture Notes On Philippines BudgetingDocument9 pagesLecture Notes On Philippines Budgetingzkkoech92% (12)

- Library Annexation ResolutionsDocument5 pagesLibrary Annexation ResolutionsDean RadfordNo ratings yet

- Americans For Prosperity FY 2017 Taxpayers' Budget - Executive SummaryDocument2 pagesAmericans For Prosperity FY 2017 Taxpayers' Budget - Executive SummaryAFPHQ_NewJerseyNo ratings yet

- PEST Analysis (Egypt Market) External Audit - Threats - OpportunitiesDocument13 pagesPEST Analysis (Egypt Market) External Audit - Threats - OpportunitiesBassem Safwat Boushra75% (4)

- Budget Its CoverageDocument36 pagesBudget Its CoveragenicahNo ratings yet

- Income Declaration FormDocument1 pageIncome Declaration FormGamy Glazyle100% (1)

- Municipal Policy BriefDocument4 pagesMunicipal Policy BriefAlbertaPartyNo ratings yet

- Role of Public Financial Management in Risk Management For Developing Country GovernmentsDocument31 pagesRole of Public Financial Management in Risk Management For Developing Country GovernmentsFreeBalanceGRPNo ratings yet

- EC 1630 Final Study Guide ContributorsDocument75 pagesEC 1630 Final Study Guide ContributorsTanit Kane ChearavanontNo ratings yet

- Tax Systems Around the World in 40 CharactersDocument11 pagesTax Systems Around the World in 40 CharactersQurat Ul AinNo ratings yet

- Budget Manual For LGUsDocument25 pagesBudget Manual For LGUsSheila Romulo100% (3)

- Amended 1040 Tax Form ExplainedDocument2 pagesAmended 1040 Tax Form Explainedgolcha_edu532No ratings yet