You might also like

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (890)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Rich Dad Poor DadDocument26 pagesRich Dad Poor Dadchaand33100% (17)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- Types of EntrepreneursDocument32 pagesTypes of EntrepreneursabbsheyNo ratings yet

- Recovery Catalytic Converters RefiningDocument20 pagesRecovery Catalytic Converters RefiningAFLAC ............80% (5)

- Tax 2 - Midterm ExamDocument2 pagesTax 2 - Midterm ExamMichelle MatubisNo ratings yet

- Daimler Chrysler MergerDocument23 pagesDaimler Chrysler MergerAdnan Ad100% (1)

- Future of POL RetailingDocument18 pagesFuture of POL RetailingSuresh MalodiaNo ratings yet

- LLP NotesDocument8 pagesLLP NotesRajaNo ratings yet

- Audit Evidence and Programs ReviewDocument9 pagesAudit Evidence and Programs ReviewcutieaikoNo ratings yet

- Ceiling heating system guideDocument4 pagesCeiling heating system guideUday Kiran100% (1)

- TCC Midc Company ListDocument4 pagesTCC Midc Company ListAbhishek SinghNo ratings yet

- TaxDocument3 pagesTaxCess MelendezNo ratings yet

- 5746Document2 pages5746cutieaikoNo ratings yet

- HobDocument5 pagesHobcutieaikoNo ratings yet

- 5764Document4 pages5764cutieaikoNo ratings yet

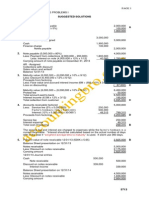

- Suggested Solutions Share Based Payment Compensation 5745 1Document1 pageSuggested Solutions Share Based Payment Compensation 5745 1cutieaikoNo ratings yet

- Installment SalesDocument3 pagesInstallment SalesEpal Ako67% (3)

- 5765Document4 pages5765cutieaikoNo ratings yet

- HOB SolutionsDocument5 pagesHOB SolutionscutieaikoNo ratings yet

- HOB SolutionsDocument5 pagesHOB SolutionscutieaikoNo ratings yet

- Practical Accounting Problems Cash and Cash Equivalents SolutionsDocument1 pagePractical Accounting Problems Cash and Cash Equivalents SolutionscutieaikoNo ratings yet

- Formation & OperationDocument4 pagesFormation & OperationcutieaikoNo ratings yet

- Tax 2Document11 pagesTax 2cutieaikoNo ratings yet

- SqueezedDocument1 pageSqueezedcutieaikoNo ratings yet

- Its Fair Value Less Costs To Sell (If Determinable) Its Value in Use (If Determinable) andDocument2 pagesIts Fair Value Less Costs To Sell (If Determinable) Its Value in Use (If Determinable) andcutieaikoNo ratings yet

- HobDocument5 pagesHobcutieaikoNo ratings yet

- 5715 5716Document2 pages5715 5716cutieaikoNo ratings yet

- HOB SolutionsDocument5 pagesHOB SolutionscutieaikoNo ratings yet

- Receivables Factoring and Financing SolutionsDocument2 pagesReceivables Factoring and Financing SolutionscutieaikoNo ratings yet

- Accounting for discontinued operations and non-current assets held for saleDocument1 pageAccounting for discontinued operations and non-current assets held for salecutieaikoNo ratings yet

- Tax 2Document11 pagesTax 2cutieaikoNo ratings yet

- Suggested SolutionsDocument1 pageSuggested SolutionscutieaikoNo ratings yet

- Not Collectible Within The Normal Operating Cycle Hence Amount To Be Collected Beyond 12 Months Shall Be Classified As A Noncurrent ReceivableDocument1 pageNot Collectible Within The Normal Operating Cycle Hence Amount To Be Collected Beyond 12 Months Shall Be Classified As A Noncurrent ReceivablecutieaikoNo ratings yet

- 01 Glossary of Terms December 2002Document20 pages01 Glossary of Terms December 2002Tracy KayeNo ratings yet

- Suggested Solutions 5740 Deferred Income Tax 1Document1 pageSuggested Solutions 5740 Deferred Income Tax 1cutieaikoNo ratings yet

- Audit questions and answers on assertions, evidence, risk, and proceduresDocument8 pagesAudit questions and answers on assertions, evidence, risk, and procedurescutieaikoNo ratings yet

- Business Combination and Date of AcquisitionDocument3 pagesBusiness Combination and Date of AcquisitioncutieaikoNo ratings yet

- Avocado Production in The PhilippinesDocument20 pagesAvocado Production in The Philippinescutieaiko100% (1)

- Auditing Theory Quiz Final PrintDocument6 pagesAuditing Theory Quiz Final Printnda0403No ratings yet

- Critique Paper BA211 12 NN HRM - DacumosDocument2 pagesCritique Paper BA211 12 NN HRM - DacumosCherBear A. DacumosNo ratings yet

- Turquía 7.25% - 2038 - US900123BB58Document61 pagesTurquía 7.25% - 2038 - US900123BB58montyviaderoNo ratings yet

- Pengaruh Kualitas Bahan Baku Dan ProsesDocument11 pagesPengaruh Kualitas Bahan Baku Dan Proses039 Trio SukmonoNo ratings yet

- Luxreal Detail Marketing Plan (2019) UsdDocument32 pagesLuxreal Detail Marketing Plan (2019) UsdTawanda Tirivangani100% (2)

- Data Link Institute of Business and TechnologyDocument6 pagesData Link Institute of Business and TechnologySonal AgarwalNo ratings yet

- 4 93-F Y B A - Micro-EconomicsDocument3 pages4 93-F Y B A - Micro-EconomicsSanjdsgNo ratings yet

- Analisa Investasi AlatDocument15 pagesAnalisa Investasi AlatPaula Olivia SaiyaNo ratings yet

- User Exits in Sales Document ProcessingDocument9 pagesUser Exits in Sales Document Processingkirankumar723No ratings yet

- US Internal Revenue Service: p1438Document518 pagesUS Internal Revenue Service: p1438IRSNo ratings yet

- Data Prep - Homogeneity (Excel)Document5 pagesData Prep - Homogeneity (Excel)NumXL ProNo ratings yet

- Rjis 16 04Document14 pagesRjis 16 04geo12345abNo ratings yet

- 20 Recent IELTS Graph Samples With AnswersDocument14 pages20 Recent IELTS Graph Samples With AnswersRizwan BashirNo ratings yet

- 21936mtp Cptvolu1 Part4Document404 pages21936mtp Cptvolu1 Part4Arun KCNo ratings yet

- Energia Solar en EspañaDocument1 pageEnergia Solar en EspañaCatalin LeusteanNo ratings yet

- Perfect Substitutes and Perfect ComplementsDocument2 pagesPerfect Substitutes and Perfect ComplementsVijayalaxmi DhakaNo ratings yet

- Forex - Nnet Vs RegDocument6 pagesForex - Nnet Vs RegAnshik BansalNo ratings yet

- Measuring Elasticity of SupplyDocument16 pagesMeasuring Elasticity of SupplyPetronilo De Leon Jr.No ratings yet

- NN Case StudyDocument9 pagesNN Case StudyAzuati MahmudNo ratings yet

- Construction Work Schedule For Boundary WallDocument1 pageConstruction Work Schedule For Boundary WallBaburam ChaudharyNo ratings yet

- Marx Alienated LaborDocument5 pagesMarx Alienated LaborDanielle BenderNo ratings yet

- Directory of Cao 01042018Document154 pagesDirectory of Cao 01042018Shyam SNo ratings yet