You might also like

- Plus: A 2011 Forecast From GFT'S David Morrison, Kathy Lien and Boris SchlossbergDocument23 pagesPlus: A 2011 Forecast From GFT'S David Morrison, Kathy Lien and Boris Schlossbergn73686861No ratings yet

- Hong Kong 2011 Economic OutlookDocument11 pagesHong Kong 2011 Economic OutlookKwok TaiNo ratings yet

- Jul 16 Erste Group Macro Markets UsaDocument6 pagesJul 16 Erste Group Macro Markets UsaMiir ViirNo ratings yet

- Trends Impacting RestaurantsDocument11 pagesTrends Impacting RestaurantsrangerscribdNo ratings yet

- Financial Crisis AftermathDocument23 pagesFinancial Crisis AftermathRafay KhanNo ratings yet

- The Impact of The Rer On United Kingdom Foreign Trade: EURO 372 ProjectDocument8 pagesThe Impact of The Rer On United Kingdom Foreign Trade: EURO 372 ProjecthalilkusbeNo ratings yet

- Value Investing Congress October 13, 2010 T2 Accredited Fund, LP Tilson Offshore Fund, Ltd. T2 Qualified Fund, LPDocument46 pagesValue Investing Congress October 13, 2010 T2 Accredited Fund, LP Tilson Offshore Fund, Ltd. T2 Qualified Fund, LPuxfarooqNo ratings yet

- Economic Update Nov201Document12 pagesEconomic Update Nov201admin866No ratings yet

- Patience: Bad News Will Become Good News: SG Multi AssetDocument51 pagesPatience: Bad News Will Become Good News: SG Multi AssetBurj CapitalNo ratings yet

- Big Rock Candy MountainDocument63 pagesBig Rock Candy MountainrguyNo ratings yet

- Global Markets Chart Book: High-Grade Bond Yields Plunge To Record LowsDocument12 pagesGlobal Markets Chart Book: High-Grade Bond Yields Plunge To Record LowslosdiabloNo ratings yet

- Keats April 21 2011Document31 pagesKeats April 21 2011Sanjay JagatsinghNo ratings yet

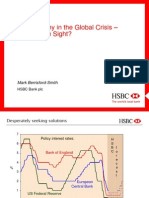

- HSCB Mark Berrisford Smith PresentationDocument42 pagesHSCB Mark Berrisford Smith PresentationMikeNigawhatupNo ratings yet

- Weekly Economic Commentary 10-10-11Document8 pagesWeekly Economic Commentary 10-10-11monarchadvisorygroupNo ratings yet

- The Aftermath of The Housing Bubble: James BullardDocument38 pagesThe Aftermath of The Housing Bubble: James Bullardannawitkowski88No ratings yet

- Lacy Hunt - Hoisington - Quartely Review Q1 2015Document5 pagesLacy Hunt - Hoisington - Quartely Review Q1 2015TREND_7425No ratings yet

- From Capitalism To Creditism Feb 27 2014Document22 pagesFrom Capitalism To Creditism Feb 27 2014richardck61No ratings yet

- The Forces Shaping The Economy Over 2012Document10 pagesThe Forces Shaping The Economy Over 2012economicdelusionNo ratings yet

- Monthly Economic Outlook 06082011Document6 pagesMonthly Economic Outlook 06082011jws_listNo ratings yet

- The Pensford Letter - 7.30.12Document4 pagesThe Pensford Letter - 7.30.12Pensford FinancialNo ratings yet

- Foote NENPA Fall ConferenceDocument36 pagesFoote NENPA Fall Conferencenenpa10No ratings yet

- Home Construction Sinks, Building Permits DownDocument30 pagesHome Construction Sinks, Building Permits DownAlbert L. PeiaNo ratings yet

- Brazil Russia India China South AfricaDocument3 pagesBrazil Russia India China South AfricaRAHULSHARMA1985999No ratings yet

- The 2011 Economic Outlook - Credit Given Where Credit Is DueDocument37 pagesThe 2011 Economic Outlook - Credit Given Where Credit Is Duerogerwilcomina3407No ratings yet

- Challenges Amid The Global Economic Storm: Northwest Insurance Council 2009 Annual Luncheon Seattle, WA January 27, 2009Document70 pagesChallenges Amid The Global Economic Storm: Northwest Insurance Council 2009 Annual Luncheon Seattle, WA January 27, 2009Vasantha NaikNo ratings yet

- Report On Risk ProfileDocument16 pagesReport On Risk ProfilehuraldayNo ratings yet

- Quick Start Report - 2011-12 - Final 11.5.10Document50 pagesQuick Start Report - 2011-12 - Final 11.5.10New York SenateNo ratings yet

- Economic Snapshot For June 2011Document4 pagesEconomic Snapshot For June 2011Center for American ProgressNo ratings yet

- Economic NewsEconomic News of The Wiregrass - 10 Jun 10Document4 pagesEconomic NewsEconomic News of The Wiregrass - 10 Jun 10webwisetomNo ratings yet

- Leveling The Playing Field December 3, 2012Document7 pagesLeveling The Playing Field December 3, 2012Pensford FinancialNo ratings yet

- 2012 Economic and Housing Market OutlookDocument38 pages2012 Economic and Housing Market OutlooknarwebteamNo ratings yet

- The Pensford Letter - 1.28.13Document6 pagesThe Pensford Letter - 1.28.13Pensford FinancialNo ratings yet

- Newshrink 2Document50 pagesNewshrink 2David TollNo ratings yet

- Deflation Prevention and Cure: Willem BuiterDocument33 pagesDeflation Prevention and Cure: Willem BuiterNavneet AmrateNo ratings yet

- Strong U.K. Economic Recovery Remains Intact: Economics GroupDocument5 pagesStrong U.K. Economic Recovery Remains Intact: Economics Grouppathanfor786No ratings yet

- JUNE 2009 Modest Growth, Higher Unemployment Predicted For Second Half of 2009Document10 pagesJUNE 2009 Modest Growth, Higher Unemployment Predicted For Second Half of 2009rebeltradersNo ratings yet

- The Bconomic and Budget Outlook: Fiscal Years 1994-1998Document175 pagesThe Bconomic and Budget Outlook: Fiscal Years 1994-1998Peggy W SatterfieldNo ratings yet

- Indonesias Economic Outlook 2011Document93 pagesIndonesias Economic Outlook 2011lutfhizNo ratings yet

- NomuraDocument37 pagesNomuradavidmcookNo ratings yet

- Assignment ADocument6 pagesAssignment Acary_puyatNo ratings yet

- Morning Call - June 3 2010Document7 pagesMorning Call - June 3 2010chibondkingNo ratings yet

- Update of The Budget and Economic OutlookDocument35 pagesUpdate of The Budget and Economic OutlookScribd Government DocsNo ratings yet

- Eco Project UKDocument16 pagesEco Project UKPankesh SethiNo ratings yet

- June 142010 PostsDocument28 pagesJune 142010 PostsAlbert L. PeiaNo ratings yet

- Weekly Market Commentary 10-24-11Document5 pagesWeekly Market Commentary 10-24-11monarchadvisorygroupNo ratings yet

- 06 - 10 Wither Green ShootsDocument4 pages06 - 10 Wither Green Shootsrichardck30No ratings yet

- University of Gloucestershire: MBA-1 (GROUP-D)Document13 pagesUniversity of Gloucestershire: MBA-1 (GROUP-D)Nikunj PatelNo ratings yet

- August 232010 PostsDocument293 pagesAugust 232010 PostsAlbert L. PeiaNo ratings yet

- c1 PDFDocument11 pagesc1 PDFDanish CooperNo ratings yet

- Weekly Economic Commentary: Beige Book: Window On Main StreetDocument7 pagesWeekly Economic Commentary: Beige Book: Window On Main Streetapi-136397169No ratings yet

- Senate Hearing, 111TH Congress - A Status Report On The U.S. EconomyDocument262 pagesSenate Hearing, 111TH Congress - A Status Report On The U.S. EconomyScribd Government DocsNo ratings yet

- Economic Focus 8-29-11Document1 pageEconomic Focus 8-29-11Jessica Kister-LombardoNo ratings yet

- Mark Kleinman: Warning: Slow Growth AheadDocument31 pagesMark Kleinman: Warning: Slow Growth AheadCity A.M.No ratings yet

- Model Questions - 2018 - Macroeconomics FinalDocument9 pagesModel Questions - 2018 - Macroeconomics FinalSomidu ChandimalNo ratings yet

- Economic Insights 25 02 13Document16 pagesEconomic Insights 25 02 13vikashpunglia@rediffmail.comNo ratings yet

- Calhoun County 2013-14 Economic ForecastDocument56 pagesCalhoun County 2013-14 Economic ForecastBCEnquirerNo ratings yet

- United States, Financial and Economic Crisis: The Recovery EconomicsFrom EverandUnited States, Financial and Economic Crisis: The Recovery EconomicsNo ratings yet

- Jul20 ErDocument5 pagesJul20 Errwmortell3580No ratings yet

- Marcato Buffalo Wild Wings Presentation Jun 2016Document48 pagesMarcato Buffalo Wild Wings Presentation Jun 2016rwmortell3580No ratings yet

- Q3 2020 High Yield Bank Loan ReportDocument16 pagesQ3 2020 High Yield Bank Loan Reportrwmortell3580No ratings yet

- Enron Message BoardDocument36 pagesEnron Message Boardrwmortell3580No ratings yet

- Liquidity Cascades - Newfound Research PDFDocument19 pagesLiquidity Cascades - Newfound Research PDFrwmortell3580No ratings yet

- Sequoia Ann 14Document36 pagesSequoia Ann 14CanadianValueNo ratings yet

- Y 2015 Annual LetterDocument24 pagesY 2015 Annual Letterrwmortell3580No ratings yet

- Rates BofE UpdateDocument47 pagesRates BofE Updaterwmortell3580No ratings yet

- How Well Do You CompareDocument17 pagesHow Well Do You Comparerwmortell3580No ratings yet

- Fear, Greed & Liquidity: January 2013Document10 pagesFear, Greed & Liquidity: January 2013rwmortell3580No ratings yet

- Q2 2013 Market UpdateDocument57 pagesQ2 2013 Market Updaterwmortell3580No ratings yet

- Corsair Q3 NWSA ThesisDocument5 pagesCorsair Q3 NWSA Thesisrwmortell3580No ratings yet

- Cards Against HumanityDocument31 pagesCards Against Humanityrwmortell3580No ratings yet

- Ruane Cunniff Sequoia Fund Annual LetterDocument29 pagesRuane Cunniff Sequoia Fund Annual Letterrwmortell3580No ratings yet

- Arithmetic of EquitiesDocument5 pagesArithmetic of Equitiesrwmortell3580No ratings yet

- FFH 2010 Annual LetterDocument11 pagesFFH 2010 Annual Letterrwmortell3580No ratings yet

- Gov Uscourts Ilnb 1098576 1 0Document39 pagesGov Uscourts Ilnb 1098576 1 0Ahmet KurtNo ratings yet

- Amortization Sinking Funds: Click To Edit Master Title StyleDocument22 pagesAmortization Sinking Funds: Click To Edit Master Title StyleCaryl KimNo ratings yet

- The Wordsmith SutrasDocument32 pagesThe Wordsmith SutrasPritam Bhattacharyya100% (3)

- Companies Act of OmanDocument41 pagesCompanies Act of Omanvirg0o0o0No ratings yet

- Idioms BussinesDocument33 pagesIdioms Bussinesmadalinam78No ratings yet

- Cellcom Israel Ltd. 20f 20110315Document386 pagesCellcom Israel Ltd. 20f 20110315manasgautamNo ratings yet

- International Strategy of TH TRUE MILKDocument17 pagesInternational Strategy of TH TRUE MILKThu HàNo ratings yet

- Product CalculationDocument65 pagesProduct CalculationmidhunnobleNo ratings yet

- ACCA P4 NotesDocument103 pagesACCA P4 NotesTanim Misbahul M100% (2)

- Terms of AgreementDocument3 pagesTerms of AgreementSodiq Okikiola HammedNo ratings yet

- Financial Statement Analysis 12thDocument2 pagesFinancial Statement Analysis 12thRohitNo ratings yet

- Protection Analysis Report Somaliland 2019 Clean VersionDocument17 pagesProtection Analysis Report Somaliland 2019 Clean VersionAbdirahman Ismail100% (1)

- Plan Z How To Survive Financial Crisis and Even Live A Little BetterDocument76 pagesPlan Z How To Survive Financial Crisis and Even Live A Little BetterBangem100% (4)

- Gitman - PPT - ch06 Bond ValuationDocument56 pagesGitman - PPT - ch06 Bond ValuationFerry GumilarNo ratings yet

- Lehman Brothers Case StudyDocument5 pagesLehman Brothers Case StudykrishhonlineNo ratings yet

- MVP Private Placement Bond Financing OutlineDocument2 pagesMVP Private Placement Bond Financing OutlineLarry JacksonNo ratings yet

- $ The Billionaire's Business Blueprint $Document336 pages$ The Billionaire's Business Blueprint $Reginald Ringgold97% (58)

- General Mathematics LAS Q2 WK 6Document18 pagesGeneral Mathematics LAS Q2 WK 6Prince Joshua SumagitNo ratings yet

- Case Study Avon FinalDocument36 pagesCase Study Avon FinalDivine CastroNo ratings yet

- BANK3011 Workshop Week 3 SolutionsDocument5 pagesBANK3011 Workshop Week 3 SolutionsZahraaNo ratings yet

- Accounting Research Journal September 2015Document25 pagesAccounting Research Journal September 2015Firehun GichiloNo ratings yet

- Mccloud'S Winery: Managerial AccountingDocument11 pagesMccloud'S Winery: Managerial AccountingsherNo ratings yet

- Performance Appraisal - Paper F7 Financial Reporting - ACCA Qualification - Students - ACCA GlobalDocument4 pagesPerformance Appraisal - Paper F7 Financial Reporting - ACCA Qualification - Students - ACCA GlobalInga ȚîgaiNo ratings yet

- Loan Agreement: Opp Andhra Bank Rudrapur RoadDocument7 pagesLoan Agreement: Opp Andhra Bank Rudrapur RoadMiddha Law Firm RudrapurNo ratings yet

- Mudio Islamic Examination Board (Mieb)Document5 pagesMudio Islamic Examination Board (Mieb)MmaryNo ratings yet

- Sole ProprietorDocument3 pagesSole ProprietorUnais AhmedNo ratings yet

- CDO StructureDocument2 pagesCDO StructuretvlodekNo ratings yet

- Profitability & Liquidity Ratio AnalysisDocument19 pagesProfitability & Liquidity Ratio AnalysisananditaNo ratings yet

- Debt Financing or Equity FinancingDocument10 pagesDebt Financing or Equity Financingimran hossain ruman100% (1)

- Debt CollectionDocument12 pagesDebt CollectionTaranisaNo ratings yet