You might also like

- The Subprime Solution: How Today's Global Financial Crisis Happened, and What to Do about ItFrom EverandThe Subprime Solution: How Today's Global Financial Crisis Happened, and What to Do about ItRating: 2 out of 5 stars2/5 (2)

- Economic Crisis Matttick JRDocument31 pagesEconomic Crisis Matttick JRAnonymous mOdaetXf7iNo ratings yet

- Bubbles, Booms, and Busts: The Rise and Fall of Financial AssetsFrom EverandBubbles, Booms, and Busts: The Rise and Fall of Financial AssetsNo ratings yet

- Basic Points: Homeicide: The Crime of The CenturyDocument40 pagesBasic Points: Homeicide: The Crime of The Centuryvb12wxNo ratings yet

- 2003b Bpea CaseshillerDocument64 pages2003b Bpea Caseshillerarash saberianNo ratings yet

- The Global Financial CrisisDocument11 pagesThe Global Financial CrisisAmogh AroraNo ratings yet

- Nothing Is Too Big to Fail: How the Last Financial Crisis Informs TodayFrom EverandNothing Is Too Big to Fail: How the Last Financial Crisis Informs TodayNo ratings yet

- The 2007-08 Financial Crisis in Review: Credit CrunchDocument3 pagesThe 2007-08 Financial Crisis in Review: Credit CrunchNasir RandhawaNo ratings yet

- The Wall Street Journal Guide to the End of Wall Street as We Know It: What You Need to Know About the Greatest Financial Crisis of Our Time—and How to Survive ItFrom EverandThe Wall Street Journal Guide to the End of Wall Street as We Know It: What You Need to Know About the Greatest Financial Crisis of Our Time—and How to Survive ItNo ratings yet

- The Housing Bubble Explained: What Is A Bubble?Document12 pagesThe Housing Bubble Explained: What Is A Bubble?f;ljas;ldfjNo ratings yet

- Zezza - The Effects of A Declining Housing Market On The US Economy - 2007Document21 pagesZezza - The Effects of A Declining Housing Market On The US Economy - 2007sankaratNo ratings yet

- Globalisation Fractures: How major nations' interests are now in conflictFrom EverandGlobalisation Fractures: How major nations' interests are now in conflictNo ratings yet

- Krugman - How The Case For Austerity Has CrumbledDocument12 pagesKrugman - How The Case For Austerity Has CrumbledEklilEklildzNo ratings yet

- Financial Fiasco: How America's Infatuation With Homeownership and Easy Money Created the Financial CrisisFrom EverandFinancial Fiasco: How America's Infatuation With Homeownership and Easy Money Created the Financial CrisisRating: 5 out of 5 stars5/5 (1)

- Anatomy of A Train Wreck: Causes of The Mortgage MeltdownDocument29 pagesAnatomy of A Train Wreck: Causes of The Mortgage MeltdownNoor HigleyNo ratings yet

- Economics ProjectDocument34 pagesEconomics ProjectRuhan MasaniNo ratings yet

- Rogoff AER 2008Document6 pagesRogoff AER 2008maywayrandomNo ratings yet

- What Were The Causes of The Great Recession?Document32 pagesWhat Were The Causes of The Great Recession?tsheshrajNo ratings yet

- Safari - 18 Nov 2022 at 09 - 17Document1 pageSafari - 18 Nov 2022 at 09 - 17Tonie NascentNo ratings yet

- The Worldly PhilosophersDocument9 pagesThe Worldly Philosophersapi-26021962No ratings yet

- Financial Crisis of 2008Document11 pagesFinancial Crisis of 2008Sohael Shams SiamNo ratings yet

- Global FinanceDocument23 pagesGlobal Financealam_123istNo ratings yet

- Us Economy CrisisDocument30 pagesUs Economy CrisisAnjali BalanNo ratings yet

- Presentation 1Document20 pagesPresentation 1Chirag JainNo ratings yet

- Mayer Housing BubblesDocument30 pagesMayer Housing Bubblesarash saberianNo ratings yet

- Case StudyDocument7 pagesCase StudyMary ClaireNo ratings yet

- Understanding The Financial Crisis and Its Impact On Contemporary Business PDFDocument24 pagesUnderstanding The Financial Crisis and Its Impact On Contemporary Business PDFbundo_158547854No ratings yet

- David Capital Partners, LLC - 2013 Q4 Macro Commentary FINAL-1Document6 pagesDavid Capital Partners, LLC - 2013 Q4 Macro Commentary FINAL-1AAOI2No ratings yet

- K204040222 - Phạm Trần Cẩm Vi 4Document4 pagesK204040222 - Phạm Trần Cẩm Vi 4Nam Đỗ PhươngNo ratings yet

- The 2008 Financial Crisis: Causes, Response, and ConsequencesDocument22 pagesThe 2008 Financial Crisis: Causes, Response, and ConsequencesUNLV234No ratings yet

- April 102010 PostsDocument6 pagesApril 102010 PostsAlbert L. PeiaNo ratings yet

- A Minsky-Kindleberger Perspective On The Financial Crisis: J. Barkley Rosser, JR., Marina V. Rosser and Mauro GallegatiDocument11 pagesA Minsky-Kindleberger Perspective On The Financial Crisis: J. Barkley Rosser, JR., Marina V. Rosser and Mauro Gallegatilcr89No ratings yet

- Econ 100 FinalDocument2 pagesEcon 100 FinalfadetNo ratings yet

- Long Waves: An Update: Tsang Shu-KiDocument8 pagesLong Waves: An Update: Tsang Shu-KiTsang Shu-kiNo ratings yet

- Eclectica 08-09Document4 pagesEclectica 08-09ArcturusCapitalNo ratings yet

- 1.) 2008 US Financial CrisisDocument6 pages1.) 2008 US Financial CrisisleighdyNo ratings yet

- The Perfect StormDocument3 pagesThe Perfect StormWolfSnapNo ratings yet

- Enc2135 Project 1 Final Draft-2Document8 pagesEnc2135 Project 1 Final Draft-2api-643122560No ratings yet

- (502497459) Great Divide - Excerpt PDFDocument26 pages(502497459) Great Divide - Excerpt PDFwamu885No ratings yet

- America - A Walking DeathDocument10 pagesAmerica - A Walking DeathhshshshshshshNo ratings yet

- The Great RecessionDocument37 pagesThe Great RecessiontakzacharNo ratings yet

- Ricardo's Law: The Unintended Consequence of The Federal Government's Budget Only You Will SeeDocument8 pagesRicardo's Law: The Unintended Consequence of The Federal Government's Budget Only You Will Seehunghl9726No ratings yet

- MAAG - Its Deja Vododoo Economics All Over Again - March 2010Document6 pagesMAAG - Its Deja Vododoo Economics All Over Again - March 2010rhyzimmer02No ratings yet

- Research On Economic DepressionDocument12 pagesResearch On Economic Depressiondurdana samreenNo ratings yet

- Impact of U.S. Recession On India - An Empirical StudyDocument22 pagesImpact of U.S. Recession On India - An Empirical StudyashokdgaurNo ratings yet

- El2012 19Document7 pagesEl2012 19annawitkowski88No ratings yet

- 2008 Financial Crisis Subprime Mortgage Crisis Caused by The Unregulated Use of Derivatives U.S. Treasury Federal Reserve Economic CollapseDocument4 pages2008 Financial Crisis Subprime Mortgage Crisis Caused by The Unregulated Use of Derivatives U.S. Treasury Federal Reserve Economic CollapseShane TabunggaoNo ratings yet

- Acknowledgements Preface To The Second Edition PrologueDocument12 pagesAcknowledgements Preface To The Second Edition PrologueTimNo ratings yet

- U.S. and Global Imbalances: Can Dark Matter Prevent A Big Bang?Document11 pagesU.S. and Global Imbalances: Can Dark Matter Prevent A Big Bang?Pao SalazarNo ratings yet

- About The 2008 Stock Market CrashDocument8 pagesAbout The 2008 Stock Market CrashMohammed SajeeNo ratings yet

- Subprime CrisisDocument10 pagesSubprime Crisisbackup cmbmpNo ratings yet

- Global Financial Crisis: AnalysisDocument21 pagesGlobal Financial Crisis: Analysischinmaydeshmukh1No ratings yet

- Ibt Movie ReviewDocument7 pagesIbt Movie ReviewNorolhaya Usman100% (1)

- 1 Leonhardt 2008 Cant Grasp The Credit CrisisDocument3 pages1 Leonhardt 2008 Cant Grasp The Credit Crisiscarmo-netoNo ratings yet

- 2007-2008 Housing CrashDocument5 pages2007-2008 Housing CrashKanishk R.SinghNo ratings yet

- Global Economic Crisis - ProjectDocument9 pagesGlobal Economic Crisis - ProjectaasthasinghtomarNo ratings yet

- 03-17-08 Guardian-America Was Conned - Who Will Pay Larry EDocument3 pages03-17-08 Guardian-America Was Conned - Who Will Pay Larry EMark WelkieNo ratings yet

- Weaponization Committee: HOW A "CYBERSECURITY" AGENCY COLLUDED WITH BIG TECH AND "DISINFORMATION" PARTNERS TO CENSOR AMERICANSDocument37 pagesWeaponization Committee: HOW A "CYBERSECURITY" AGENCY COLLUDED WITH BIG TECH AND "DISINFORMATION" PARTNERS TO CENSOR AMERICANSJim Hoft100% (2)

- Reynolds Public Health Proclamation - 2020.04.06Document5 pagesReynolds Public Health Proclamation - 2020.04.06Shane Vander HartNo ratings yet

- Fifth Circuit Decision Against FDA in Apter CaseDocument24 pagesFifth Circuit Decision Against FDA in Apter CaseAssociation of American Physicians and Surgeons100% (1)

- HY Vs IG DurationDocument1 pageHY Vs IG DurationCreditTraderNo ratings yet

- Credit ContractionDocument1 pageCredit ContractionCreditTraderNo ratings yet

- SPL 20101019Document1 pageSPL 20101019CreditTraderNo ratings yet

- USD TLGP MaturitiesDocument1 pageUSD TLGP MaturitiesCreditTraderNo ratings yet

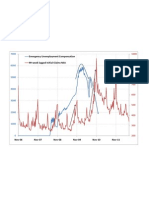

- EUC and 99-Week-Lagged Initial ClaimsDocument1 pageEUC and 99-Week-Lagged Initial ClaimsCreditTraderNo ratings yet

- IG Fundamentals Q22010Document1 pageIG Fundamentals Q22010CreditTraderNo ratings yet

- EUR Vs GDP-Weighted CDSDocument1 pageEUR Vs GDP-Weighted CDSCreditTraderNo ratings yet

- HY-IG Vs EquityDocument1 pageHY-IG Vs EquityCreditTraderNo ratings yet

- IG-HY Vs Stocks Relative-ValueDocument1 pageIG-HY Vs Stocks Relative-ValueCreditTraderNo ratings yet

- SPX Now and ThenDocument1 pageSPX Now and ThenCreditTraderNo ratings yet

- HY-IG Vs StocksDocument1 pageHY-IG Vs StocksCreditTraderNo ratings yet

- FSB30 IntrinsicsDocument1 pageFSB30 IntrinsicsCreditTraderNo ratings yet

- CDR Csa Aug2010Document1 pageCDR Csa Aug2010CreditTraderNo ratings yet

- IG Over TSYDocument1 pageIG Over TSYCreditTraderNo ratings yet

- C&I Loans + ABCP - Aggregate CreditDocument1 pageC&I Loans + ABCP - Aggregate CreditCreditTraderNo ratings yet

- CDR Csa 20100813Document1 pageCDR Csa 20100813CreditTraderNo ratings yet

- CDR Csa Scatter Aug10Document1 pageCDR Csa Scatter Aug10CreditTraderNo ratings yet

- CDR Csa 20100716Document1 pageCDR Csa 20100716CreditTraderNo ratings yet

- IG Weekly RangeDocument1 pageIG Weekly RangeCreditTraderNo ratings yet

- JUN Roll by SectorDocument1 pageJUN Roll by SectorCreditTraderNo ratings yet

- CDR Csa 201007Document1 pageCDR Csa 201007CreditTraderNo ratings yet

- Spread Leverage ComparisonDocument1 pageSpread Leverage ComparisonCreditTraderNo ratings yet

- Implied CorrelationDocument1 pageImplied CorrelationCreditTraderNo ratings yet

- IG Range CompressionDocument1 pageIG Range CompressionCreditTraderNo ratings yet

- IG Vs TSY CycleDocument1 pageIG Vs TSY CycleCreditTraderNo ratings yet

- Exchange Rate Regime Analysis For The Chinese YuanDocument10 pagesExchange Rate Regime Analysis For The Chinese YuanCreditTraderNo ratings yet

- Loan Application FormDocument2 pagesLoan Application FormKaichou NeteroNo ratings yet

- Answer Key Chapter 6 Corporate LiquidationDocument11 pagesAnswer Key Chapter 6 Corporate Liquidationkaren perrerasNo ratings yet

- Black BookDocument41 pagesBlack BookMoazza QureshiNo ratings yet

- Investment For African Development: Making It Happen: Nepad/Oecd Investment InitiativeDocument37 pagesInvestment For African Development: Making It Happen: Nepad/Oecd Investment InitiativeAngie_Monteagu_6929No ratings yet

- Masala BondsDocument3 pagesMasala BondsRashmi BihaniNo ratings yet

- ISJ003Document100 pagesISJ0032imediaNo ratings yet

- Insular Investment & Trust Corp. V Capital One Equities Corp & PlantersDocument27 pagesInsular Investment & Trust Corp. V Capital One Equities Corp & PlantersMicah Clark-MalinaoNo ratings yet

- 1339617927061412Document20 pages1339617927061412CoolerAdsNo ratings yet

- Clarita Depakakibo GarciaDocument5 pagesClarita Depakakibo GarciaKristel Jane Palomado CaldozaNo ratings yet

- Fnce 100 Final Cheat SheetDocument2 pagesFnce 100 Final Cheat SheetToby Arriaga100% (2)

- Corporate Finance Chapter 6Document7 pagesCorporate Finance Chapter 6Razan EidNo ratings yet

- ADVANCED AUDITING Revision QNS, Check CoverageDocument21 pagesADVANCED AUDITING Revision QNS, Check CoverageRewardMaturure100% (2)

- fc7bb - Tech Shristi Salary Income TaxDocument76 pagesfc7bb - Tech Shristi Salary Income TaxGopal SharmaNo ratings yet

- Citi BankDocument40 pagesCiti BankZeeshan Mobeen100% (1)

- Law Digest InsolvencyDocument187 pagesLaw Digest InsolvencytutsipoppyNo ratings yet

- Copper Contract TurkeyDocument9 pagesCopper Contract TurkeyHasan Uyan67% (3)

- US Internal Revenue Service: 2005p1212 Sect I-IiiDocument168 pagesUS Internal Revenue Service: 2005p1212 Sect I-IiiIRSNo ratings yet

- International Payment SystemsDocument2 pagesInternational Payment SystemsPrerna SharmaNo ratings yet

- Manage Money TemplateDocument1 pageManage Money TemplateRahman ZafNo ratings yet

- CFE - SNL Bank Valuation BrochureDocument5 pagesCFE - SNL Bank Valuation BrochureFahad MirNo ratings yet

- UACS (Cat)Document103 pagesUACS (Cat)lairah.mananNo ratings yet

- Microfinance Management Solution On Tally - ERP9 - MpowerDocument28 pagesMicrofinance Management Solution On Tally - ERP9 - MpowerMilansolutionsNo ratings yet

- Bank Alfalah Clearance DepartmentDocument7 pagesBank Alfalah Clearance Departmenthassan_shazaib100% (1)

- STARR V BAC CHL BNY-Deposition-Of-Renee-Hertzler-02 19 2010 (Bank Fraud/securities Fraud/bankruptcy Fraud/forgery)Document67 pagesSTARR V BAC CHL BNY-Deposition-Of-Renee-Hertzler-02 19 2010 (Bank Fraud/securities Fraud/bankruptcy Fraud/forgery)Tim Bryant100% (1)

- Capacity To ContractDocument10 pagesCapacity To ContractEsha bansalNo ratings yet

- Advance Acctg. Dayag 2013Document12 pagesAdvance Acctg. Dayag 2013Clarize R. Mabiog100% (2)

- Instadeep Sarl Daily Cash Status: Column1Document3 pagesInstadeep Sarl Daily Cash Status: Column1lassaad bahloulNo ratings yet

- Central Civil Services (Conduct) Rules, 1964: ISTM 2015Document48 pagesCentral Civil Services (Conduct) Rules, 1964: ISTM 2015Abhishek100% (1)

- The Wall Street Journal - 2019-09-21 PDFDocument54 pagesThe Wall Street Journal - 2019-09-21 PDFKevin MillánNo ratings yet

- #5 PFRS 5Document3 pages#5 PFRS 5jaysonNo ratings yet

- A History of the United States in Five Crashes: Stock Market Meltdowns That Defined a NationFrom EverandA History of the United States in Five Crashes: Stock Market Meltdowns That Defined a NationRating: 4 out of 5 stars4/5 (11)

- The Trillion-Dollar Conspiracy: How the New World Order, Man-Made Diseases, and Zombie Banks Are Destroying AmericaFrom EverandThe Trillion-Dollar Conspiracy: How the New World Order, Man-Made Diseases, and Zombie Banks Are Destroying AmericaNo ratings yet

- Financial Literacy for All: Disrupting Struggle, Advancing Financial Freedom, and Building a New American Middle ClassFrom EverandFinancial Literacy for All: Disrupting Struggle, Advancing Financial Freedom, and Building a New American Middle ClassNo ratings yet

- Economics 101: How the World WorksFrom EverandEconomics 101: How the World WorksRating: 4.5 out of 5 stars4.5/5 (34)

- Look Again: The Power of Noticing What Was Always ThereFrom EverandLook Again: The Power of Noticing What Was Always ThereRating: 5 out of 5 stars5/5 (3)

- The Meth Lunches: Food and Longing in an American CityFrom EverandThe Meth Lunches: Food and Longing in an American CityRating: 5 out of 5 stars5/5 (5)

- The War Below: Lithium, Copper, and the Global Battle to Power Our LivesFrom EverandThe War Below: Lithium, Copper, and the Global Battle to Power Our LivesRating: 4.5 out of 5 stars4.5/5 (8)

- This Changes Everything: Capitalism vs. The ClimateFrom EverandThis Changes Everything: Capitalism vs. The ClimateRating: 4 out of 5 stars4/5 (349)

- University of Berkshire Hathaway: 30 Years of Lessons Learned from Warren Buffett & Charlie Munger at the Annual Shareholders MeetingFrom EverandUniversity of Berkshire Hathaway: 30 Years of Lessons Learned from Warren Buffett & Charlie Munger at the Annual Shareholders MeetingRating: 4.5 out of 5 stars4.5/5 (97)

- Chip War: The Quest to Dominate the World's Most Critical TechnologyFrom EverandChip War: The Quest to Dominate the World's Most Critical TechnologyRating: 4.5 out of 5 stars4.5/5 (228)

- Principles for Dealing with the Changing World Order: Why Nations Succeed or FailFrom EverandPrinciples for Dealing with the Changing World Order: Why Nations Succeed or FailRating: 4.5 out of 5 stars4.5/5 (237)

- Economics 101: From Consumer Behavior to Competitive Markets—Everything You Need to Know About EconomicsFrom EverandEconomics 101: From Consumer Behavior to Competitive Markets—Everything You Need to Know About EconomicsRating: 5 out of 5 stars5/5 (3)

- The Infinite Machine: How an Army of Crypto-Hackers Is Building the Next Internet with EthereumFrom EverandThe Infinite Machine: How an Army of Crypto-Hackers Is Building the Next Internet with EthereumRating: 3 out of 5 stars3/5 (12)

- Anarchy, State, and Utopia: Second EditionFrom EverandAnarchy, State, and Utopia: Second EditionRating: 3.5 out of 5 stars3.5/5 (180)

- Deaths of Despair and the Future of CapitalismFrom EverandDeaths of Despair and the Future of CapitalismRating: 4.5 out of 5 stars4.5/5 (30)

- The New Elite: Inside the Minds of the Truly WealthyFrom EverandThe New Elite: Inside the Minds of the Truly WealthyRating: 4 out of 5 stars4/5 (10)

- The Myth of the Rational Market: A History of Risk, Reward, and Delusion on Wall StreetFrom EverandThe Myth of the Rational Market: A History of Risk, Reward, and Delusion on Wall StreetNo ratings yet

- Vulture Capitalism: Corporate Crimes, Backdoor Bailouts, and the Death of FreedomFrom EverandVulture Capitalism: Corporate Crimes, Backdoor Bailouts, and the Death of FreedomNo ratings yet

- Narrative Economics: How Stories Go Viral and Drive Major Economic EventsFrom EverandNarrative Economics: How Stories Go Viral and Drive Major Economic EventsRating: 4.5 out of 5 stars4.5/5 (94)

- The Technology Trap: Capital, Labor, and Power in the Age of AutomationFrom EverandThe Technology Trap: Capital, Labor, and Power in the Age of AutomationRating: 4.5 out of 5 stars4.5/5 (46)

- These are the Plunderers: How Private Equity Runs—and Wrecks—AmericaFrom EverandThese are the Plunderers: How Private Equity Runs—and Wrecks—AmericaRating: 4.5 out of 5 stars4.5/5 (14)